Download

1 / 4

40 likes | 214 Views

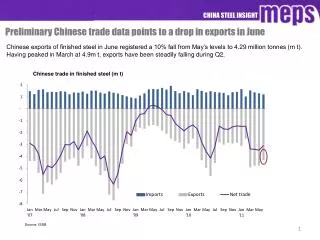

CHINA STEEL INSIGHT. Preliminary Chinese trade data points to a drop in exports in June. Chinese exports of finished steel in June registered a 10% fall from May’s levels to 4.29 million tonnes (m t). Having peaked in March at 4.9m t, exports have been steadily falling during Q2.

E N D

CHINA STEEL INSIGHT Preliminary Chinese trade data points to a drop in exports in June Chinese exports of finished steel in June registered a 10% fall from May’s levels to 4.29 million tonnes (m t). Having peaked in March at 4.9m t, exports have been steadily falling during Q2. Chinese trade in finished steel (m t) Source: ISSB

CHINA STEEL INSIGHT Detailed trade data for May shows falling demand in key Asian export markets China’s finished steel exports have fallen most substantially in key Asian export markets amid softening domestic demand in the region. Bookings from Europe have taken up some of the slack. Exports to Belgium rose 72% month-on-month (m-o-m) in May to 269,000 t. These levels are unlikely to be sustained in the coming months, however. Chinese exports of finished steel (m t) (RHS) Source: ISSB

CHINA STEEL INSIGHT Chinese/world price differential points to further weakness in exports The Chinese/world HRC price differential, which is closely related to export levels, has fallen markedly in recent months. We anticipate that this will continue to limit export bookings in the short term. Finished steel exports (m t) v. China/world HRC price differential ($/t) Source: ISSB, Mysteel, MEPS

CHINA STEEL INSIGHT Spot prices continue to surge Spot prices ended last week strongly, with the biggest gains recorded in rebar. These rose RMB 60/t (US$ 9/t) to RMB 4680/t. HRC was up RMB 10/t to RMB 4810/t. Although demand remains soft as steel consumption slows going into the summer months, prices have received support from a positive outlook for demand in the autumn. Orders of construction steel are expected to remain high amid an expected acceleration of economic housing projects. Last week’s raising of benchmark interest rates and the sharp rise in the consumer price index to 6.4 for June, have both been interpreted as positive for future steel demand. Many believe that inflation has now peaked and that government policy is now likely to be less focused on tightening monetary supply. This positive outlook is reflected in the surging price of the first forward month contract for rebar on the Shanghai Futures Exchange. This optimism is partly shared by steel mills. Baosteel and Wugang Iron and Steel have both frozen list prices of commodity grade HRC for August delivery. Shanghai Futures Exchange, rebar first forward month contract (RMB/t) HRC and rebar spot prices (Shanghai, RMB/t including 17% VAT) Source: SFX Source: Mysteel