Download

1 / 25

250 likes | 418 Views

Korea’s Financial Reform: A Systemic Risk Approach. Jang-Yung Lee Senior Counselor to the Deputy Prime Minister Ministry of Finance and Economy Republic of Korea. November 2002. 2. Korea’s Financial Reform : A Systemic Risk Approach. Overall Assessment of Reforms

E N D

Korea’s Financial Reform:A Systemic Risk Approach Jang-Yung Lee Senior Counselor to the Deputy Prime Minister Ministry of Finance and Economy Republic of Korea November 2002

2 Korea’s Financial Reform :A Systemic Risk Approach • Overall Assessment of Reforms • Financial Restructuring: Banking vs. Non-banking financial sector • Corporate sector vulnerability • Conclusion : Remaining reform agenda

3 Questions to be answered • What are the lessons to be drawn from Korea’s post-crisis reforms? • Were the sequence and pace of the reforms appropriate? • Were Korea’s reform strategy properly formulated to deal with the systemic risks? • How serious is the systemic threat currently posed by weak corporate sector?

4 Initial policy responses • Liquidity support by the BOK • A blanket guarantee for depositors • Institutional Infrastructure: => FSC, KDIC, KAMCO • Resolution strategy consulted with IMF and IBRD • Socio-political consensus on financial reforms and fiscal support plan

5 A Systemic Risk Approach • Prioritize the government-led restructuring of financial institutions, based on their systemic importance • Deposit-taking intermediaries first: =>a greater risk to the payment system • Prioritize the banks with the greatest systemic importance

6 Resolution of weak banks • Two large commercial banks: Jan.’98 • Five small banks: July.’98 • Remaining seven undercapitalized banks: Jan.’99-Sep.’99 • Various forms of restructuring in the banks that were not undercapitalized

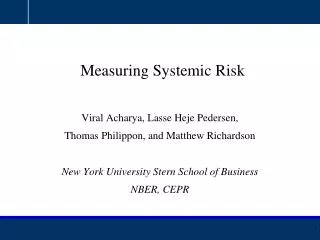

7 Speed of banking sector restructuring • Swift move to recapitalize: meet the 6% CAR by Mar.’99, and 8% CAR by Mar.’00 • Adhered to the tighter CAR even when the banking system returns to normalcy • Prompt mobilization and injection of the public funds: W 137.5 trillion

8 Use of Public Funds in Financial Restructuring

9 Restructuring of non-banking financial sector • Priority given to the closure of 17 merchant bank sector: large exposure to FX risk • A tightening of investment guidelines for insurance companies • Relatively lax supervisory framework for investment trust companies(ITC), even though the weakest among the non-banks => posed the significant systemic risk

10 Asymmetric Restructuring • Regulatory forbearance for the non-bank financial institutions • Exceptional growth of ITC’s trust assets: July ’98- August ’99 <= Driven by a sharp fall in interest rates + by the lax supervisory oversight • Continued to be used as a financing vehicle by the large companies => reduced the pressure on corporate sector restructuring

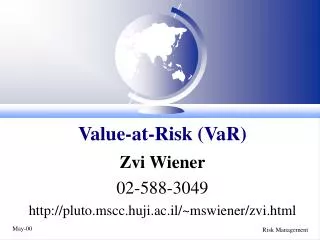

11 Figure 1. Trust Assets of Investment Trust Companies(Unit: W100 billion)

12 ITC’s liquidity problems • Triggered by Daewoo’s debt servicing problems in mid-1999: held 80% of Daewoo’s domestic bonds • Public confidence further damaged by illegal marketing practices, poor accounting standards, and maturity mismatch • Redemption pressure increased

13 Stabilization of ITC industry • Restrict ITC fund redemption: could receive only 50% of Daewoo portion of their investment if withdrawn before Nov.’99 • Create bond market stabilization fund • Public bail-out of two largest ITCs • Intervention justifiable based on the market’s failure to respond appropriately • Systemic risk: event risk or refinancing risk

