Download

1 / 46

460 likes | 633 Views

A Review of the Accounting Cycle. Learning Objectives. Identify and explain the basic steps in the accounting process (accounting cycle). Analyze transactions and make and post journal entries. Make adjusting entries, produce financial statements, and close nominal accounts.

E N D

Learning Objectives • Identify and explain the basic steps in the accounting process (accounting cycle). • Analyze transactions and make and post journal entries. • Make adjusting entries, produce financial statements, and close nominal accounts. • Distinguish between accrual and cash-basis accounting.

Learning Objectives • Discuss the importance and expanding role of computers to the accounting process. EXPANDED MATERIAL • Use special journals and subsidiary ledgers to process accounting information more efficiently and to provide additional useful information.

The purpose of this chapter is to review the basic steps of the accounting process.

Double-Entry Accounting or A = L + OE A system of recording transactions in a way that maintains the equality of the accounting equation. Assets = Liabilities + Owners’ Equity

Double-Entry Accounting Facts • For every transaction, there must be at least one debit and one credit. • Debits must always equal credits for each transaction. • Debits are always entered on the left side of an account and credits are always entered onthe right side.

The Accounting Equation with T-Accounts Assets = Liabilities + Owners’ Equity DR CR + - DR CR - + DR CR - +

Capital Stock Retained Earnings DR CR DR CR - + - + Expenses Revenues Dividends DR CR DR CR DR CR + - - + + - How Accounts Affect Owners' Equity Owners' Equity DR CR - +

Journalizing • Identify the accounts involved with an event or transaction. • Determine whether each account increased or decreased. • Determine the amount by which each account was affected. This process is used whether the accounting is being done manually or with a computer.

1. Analyze Transactions and Business Documents • Transactions are the exchange of goods or services between entities, as well as other events that have an economic impact on a business. • Business Documents are records that are evidence of transactions.

2. Journalize Transactions • A journal is an accounting record in which business transactions are entered in chronological order. • Journal entries record transaction information; debits equal credits.

Journal Entries • A journal is an accounting record in which business transactions are entered in chronological order. • Journal entries record transaction information; debits equal credits. General Journal Entry Format Date Debit Entry.................................. xx Credit Entry............................. xx Explanation.

Post Ref. Journal Page 1 Date Description Debits Credits Jan 1 Cash 5 Revenue 5 Received cash for services provided. 4 Supplies 12 Accounts Payable 12 Purchased supplies on account. 10 Accounts Payable 12 Cash 12 Paid for supplies.

Example: Journal Entry Merchandise is sold to a customer on account for $75. The cost of the product to the firm is $60. Make the journal entry.

Example: Journal Entry Merchandise is sold to a customer on account for $75. The cost of the product is $60. Make the journal entry. Merchandise is sold to a customer on account for $75. The cost of the product to the firm is $60. Make the journal entry. Jan. 1 Accounts Receivable..................... 75 Sales Revenue.......................... 75 Sold merchandise on account. 1 Cost of Goods Sold...................... 60 Inventory................................. 60 To record cost and reduce inventory.

3. Post Journal Entries to Accounts • Posting is the process of transferring amounts from the journal to the general ledger. • A ledger is a book of accounts in which data from transactions recorded in the journals are posted, classified, and summarized. • A chart of accounts lists all accounts used by the company.

Chart of Accounts Long-Term Liabilities (220-239) 222 Mortgage Payable OWNERS’ EQUITY (300-399) 301 Capital Stock 330 Retained Earnings SALES (400-499) 400 Sales Revenue EXPENSES (500-599) 500 Cost of Goods Sold 523 Rent Expense 528 Advertising Expense 573 Utility Expense ASSETS (100-199) Current Assets (100-150) 101 Cash 105 Accounts Receivable 107 Inventory Long-Term Assets (151-199) 151 Land 152 Building LIABILITIES (200-299) Current Liabilities (200-219) 201 Notes Payable 202 Accounts Payable

The Reporting Phase • A trial balance is prepared. • Adjusting entries are recorded. • Financial statements are prepared. • Closing entries are made. • Post-closing trial balance may be taken.

4. Determine Account Balances and Prepare a Trial Balance • Determine the account balance for each T-Account. • A Trial Balance is a listing of all account balances. It provides a means to assure that debits equal credits.

