Download

1 / 31

320 likes | 557 Views

Basics of Retirement Investing. Date February 2009 Presented by: Vernon Stockton – ICMARC . AC: 0506-758. Today’s Discussion. Setting Goals Basic Concepts. Why is Investment Education Important?. Reaching retirement goals is a two-step process

E N D

Basics of Retirement Investing Date February 2009 Presented by:Vernon Stockton – ICMARC AC: 0506-758

Today’s Discussion • Setting Goals • Basic Concepts

Why is Investment Education Important? • Reaching retirement goals is a two-step process • Step #1: Participate in your employer-sponsored retirement savings programs • Put enough money away for the future • Most experts say you will need between 70% to 80% of your salary when you retire • May differ based on your situation and retirement plans

Why is Investment Education Important? • Reaching retirement goals is a two-step process • Step #2: Invest contributions wisely • Compounding: Earn money on the principle plus all previous earnings • Over time, retirement assets may grow more through earnings than amount initially contributed • Must develop investment strategy and actively manage investments

You don’t have to be an Expert • What you do need is a basic understanding of: • Common investment concepts • Types of investment vehicles • Resources available to you through ICMA-RC • Personal Assistance • Your ICMA-RC Investment Options1 1 See disclosure at the end of this presentation.

Investment Concepts • Risk • Managing risk through diversification • Focus on the long term • Steady investing

Risk • How confident can you be in expected returns? • More volatile and unpredictable, more risky the investment • Every investment carries some level of risk • Risk/return trade off • Match your financial goals with the level of risk you’re willing to accept • More risk = More reward over time • Less risk = Less reward over time

Managing Risk Through Diversification • Spread risk by investing in different funds and types of investments • Diversification protects against down-side risks and maximizes potential for returns • Helps smooth out ups and downs of market • Takes advantage of market swings • Investments react differently to market conditions • Bonds usually up when stocks are down • Inflation and interest rate change

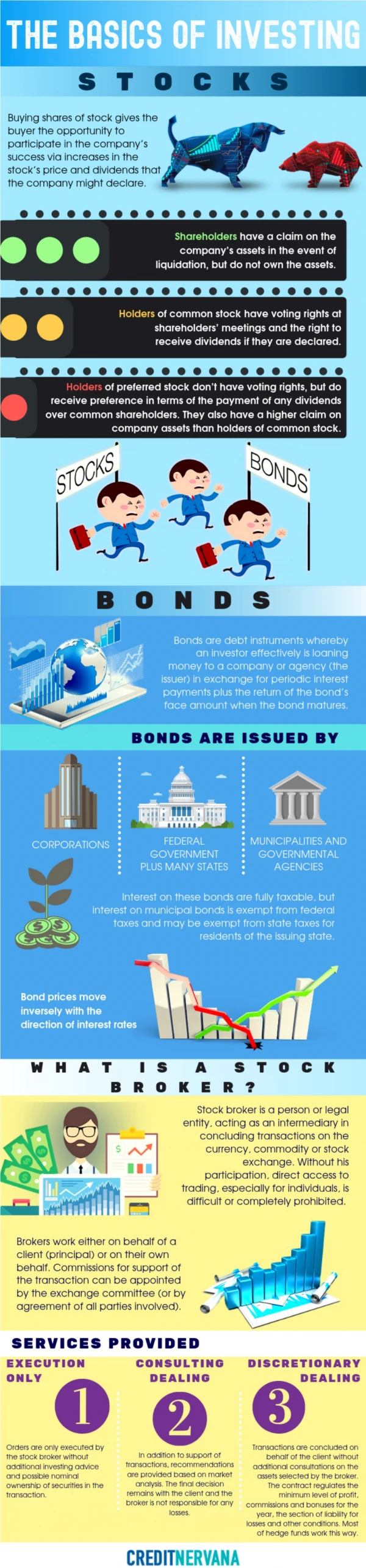

Mutual Funds are Diversified Funds • Funds that are invested in a variety of industries/companies/locations • Money of many investors is “pooled” • Large blocks of securities purchased • Professionally managed by investments experts • Research and assess market trends • Make buy/sell decisions • Types • Stock Funds • Bond Funds • Balanced/Asset Allocation Funds • Index Funds • Specialty Funds