14 Corporate Sector Restructuring • Pursued simultaneous restructuring of the financial and corporate sector • Slow pace of corporate restructuring, due to weakened reform momentum in early 2000 • Weak accounting and disclosure standards • Poor risk management in both firms and banks • Inadequate legal and judicial framework for court-supervised insolvency procedures

15 Macroeconomic vulnerability • Smooth macroeconomic adjustment • Success of IMF-supported stabilization program-> external position no longer a systemic threat by early 1999 • Evidence of reduced vulnerability: no exchange rate misalignment, balance between foreign exchange reserves and domestic money, and normal rate of credit growth

16 Figure 2. Credit Ratings of Korean Firms (Share by the Ratings)(Unit: percentage)

17 Renewed credit crunch in the last quarter of 2000 • Collapse in corporate bond market-> increased refinancing risk • Heavy concentration of maturing corporate bonds in early 2001 (W 65 tril. 13 % of GDP) • Demise of merchant banks and shrinkage of ITC as the main investors • Absence of active high-yield (junk bond) market • Perception of high credit risk -> almost 70 % of maturing corporate bond not renewable

18 Quick underwriting scheme • Primary CBO market to facilitate the revolving of the sub-investment grade bonds • Let the KDB underwrite 80% of the maturing corporate bonds with sub-inv. grade • WTO issue: no specificity => non-actionable subsidies • Assistance strictly limited to economically viable companies: importance of solvency analysis by the main creditor bank • Penalty rate (260 bp) to avoid moral hazard

19 After the quick underwriting scheme • Market sentiment improved-> Bond market ceased to be a systemic concern • Liquidity pressure not likely • =>Absorptive capacity of the primary CBO (W 6.0 tril.) large enough to deal with the maturing sub-investment grade bonds (W 5.3 tril.)

20 Corporate vulnerability • Profitability still constrained by large debt burden • Recessionary shock will lead to further strains • 29 % of manufacturing companies have an ICR of less than one • Chronically insolvent companies (ICR of less than one for three consecutive yrs): 4 % of Korean companies • Total liabilities issued: W 10 trillion, only 2.7 % of banking system’s asset • Do not pose a systemic threat to the rest of the economy => calls for acceleration of corporate restructuring

21 Remaining challenges • Orderly exit of the insolvent firms • Need insolvency reform to harmonize three bankruptcy-related laws • Make the Constant Restructuring System work more forcefully => Early privatization of the nationalized banks => Promote active M&A market; => Strengthen corporate governance; => More rigorous bank accounting standards;

22 Table 1. Public Funds Injected (Nov.1997~Jun.2002) Source : Ministry of Finance and Economy, Public Fund Management Committee (August 2002), White Paper on Public Fund Management

23 Table 2. Estimate of Recollectable Fund (unit: tril.KRW) Spent (A) Recollection (B) Recollection Ratio (B/A) Total Spent 156 Already recollected(’02.3) : 42 26.9% + + Recollectable in Future : 45(41~49)1) 26.1%+31.2% KDIC . KAMCO • Sale of equity-stake : 13.1~18.4 • Bankrupt asset sales : 3.1~ 3.3 • Sale of NPLS : 7.8~10.3 • Sub total : 28.0(24.0~32.0) Fiscal A/C • -Subordinate Debt value held by • gov’t (100% recollectable) : 6.4 • Book-value of equity-stake at • Specialized banks : 10.3 • (KDB, KEXIM, IBK) • Sub total : 16.7 Total Recollection : 87 55.6% Non Recollectable(A-B) : 69 1) Present discounted

24 Table 3. Closures and Mergers of FIs (1997-2002) Note: 1) Merchant Banks, Investment Trust Funds, Mutual Funds, Credit Unions, Lease companies, etc. Sources : Financial Supervisory Service(FSS)

P&A Disapproved Resolution BIS Capital Ratio<8% 12 Problem Banks Evaluation M&A Rehabilitation Plan Diagnostic Review Approved Rehabilitation Plan Dispose NPLs Sound Banks BIS Capital Ratio>8% 13 Banks Public Resources Diagnostic Review Recapitalize Asset Assessment Lead Manager Bidding Privatize SB/KFB 25 Figure 3. Bank Restructuring flow