XYZ Company Trial Balance December 31, 2002 DebitsCredits Cash $ 21 Accounts Receivable 15 Inventory 12 Land 200 Accounts Payable $ 30 Capital Stock 150 Retained Earnings 24 Sales Revenue 919 Cost of Goods Sold 850 Advertising Expense 10 Misc. Expenses 15 ______ Total $ 1,123 $ 1,123

5. Adjusting Entries Adjusting entries are requiredat the end of each accounting period for accrual-basis accounting, prior to preparing the financial statements. The purpose for adjusting entries are to: • Bring balance sheet accounts current. • Reflect proper amounts of revenues and expenses on the income statement.

Tips Regarding Adjusting Entries • Analytical Process. You must determine what original entry was made (if any) and what the ending balances should be before you know what adjusting entry to make. You cannot memorize adjusting entries. • Adjusting entriesalways incorporate a balance sheet account and an income statement account. • Adjusting entries neverinvolve a cash account.

Most Common Adjusting Entries • Unrecorded Revenues--Revenues that have been earned but not yet recorded. • Unearned Revenues--Revenues that have been recorded but not yet earned. • Unrecorded Expenses--Expenses that have been incurred but not yet recorded. • Prepaid Expenses--Expenses that have been recorded but not yet incurred.

Three-Step Process forAdjusting Entries • Identify the original entries that were made, if any. (Original entries are only made for unearned revenues and prepaid expenses.) • Determine what the correct balances should be at this point in time. • Make the adjustments needed to correct the balances.

Example: Depreciation Adjusting Entry 12/31 Depreciation Expense--Buildings 7,800 Accumulated Depr.--Buildings 7,800 To record depreciation on building at 5% per year. Rosi, Inc., purchased buildings in 1997 at a cost of $156,000. Each year, 5% of the cost is depreciated. At the end of 2002, the following adjusting entry is made:

Example: Doubtful Accounts Adjusting Entry 12/31 Doubtful Accounts Expense 1,100 Allowance for Doubtful Accounts 1,100 To adjust for estimated doubtful accounts expense. An estimation of bad debts based on the ending receivables balance reveals that the allowance account needs to be increased by $1,100.

Example: Doubtful Accounts 3/19 Allowance for Doubtful Accounts 150 Accounts Receivable 150 To write off an uncollectible account. Later, assume on March 19 that a $150 receivable is deemed to be uncollectible. Using the allowance account, the uncollectible account is written off the books.

Example: Accrued Expenses Adjusting Entry 12/31 Salaries and Wages Expense 2,150 Salaries Payable 2,150 To record accrued salaries and wages. At the end of the fiscal period, Rosi, Inc., had accrued salaries and wages totaling $2,150.

Example: Accrued Revenues Adjusting Entry 12/31 Interest Receivable 250 Interest Revenue 250 To record accrued interest on a note receivable. Rosi, Inc., holds a note receivable from a customer on which interest totaling $250 has accrued.

Example: Prepaid Expenses Adjusting Entry 12/31 Insurance Expense 4,200 Prepaid Insurance 4,200 To record expired insurance. Rosi, Inc.’s trial balance shows that the asset account Prepaid Insurance has a balance of $8,000. By December 31, only $3,800 applies to future periods. $8,000 - $3,800

Example: Deferred Revenues Rosi, Inc., receives a payment of $2,550 from a customer prior to the services being rendered. By December 31, $2,075 in services have been provided. Original credit to a revenue account. $2,550 - $2,075 Adjusting Entry 12/31 Rent Revenue 475 Unearned Rent Revenue 475 To record unearned rent revenue.

Example: Deferred Revenues Rosi, Inc., receives a payment of $2,550 from a customer prior to the services being rendered. By December 31, $2,075 in services have been provided. Original credit to a liability account. Adjusting Entry 12/31 Unearned Rent Revenue 2,075 Rent Revenue 2,075 To record rent revenue ($2,550 - $475).

Example: Inventory Refer to Rosi, Inc.’s trial balance in this chapter. Note that the firm has $45,000 in inventory. The year-end count shows that $51,000 is on hand. Assume that the firm uses a periodic system.

