Download

1 / 21

210 likes | 285 Views

Capital Structure: Theory And Taxes. Professor XXXXX Course Name / Number. Capital Structure. Can a firm increase its value by choosing the right mix of debt and equity (i.e., the right capital structure) to finance its operations?.

E N D

Capital Structure: Theory And Taxes Professor XXXXX Course Name / Number

Capital Structure Can a firm increase its value by choosing the right mix of debt and equity (i.e., the right capital structure) to finance its operations? Capital structures vary across firms, industries, and countries. Is debt better than equity because it is cheaper? Is equity better than debt because firms that borrow may go bankrupt?

Evidence on Capital Structure 1) More profitable firms tend to use less leverage. 2) High-growth firms borrow less than mature firms do. 3) Firms’ product market strategies and asset bases influence capital structure choice. 4) Stock market generally views leverage-increasing events positively. 5) Tax deductibility of interest gives firms an incentive to use debt.

Company Debt to total assets L-T debt to total capital Market to book ratio Microsoft 0 0 5.54 Intel 0 0 4.03 ExxonMobil 0.04 0.03 3.72 Procter & Gamble 0.12 0.07 10.13 Boeing 0.27 0.24 3.65 Walt Disney 0.27 0.25 1.92 American Electric Power 0.54 0.36 1.62 Georgia Pacific 0.69 0.55 1.19 Delta Air Lines 0.77 0.75 0.82 General Motors 0.84 0.83 4.12 Market Value Debt Ratios, Selected U.S. Corporations, July 2002 Source: Firm-specific data taken from each company’s financial information at http://money.cnn.com of June 12, 2002.

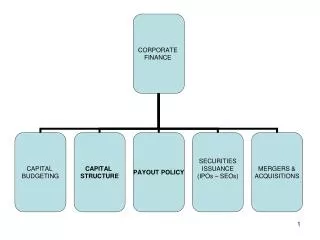

Theoretical Models Of Capital Structure Modigliani and Miller’s (M&M) capital structure model The agency cost/tax shield trade-off model The pecking order theory The signaling model

Firm value is determined by: Key insight Cash flows generated Underlying business risk The M&M Capital Structure Model First model to show that capital structure decision may be irrelevant Assumes perfect markets, no taxes or transactions costs Capital structure merely determines how cash flows and risks are allocated between bondholders and stockholders.

M&M Proposition Proposition I: Market value of a firm is driven by two factors: cash flow and risk (determines the discount rate). The mix of debt and equity merely determines how the cash flows and the risks are divided. Proposition II:The expected return on a levered firm’s equity, rl, is a linear function of firm’s debt to equity ratio. Though the cost of debt is lower than the cost of equity, substituting debt for equity causes the cost of equity to rise, negating any cost savings from the switch.

Firms U and L belong to same risk class and have same expected EBIT $2,000,000 per year in perpetuity. Firm U has no debt. Firm L has both debt and equity. Required return r for firms of this risk class is 10%. M&M Proposition I Use arbitrage arguments to prove proposition I Proposition I: Market value of a firm is driven by two factors: cash flow and risk (determines the discount rate). Under proposition I, market value of firms U and L should be identical.

$20,000,000 $20,000,000 M&M Proposition I Market value of assets should be $20,000,000 Market value of firm U = 1,000,000 x $20 = $20,000,000 Market value of firm L = 500,000 x $20 + $10,000,000 = $20,000,000

Firm U has no debt Required return on equity equals required return on assets of 10% Required return on equity = 10% Firm L pays $600,000 interest. EBIT is $2,000,000 Shareholders receive a cash dividend of $1,400,000, or $2.80/share. Share price = $20. Required return on equity = $2.80/$20 = 14% M&M Proposition I What is the return the shareholders of the two firms expect on their shares?

M&M Proposition I What if the shares of the levered firm are selling at premium? Assume the stock price of firm L is $25. $25 $22,500,000 Total firm value increases to $22,500,000. The price of $25 per share implies a return of $2.80/$20 = 0.112. 0.112 Firm L stockholders can use “homemade leverage” to generate arbitrage profit.

The investor owns 1% of firm L. • He earns $2.80 per share in dividends. • The shares will generate $14,000 each year. Assume investor owns 5,000 shares of firm L Borrow an amount equal to 1% of firm L debt Sell 5,000 of firm L at $25 per share • $100,000 at 6% interest • Proceeds of $125,000 Buy 1% of firm U equity • 10,000 shares at $20 per share M&M Proposition I The investor could earn an arbitrage profit from the following:

$2 dividend per share of firm U, $20,000 for 10,000 shares • $6,000 interest expense on borrowed money • $14,000 cash inflow next year on the new portfolio The net return on the new portfolio The same return expected on the original 1% stake in firm L's shares! The cost of building this portfolio is just $200,000 , $25,000 less than the cost of 5,000 firm L shares. M&M Proposition I Using homemade leverage, investor has built a portfolio of $200,000 of firm U's stock and $100,000 in personal debt. Investor has $25,000 remaining.

Required return on firm’s assets Required return on equity Required return on debt Firm U return on equity Firm L return on equity M&M Proposition II Proposition II:The expected return on a levered firm’s equity is a linear function of firm’s debt to equity ratio.

Proposition II rearranged is just the WACC : Firm U WACC Firm L WACC M&M Proposition II If proposition II holds, WACC is independent of capital structure.

Required Return r + (r - rd)D/E rl (cost of equity) WACC r rd (cost of debt) D/E (debt to equity ratio) Firm’s Cost Of Equity Under M&M Proposition II

M&M with Taxes 1) Most countries allow firms to deduct interest as an expense, but not dividends. 2) Deductibility lowers the after-tax cost of debt. 3) By using more debt, firms shelter more cash flow from taxes. 4) Maximum firm value is reached at 100% debt.

Taxes 10% Equity 10% Debt 25% Taxes 25% Debt 80% Equity 50% Models Of Capital Structure: With Corporate Income Taxes

The M&M Model With Corporate And Personal Taxes Incorporating corporate income taxes yields a straight-forward result: use 100% leverage. • Two obvious candidates: personal taxes and deadweight costs of corporate bankruptcy • Perhaps personal taxes offset corporate taxes. • Direct bankruptcy costs are small, indirect costs are larger but not large enough. • Equity has a personal tax advantage (capital gains and sometimes dividends taxed at lower rates than interest income). This is not observed in the market. How can we explain that firms use less than 100% debt?

Gains from leverage Miller (1977) And The Gain From Leverage Miller proposed a model where corporate tax benefits of leverage are partially or fully offset by personal taxes. Tc = Tax rate on corporate profits Tps = Personal tax rate on income from stock (capital gain and dividends) Tpd = Personal tax rate on income from debt (interest income) D = Market value of a firm's outstanding debt This is a general formulation. It includes original no-tax model as special case, where GL=0. Also includes case with only corporate taxes.

Capital Structure: Theory And Taxes Capital structures vary across firms, industries, and countries Modigliani and Miller showed that in a world of frictionless capital markets capital structure is irrelevant Most of the assumptions of M&M model have been successfully weakened