Investment Options Stock Funds • Stocks (equities) are ownership interest in a company • “Share price” of the stocks in the fund and reinvestment of any dividends • Stock funds • Different funds concentrate on specific factors • Growth stock funds: strong earnings growth • Equity income funds: strong dividend history • International funds: overseas companies • Actively managed • Buy and sell decisions about which securities are in the funds

Investment Options Bond Funds2 • Bonds are “loans” to corporations and the federal government (treasury securities) • Bond funds • Not federally guaranteed • Professional management is essential • Not traded on the Stock exchange • Selected from different issuers, maturities, types of bonds • Less risky then stock funds • Value up when interest rates are lower 2 See disclosure at the end of this presentation.

Investment Options Balanced/Asset Allocation Funds • Balanced funds • Balance volatility and return with a mix of stocks, bonds, cash • Mix consistent; actual funds may be actively traded • Asset allocation funds • Managers shift money among stocks, bonds and short-term cash investments

Investment Options Index Funds and Specialty Funds • Index funds • Hold same securities in the same proportion of specific market index like S&P 500 • Not actively managed • Specialty funds3 • One specific segment of the market (financial, technology) • Small area of concentration • More risk 3 See disclosure at the end of this presentation.

Investment Options Stable Value Funds • Stable value contract • Specific rate of return promised by financial entity like an insurance company • Stable value funds by contracts • No price fluctuation, no market risk • More conservative investment with lower rate of return

Annual Returns for Market Indexes 1987 to 2005 Source: Ibbotson AssociatesSee key on the following slide.

Glossary S&P 500 Index measures the performance of large capitalization U.S. stocks. The S&P 500 is a market-value-weighted index of 500 stocks that are traded on the NYSE, AMEX and NASDAQ. The weightings make each company's influence in the Index performance directly proportional to that company's market value. Wilshire 4500 Index measures the performance of all small- and mid-cap stocks and is constructed using the Wilshire 5000 Index with the securities of the S&P 500 Index removed. Wilshire Large Cap Growth and Wilshire Large Cap Value indices measure performance of the growth and value styles of investing in large-cap U.S. stocks. Widely regarded as one of the standards for measuring large-cap U.S. stock market performance, the index includes a representative sample of leading companies in leading industries. Large companies in the Wilshire 5000 are made of the top 750 stocks of the overall index and are split into two indices: the Value Index based on price/earnings ratio, price-to-book ratio and yield, and the Growth Index which groups companies with at least five years of history based on sales, growth rate, return on equity, and dividend payout. Wilshire Small Company Growth and Wilshire Small Company Value measure the performance of growth and value styles of investing in small-cap U.S. stocks. The same variables as above are used to characterize the stocks as value or growth. MSCI EAFE is a Morgan Stanley Capital International index that is designed to measure the performance of the developed stock markets of Europe, Asia, and the Far East. LB Agg is the Lehman Brothers Aggregate Bond index. This index includes U.S. government, corporate and mortgage-backed securities with maturities up to 30 years. *You cannot invest directly in these indices therefore; their performance does not reflect the expenses associated with the management of a portfolio of open-ended investment company shares. This information is being provided for educational purposes only and is not intended to be construed as or relied upon as investment advice. This information is not intended to be construed as a solicitation for particular product or security. Performance reflected above represents past performance. Investment returns and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Past performance is not indicative of future returns. Individuals are advised to consider any new investment strategies carefully prior to implementing.

