Download

1 / 6

60 likes | 90 Views

This article explores Amazon's potential vertical integration into parcel delivery, discussing implications, regulatory concerns, and strategic options for the tech giant.

E N D

Value Chain and Vertical Integration Edward S. Pearsall, discussant I am an economist and independent consultant. The views expressed here are my own and do not necessarily represent the opinions of the U.S. Postal Regulatory Commission (PRC).

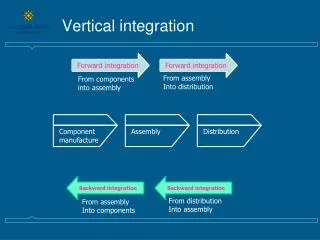

Amazon: The Elephant in the Room • Amazon at present: • Amazon largely relies on other firms for parcel distribution services. In the U.S., Amazon is by far the largest consumer of parcel delivery services offered by the U.S. Postal Service (USPS). These services are mostly supplied at non-public rates. The rates are set in Negotiated Service Agreements (NSAs) between Amazon and USPS that must be approved by the PRC. • There is little evidence that Amazon’s rates are more favorable than the rates offered other “similarly situated” venders through NSAs with USPS even though Amazon is much the largest of the group. The revenues USPS receives from various categories of parcel service NSAs covers the incremental costs of the service categories. • Amazon’s business is still growing rapidly. If Amazon is not yet large enough to capture the economies of scale necessary to operate its own in-house parcel delivery service, it soon will be. There is nothing about the delivery business except size that presents a significant barrier to entry. • It is just a matter of time before Amazon enters the parcel delivery business or otherwise seeks to lever its huge demand for delivery services to obtain preferential rates and services. • How could this happen? • Merger or acquisition. Amazon might attempt to vertically merge with or buy out an existing mid-sized private parcel service such as DHL or Federal Express. This would almost certainly precipitate a classic anti-trust suit a la AT&T/Time Warner in which the U.S. Justice Dep’t would argue that the result of the merger would be a combination with excessive market power. • Build its own delivery service. There are no barriers that would prevent Amazon from acquiring the trucks, terminals and labor force to build its own dedicated in-house delivery service. Amazon’s size is sufficient to provide the economies of scale needed to make this option attractive. It is also an option that competition authorities would find to be the most difficult to prevent. • Obtain preferential rates. Amazon might employ its monopsonistic market power to extract preferential rates and services from the existing venders. In the U.S. this would avoid the Justice Dept’s anti-trust division but would instead trigger complaints of anti-competitive practices with the Federal Trade Commission (FTC). This would invoke an entirely different process and set of remedies. • The papers taken together: • The papers each deal more-or-less tangentially with some aspect of the problem that Amazon will present to regulatory authorities in the U.S. and abroad when it eventually seeks to exploit its power in the market for parcel delivery services.

The Ongoing Evolution in Work-sharing in the US Postal Systemby Michael Plunkett • Work-sharing at present: • The paper provides an excellent description of the evolution of postal work-sharing in the U.S. Since 1970 USPS has offered more and successively deeper discounts to large mailers for unbundled component services (presorting, automation prep, drop shipping, palletization, et cetera; everything except delivery). • Historically, the discounts stimulated a large increase in USPS volumes between 1976 and about 1995. Since then the long term trend in volume has mostly been downwards except, recently, for parcels. • Currently, the discounts that USPS may offer for all kinds of work-sharing are governed by provisions of the Postal Accountability and Enhancement Act (PAEA). In general, PAEA limits discounts to USPS’s “cost avoided”, i.e. USPS’s marginal cost of performing the discounted component service. • PAEA’s discount limits are generally also observed in the NSAs that USPS negotiates with Amazon and its competitors. The discounts apply to Amazon mostly by eliminating everything but delivery service from the rates that Amazon pays. • What the paper should tell us: • The paper should tell us if PAEA’s discount provisions are distorting the postal pricing system. • There are reasons to believe that PAEA’s work-sharing discounts are too low (see Pearsall 2017, “PAEA’s Take on Regulatory Economics”). Second-best efficient discounts are above marginal cost. Also, discounted activities are cross-subsidized when performed by USPS unless the incremental cost of the activity equals or exceeds the discount. • If every component service except delivery is under-priced, then delivery service must be over-priced. This occurs because the price of a compound service is the sum of the prices of its components; and the price of a compound service must always cover incremental cost (aka attributable cost) in order to comply with PAEA’s pricing rules. • Back to Amazon: • Amazon will not enter the delivery business unless it believes that there is an opportunity to reduce its costs. • PAEA’s discount limits encourage Amazon to enter the delivery business by over-pricing delivery.