Example: Inventory The XYZ Company earns a rent revenue of $500 in 19x8 but will not receive the payment until January 10, 19x9. An adjustment will be needed. What is the adjusting entry? Purchases, Purchase Discounts, and Cost of Goods Sold are affected by the adjusting entry to update the inventory account. Adjusting Entry 12/31 Inventory 6,000 Purchases Discounts 3,290 Cost of Goods Sold 153,310 Purchases 162,500 To adjust inventory, cost of goods sold, and related accounts. $51,000 - $45,000 To close To close

6. Preparing Financial Statements Prepare Trial Balance Make Adjusting Entries Prepare Financial Statements • After all transactions have been recorded, a trial balance prepared, and adjusting entries made, the financial statements are prepared. Record Trans-actions

7. The Closing Process • Real accounts are permanent accounts not closed to a zero balance at the end of the accounting period. These accounts are carried forward to the next period. • Nominal accounts are temporary accounts that are closed to a zero balance at the end of each accounting period. • Closing entries reduce all nominal accounts to a zero balance.

The Closing Process Retained Earnings Revenues Beg. Bal. xxx Revenues xxx Bal. xxx Since the revenue account is a nominal account, it is closed at the end of the period to Retained Earnings.

The Closing Process Retained Earnings Beg. Bal. xxx Revenues Expenses Expenses The expense account is credited in order to close the account at the end of the period. xxx Bal. xxx

The Closing Process Dividends Retained Earnings Beg. Bal. xxx Revenues The dividends account, which is also nominal, is credited to close out the balance. Expenses Dividends xxx Bal. xxx

The Closing Process Net Income for the period is determined by these two entries. Retained Earnings Beg. Bal. xxx Revenues End. Bal. xxx Retained Earnings is a real account and always carries a balance. Expenses Dividends

8. Post-Closing Trial Balance • Provides a listing of all real account balances at the end of the closing balance. • The trial balance assures that totaldebits equal total credits prior to the beginning of the new accounting period. • Only real accounts will have a balance at this time.

Example: Post-Closing Trial Balance Jim Brewster, Inc. Post-Closing Trial Balance December 31, 2002 DebitsCredits Cash $ 8,200 Accounts Receivable 4,000 Inventory 3,000 Supplies 1,000 Accounts Payable $ 5,000 Capital Stock 10,000 Retained Earnings 1,200 Totals $16,200 $16,200

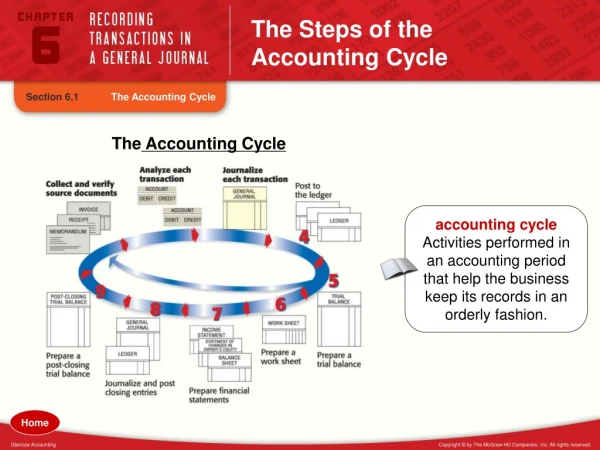

Summary of the Accounting Cycle • Analyze transactions and business documents. • Journalize transactions. • Post journal entries to accounts. • Determine account balances and prepare a trial balance. • Journalize and post adjusting entries. • Prepare financial statements. • Journalize and post closing entries. • Balance the accounts and prepare a post-closing trial balance.

Special Journals • A special journal is a book for recording similar transactions that occur frequently. • Sales Journal--A record where credit sales are recorded. • Subsidiary Ledger--A grouping of individual accounts that equal the balance of a control account in the general ledger.

Special Journals • Voucher Register--A book of original entry which takes the place of a purchases journal and provides a record of all authorized payments to be made by check. Charges on each voucher are classified by the appropriate accounting in the financial records. • Cash Receipts Journal--A record in which all cash received from sales, interest, rent, or other sources is recorded. • Cash Disbursements Journal--A record of all checks issued during the period in payment of properly approved vouchers.