Understanding Financial vs. Managerial Accounting: Key Differences and Uses

This session discusses the contrasting roles of financial and managerial accounting. Learn who uses the information, the involved entities, time periods, and basic information utilized in each. Discover the guiding standards and significant methods in both fields. The session also covers the essential characteristics that make information useful, such as relevance, reliability, comparability, and consistency. Participants will gain insights into how decision-makers leverage accounting information for various organizational needs.

Understanding Financial vs. Managerial Accounting: Key Differences and Uses

E N D

Presentation Transcript

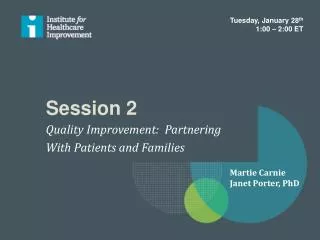

Session 2 AGENDA • Answer questions • Compare and contrast financial and managerial accounting Prof. Bentz

Financial Vs. Managerial • Who uses the information? • What entities are involved? • What time periods are used? • What basic information is used? • What are the guiding standards? • What are the more important methods? Prof. Bentz

Financial Vs. Managerial • What makes information useful? • Relevance • Reliability • Comparability • Consistency Prof. Bentz

Financial – Current and potential owners Directors Regulators Lenders Managerial – Directors Managers & Associates Customers (e.g., Federal Gov’t) “Partners” Users of the Information Prof. Bentz

Financial – Suppliers Customers Managers & Associates Managerial – Regulators Litigants Economists Investigators Users of the Information (2) Prof. Bentz

Financial – Entities that are recognized in law for both business and non-business purposes Managerial – Any identifiable unit for which costs, revenues, cash flows, or assets can be associated meaningfully Accounting Entities Prof. Bentz

Financial – Corporations Partnerships Trusts Sole proprietors Individuals Managerial – Cost centers Revenue centers Profit centers Activities Divisions Departments Examples of Entities (1) Prof. Bentz

Financial – Wendy’s OSU City of Columbus State of Ohio Managerial – Tim Horton’s Dept. of A&MIS Water Dept. Dept. of Education Examples of Entities (2) Prof. Bentz

Financial – Past months, quarters, or years Indefinite (e.g., bankruptcy trust) Managerial – Any period consistent with the information need at hand. Accounting Periods Prof. Bentz

Financial - Quarterly financial statements Periodic reports to a bankruptcy judge Managerial - Monthly division statements 20-year capital expenditure analysis Hourly spoilage reports Examples of Periods Prof. Bentz

Financial – Transactions, accruals, deferrals, estimates, allocations, and market values Managerial – Transactions, accruals, deferrals, estimates, allocations, market values, forecasts, plans, and hypothetical scenarios Basic Information Utilized Prof. Bentz

Financial – SEC FASB AICPA EITF Other GAAP Managerial – Cost Accounting Standards Bd. Company Stds. Contracts GAAP Guiding Standards Prof. Bentz

Financial – Standards protect the investing public and the functioning of markets. Managerial – Standards enhance the quality of the information available to managers and representatives of stakeholders. Role of the Standards Prof. Bentz

Financial – accounting equation double-entry system chart of accounts data dictionaries Documentation standards are nearly universal. Managerial – Fin. acct. methods ERP and other software systems Statistical methods Mathematical programming Accounting Methods Prof. Bentz

Financial – Timelinessof reporting & analysis is constrained by audits, SEC review, etc. Managerial – Timeliness is un-constrained by out-side forces, so management decides the trade-off among timeliness, cost, and quality. Usefulness: Relevance Prof. Bentz

Financial – Feedback value is relatively high and improving due to GAAP & standardization Managerial – Feedback value should be higher because the decision-makers can request needed information Usefulness: Relevance (2) Prof. Bentz

Financial – Predictive value is limited without other economic forecasts Managerial – Predictive value high because the perspective, volume, and variety of info. is geared for these purposes Usefulness: Relevance (3) Prof. Bentz

Financial – Neutrality is supposed to be high but abuses abound Managerial – Neutrality in the sense of an absence of “spin” and efforts to please bosses is important Usefulness: Reliability Prof. Bentz

Financial – Verifiability—objective bases that can be confirmed by other professionals Managerial – Verifiability—objective bases that can be confirmed by other professionals Usefulness: Reliability (2) Prof. Bentz

Financial – Representational validity - communicates a “valid” perspective of what is happening in the underlying system Managerial – Representational validity – communicates a “valid” perspective of what is happening in the underlying system Usefulness: Reliability (3) Prof. Bentz

Usefulness: Reliability (4) Is neutrality redundant? The idea is that an accountant should be neutral in developing and presenting information rather than taking sides on an issue and attempting to put a more favorable light on one side or another. Prof. Bentz

Financial – Comparability across entities for investment and lending decision purposes Managerial – Comparability – report results in a manner comparable with profit plans or analyses Usefulness: Comparability Prof. Bentz

Usefulness: Comparability (2) Enhancing comparability in mgt. acct. • Flexible budgets • Plans modified to reflect the actual operating environment (adaptive plans) • Seasonal adjustment of data Prof. Bentz

Usefulness: Comparability (3) Enhancing comparability in mgt. acct. • The most important comparability issue in MA is the reporting results in a manner consistent with the development of plans. • Comparability across business units is an important challenge in MA Prof. Bentz

Financial – Reporting standards are observed over time by reporting entities within a firm Managerial – Consistency of reporting and analysis methodologies over time. Usefulness: Consistency Prof. Bentz

Some Implications 1. Generally accepted accounting principles inform and support--but not constrain--what we do in managerial accounting. 2. If we are to better support internal users of information, we need to know how information is to be used. Increasingly, this implies interacting with other members of a team. Prof. Bentz

Some Implications 3. Being knowledgeable about financial reporting standards and transactions processing systems does not make one a good managerial accountant. Some would go so far as to argue that different skills and abilities are needed for managerial accounting, particularly when it comes to planning activities. Prof. Bentz

Where are YOU? • Comments? • Observations? • Questions? Prof. Bentz

Homework • http://fisher.osu.edu/~bentz_1/525/problems/H11C1E18.ppt • http://fisher.osu.edu/~bentz_1/525/problems/H11C1E21.ppt Prof. Bentz