Platform Competition: Market Structure and Pricingby Helmuth Cremer, Claire Borsenberger, Denis Joram and Jean-Marie Lozachmeur • Is a vertical merger of a platform and a delivery service harmful? • The authors present a simple but serviceable model of two platforms, two services and a competitive fringe that is then used to answer the question for an assumed single scenario. • Welfare is derived for a base case where all participants independently maximize their profits. This is compared to welfare for various outcomes of a merger between one of the platforms and one of the delivery services. • The authors find that the merger should be prevented. The authors further speculate that in most similar circumstances a vertical merger is not in the public interest. • The model does not specifically describe the Amazon situation, however, it is sufficiently close to raise many red flags. Among other issues their simulations suggest that the merger enterprise may engage in additional anti-competitive practices and that the enterprises that are not part of the merger may exit their markets. • He How the model should be developed: • In its present form the model cannot be calibrated to numerically explore many specific situations such as an Amazon merger. The model includes just two parameters and has other severe structural limitations. • The model would be a good design for simulations if it can be generalized in several respects. To be generally useful it should allow for varying numbers of market participants, differences in the demand properties of the goods it defines, differences in costs among producers, et cetera. It should also allow us to model one of the delivery suppliers as a national post setting rates to maximize welfare subject to a breakeven condition. It would also be helpful to be able to evaluate other anti-competitive actions besides a merger and various kinds of regulatory responses. • The model could then be calibrated to specific scenarios and used within experimental designs that would reveal the welfare consequences of various public policies. • The Glass and Gori paper suggests to me that such a model could be used to explore various rules and legal tests that might be applied in practice to determine the legality of a vertical merger. For example, how much re-concentration of the market for services should be deemed unacceptable for anti-trust purposes? • Back to Amazon: • Hopefully, the generalized model could be calibrated to Amazon, its competitors and existing parcel delivery services including USPS. We could then experiment to find the most appropriate public response to whatever strategy Amazon adopts.

Approaches to Assessing Vertical Mergers: A Review and Evaluationby Victor Glass and Stefano Gori • What is the state of U.S. competition law vis-à-vis vertical combinations? • Vertical integrations are possible “combinations in restraint of trade” as defined by U.S. anti-trust law. The paper presents an us-to-date summary of the state of U.S. anti-trust enforcement w/r vertical mergers. • Observation: Anti-trust is a particularly difficult area for applied economics. Cases are likely to depend upon the outcomes of practical tests such as the SSNIP test accepted on the basis of prior case law. • The U.S. Justice Dep’t. is rewriting its standards w/r vertical mergers as the result of the outcome of the AT&T/Time-Warner case which the Justice Dep’t. effectively lost. • A merger of a platform and delivery service raises questions that are historically unusual but may be extremely important. For example, does a platform’s ability to collect and control the use of data confer an excessive competitive advantage on the merger enterprise? At present U.S. anti-trust practice scarcely considers such questions. • Back to Amazon: • Amazon is currently nibbling at the edges of U.S. competition law by incrementally and selectively entering the delivery business in ways that it probably hopes will not provoke an anti-trust proceeding. • An Amazon merger with a large parcel deliverer would be a vertical merger with disturbing parallels to the AT&T/Time-Warner case. It is hard to imagine that such a merger would not be considered against the public interest. • If the Justice Dep’t. brought an anti-trust case to forestall a merger, given the present state of disarray, it would probably either lose or settle short of preventing all of the resultant abuses of market power by Amazon. • Back to Glass and Gori: • My speculation: The crux of the matter is likely to be the harm caused to the delivery firms that are not merged with Amazon. What volumes and prices prevail with and without Amazon’s entry? What happens when Amazon exercises its monopsony power in the usual expected ways?

Questions for the Presenters • Michael Plunkett • Do you agree that USPS overprices delivery services? • Do you agree that PAEA’s discount rules are partly responsible? • Would changing PAEA’s discount rules be sufficient to discourage Amazon from entering the parcel delivery business? • Helmuth Cremer, Claire Borsenberger, Denis Joram and Jean-Marie Lozachmeur • Can your model be modified sufficiently to be calibrated present conditions in the U.S.? • Could a modified and calibrated model be used in a wide-ranging exploration of the potential welfare losses that would arise if Amazon is successful in entering the parcel delivery business on a large scale? • Do you believe that your present experimental findings would apply to an Amazon merger with, say, Federal Express? • Victor Glass and Stefano Gori: • What tools for analyzing evidence are needed to revive U.S. anti-trust practice as it would apply to an Amazon merger? • How generally should U.S. authorities deal with the other possible ways that Amazon may enter the parcel delivery business? • Would it be helpful for USPS to stop over-pricing package delivery? • Would it be helpful to explore alternative government responses to a proposed Amazon merger using a simulator designed along the lines of the Cremer et al model?