What is Your Time Horizon? • Retiring in less than 10 years? • Allocate a larger portion of assets in less risky investments • Less short-term fluctuation • Growth slower but more predictable • Retirement more than 10 years away? • Generally the more time before retirement, the more aggressive investments can be • More short-term ups and downs but over time, volatility (risk) is reduced

Patience is Key • Stock and bond markets are unpredictable • Timing the market difficult, even for seasoned professionals • When to get out? When to get back in? • Short-term changes are less important than long-term trends • Regardless of market fluctuations, consistently invest the same amount of money on a regular basis (Dollar Cost Averaging4) 4 See disclosure at the end of this presentation.

Dollar Cost Averaging4 Investing $2,400 Over A Four Month Period Dollar Cost Averaging buys 90 shares Average Market Price buys only 84.2 shares Amount Price/ # ofMonth Invested Share Shares Jan $600 $20 30 Feb $600 $30 20 Mar $600 $24 25 Apr $600 $40 15 Total $2400 90 Average Share Price = $28.50 Average Cost Per Share Price = $26.67 Savings: $1.83 Per Share Example is for illustration purposes only and is not intended to represent an actual account. 4 See disclosure at the end of this presentation.

Putting it All Together Building Your Portfolio • Start by participating in your employer sponsored retirement savings plan • Contribute as much as you can afford • Your most important decision is asset allocation • Percentage of assets invested in type of fund • Factors to consider • What is your timeline? • Is your portfolio diversified? • Do you understand the risks of your investments? • Too safe? Too aggressive?

Investment Solutions Three different investors I will need my assets in the year… –Milestone Funds Single Fund Solutions I want to look at risk… –Model Portfolio Funds I want to build a custom line-up… Three different solutions.

I will need my assets in the year… Option One – Milestone Funds1 Ideal for people that want to make one simple fund selection for the long-term Target Retirement Date 35 years 30 years 25 years 20 years 15 years 10 years 5 years Years to Planned Retirement Date Fixed Equity 1 See disclosure at the end of this presentation.

I want to manage risk… Option Two –Model Portfolios Funds1, 5 Ideal for people that understand their risk profile and want to annually monitor their account SavingsOriented6 ConservativeGrowth TraditionalGrowth Long-termGrowth All-EquityGrowth Conservative Risk High Risk Fixed Equity 1, 5-6 See disclosure at the end of this presentation.

I want to build a custom line-up… Option Three –Customized Investing1, 7 Value Blend Growth Large Cap: > $10.5 B Mid Cap: $1.7 B - $10.5 B Small Cap: < $1.7 B 1, 7 See disclosure at the end of this presentation.

Your ICMA-RC Investment Options1, 7 Single Fund Solutions Customized Investing I want to build a custom line-up… I will need my assets in the year… VANTAGEPOINT MILESTONE FUNDS Milestone Retirement Fund Milestone 2010 Fund Milestone 2015 Fund Milestone 2020 Fund Milestone 2025 Fund Milestone 2030 Fund Milestone 2035 Fund Milestone 2040 Fund I want to manage risk… VANTAGEPOINT MODEL PORTFOLIO FUNDS5 Savings Oriented7 Conservative Growth Traditional Growth Long-Term Growth All-Equity Growth 1-3, 5-14 See disclosure at the end of this presentation.

Family of Funds1, 7 I will need my assets in the year… I want to manage risk… I want to build a custom line-up… 29 1-3, 5-14 See disclosure at the end of this presentation.

How We Can Help Local Representative Phone ICMA-RC Web site Your Account Statement • Series 7, 63 and 65 licensed • Answer questions and help fill out enrollment forms • Retirement planning worksheets and materials • Location visits on a regular basis or contact me directly • Ongoing presentations focusing on the basics of investing • Account inquiries • Answer questions • Resolve Issues • Transactions • Address changes • Other customer service-related issues • ICMA-RC Investor Services: 1-800-669-7400 • Automated services 24 hours a day, 7 days a week • Investor Services representative Monday – Friday between 8:30am and 9:00pm ET • www.icmarc.org • Check account balance • Make transactions • Fund information • Additional helpful tools and services • Mailed 10 business days after quarter end • Provides: • Account summary • Personalized performance • Account balance charts • Fund information Contact Info:Vernon Stockton800-669-7400

Top Investment Tips • Payroll deduction makes investing automatic • Invest a regular dollar amount • Take advantage of tax-deferred investing • Think about your risk tolerance • Diversify • Invest in what you understand • Invest for the long haul • The power of time – compounding • Retirement assets are for retirement!

