Download

1 / 24

240 likes | 305 Views

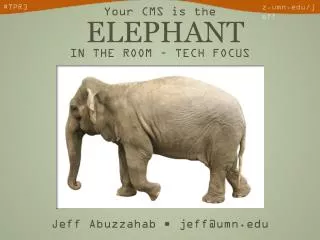

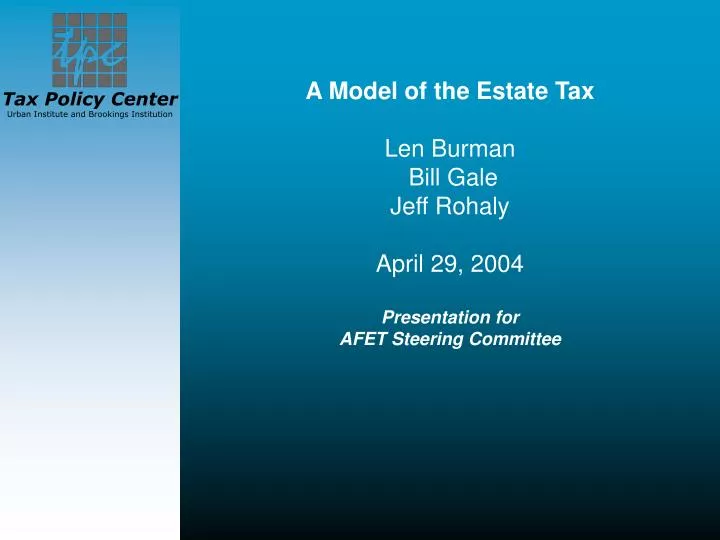

A Model of the Estate Tax Len Burman Bill Gale Jeff Rohaly April 29, 2004 Presentation for AFET Steering Committee. 2001*. $675,000. 60%. 2011. $1 million. 60%. Changes in Transfer Tax Exemptions and Rates Due to EGTRRA, 2002-2011. Highest Estate and Gift Tax Rates.

E N D

A Model of the Estate Tax Len Burman Bill Gale Jeff Rohaly April 29, 2004 Presentation for AFET Steering Committee

2001* $675,000 60% 2011 $1 million 60% Changes in Transfer Tax Exemptions and Rates Due to EGTRRA, 2002-2011 Highest Estate and Gift Tax Rates Calendar Year Estate and GST Tax Transfer Exemption 2002 $1 million 50% 2003 $1 million 49% 2004 $1.5 million 48% 2005 $1.5 million 47% 2006 $2 million 46% 2007 $2 million 45% 2008 $2 million 45% 2009 $ 3.5 million 45% 2010 N/A (taxes repealed) 35% (gift tax only) * Pre-EGTRRA law

Need for a Distributional Model • Necessary for evaluating burden of whole tax system • Calculate winners and losers under reform options

Modeling Strategy • Pretend all owe estate tax • Use SCF data to impute wealth, liabilities onto tax model • Calibrate to match published estate tax tabulations • Assign average level of deductions, credits • Calculate estate tax liability (if any) for each record • Use mortality probability to calculate expected estate tax

Estate Tax Computation • Gross Estate = Assets - Liabilities • Taxable Estate = Gross Estate - Deductions • Calculate Tentative Tax • Tax = Tentative Tax - Credits

Assets Imputed • Cash • Tax-exempt bonds • Taxable bonds • Stock • Retirement assets • Life insurance • Other financial assets • Vehicles • Personal residences • Other real estate • Farm assets + land • Active business • Passive assets • Other nonfinancial assets

Liabilities • Mortgage and home equity line of credit • Real estate debt • Farm debt • Credit card balances • All other debt

# dependents age brackets income taxable interest tax-ex interest dividends farm + business income rental income pension capital gains negative income zero dummies itemize schedule dummies Explanatory Vars

From NW to Estate • Randomly assign deductions • Married people--tax is optional • 80% don’t pay • assign average marital deduction to others • Assume maximum death tax credit

Modeling QFOBI • 1/5 of potential eligibles take it • We assign QFOBI randomly for baseline simulations • To estimate effect of QFOBI increases, we assume 100% take-up • Upper bound on cost

Two Measures of Income • Cash Income • AGI plus items excluded from income such as pensions, IRAs, health insurance, and transfers • Economic Income • Assumes imputed return to capital • Adjusted for family size

Economic Income is Better Measure • Many people with low or even negative realized income are extremely wealthy • Economic income says that if you have $10 million of stock, you are high income, even if you sell none of it and have business losses • But cash income is easier to explain to noneconomists

Permanent Revenue Options vs. Current Law10-Year Revenue Change

Permanent Options v. Permanent Baseline10-Year Estate Tax Gain