Next Steps Building Your Portfolio • Take control today • Start enrolling • Review your current asset allocation • Understand your investments and plan rules • Set up an appointment

Please consult both the current applicable prospectuses and MAKING SOUND INVESTMENT DECISIONS: A Retirement Investment Guide carefully for a complete summary of all fees, expenses, charges, financial highlights, investment objectives, risks and performance information. Investors should consider the Fund’s investment objectives, risks, charges and expenses before investing or sending money. The prospectus contains this and other information about the investment company. Please read the prospectus carefully before investing. ICMA-RC’s proposed fund line-up is a commitment to administer these funds for the plan, not advice to the plan sponsor on the composition of the plan’s fund line-up. ICMA-RC provides plan sponsors fund information to assist them in meeting their fiduciary responsibility in managing the plan. The plan sponsor retains the obligation to prudently select and monitor the investment funds it offers to plan participants. ICMA-RC may adjust fees commensurate with changes in revenue from alternative funds selected by the plan sponsor from ICMA-RC’s mutual fund platform. Vantagepoint securities are distributed by ICMA-RC Services LLC, a broker dealer affiliate of ICMA-RC, member NASD/SIPC. For a current prospectus, contact ICMA-RC Services LLC, 777 North Capitol Street NE, Washington, DC 20002-4240. 1-800-669-7400. A rise/fall in the interest rates can have a significant impact on bond prices and the NAV (net asset value) of the fund. Funds that invest in bonds can lose their value as interest rates rise and an investor can lose principal. Funds that concentrate investments in one industry may involve greater risks than more diversified funds, including greater potential for volatility. Dollar Cost Averaging Plans do not assure profit or protect against loss in a declining market. Since Plans involve continuous investment, regardless of fluctuating prices, investor must consider financial ability to continue to invest during low price levels. The asset allocation of the Model Portfolios was rebalanced when the Income Preservation Fund was replaced by the Short-Term Bond Fund on November 9, 2004. Because of its high allocation to fixed income, the Fund may be appropriate for investors with a low risk tolerance and shorter investment horizon. However, because the Fund invests one quarter of its assets in stocks, the Fund may offer higher growth potential and inflation protection than an all-bond portfolio. A redemption fee may be assessed when participants sell shares within proposed funds. Please refer to the fund prospectuses for guidance on redemption fee and market timing terms. Invests solely in the Lord Abbett Affiliated Fund. Closed to new plan sponsors. Disclosures

Small/Mid Cap: Funds that invest in small and/or mid-sized company stocks typically involve greater risks, particular in the short-term than those investing in large, more established companies. Investments in the Vantagepoint Money Market Fund are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund. Vantagepoint securities are distributed by ICMA-RC Services, LLC, a broker-dealer affiliate of ICMA-RC, member NASD/SIPC. 1-800-669-7400. Because there is no trading market for investment contracts, PLUS Fund returns consist of yield only. Returns are annualized for ease of comparison with other stable value investments. Please consult the current MAKING SOUND INVESTMENT DECISIONS: A Retirement Investment Guide for additional information on the VantageTrust PLUS Fund including trading and transfer restrictions. 1-800-669-7400. International: Foreign investments are subject to more risks not associated with domestic investments (I.e. currency, economy and political risks.) Investors who transfer assets out of these Funds must wait at least 91 days before transferring assets back into the same Funds. The policy affects transfers only. It does not affect regular contributions or disbursements. Disclosures