Download

1 / 11

110 likes | 159 Views

Learn about discounted dividend model, growth models, and more to understand how stocks are valued & investment opportunities. Detailed insights by Dr. Menahem Rosenberg.

E N D

Valuation of Stocks Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

Asset Valuation • Asset Value as Present Value of the Cash Flows it will produce: Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

Stocks Features • Represents (residual) ownership. • Ownership implies control. • Stockholders elect directors. • Directors elect management. • Management’s goal: Maximize stock price. • Stocks certificate represent proportional ownership. • Stocks certificate entitle its holders to proportional distributions (mainly dividend), if there are any. Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

The Discounted Dividend Model • A discounted dividend model is any model that computes the value of a share of a stock as the present value of the expected future cash dividends • Using (1) above: Let: P0 be the present stock price, Dt - Cash dividend per share at time t r – discount rate Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

The Discounted Dividend Model • Alternative view of the Model. • Assume a risk less environment • Every investor takes a position in a stock for one period only. • P1 -the price the next investor will pay for the stock in period 1, after dividend in that period is paid • Repeated substitution will result in (2) Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

The Dividend Model • Case 1: Constant DividendWhen all dividends are the sameD0 = D1 = D2 = …. • The dividend stream is treated as a perpetuity Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

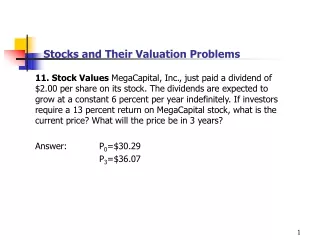

Dividend Growth Model • Case 2: Constant Growth Dividend • When dividend grow at constant growth rate g from D1 and on and g<r(normal growth) • D2 = D1(1+g)D3 = D2(1+g) = D1(1+g)2 • The dividend stream is treated as a constant growth perpetuity Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

Dividend Growth Model • Case 3: Limited abnormal growth continued by Constant Growth Dividend • Let dividend grow at g1> r rate for t periods, and from t+1 grow forever at a constant growth rate g2< r . • Compute (6.1) Dt+1= Dt (1+ g2) = D0(1+ g1)t (1+ g2) Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

Dividend Growth Model • Which can be substituted with a growing annuity Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

Where is Growth Coming from ? • Review:Net Income = Retained earning + Dividend • Retained earning are additions to equity, therefore, next period the increase in NI = ROE * Retained earning • Therefore, growth (7) g= ROE*(Retention Ratio) Fin 307-Stocks Valuation | Dr. Menahem Rosenberg

Price and Investment Opportunities • The price of a stock that pays out 100% of its earning : • If the firm decides to retain earning and invest in new project, its value will increase by exactly the projects’ NPV. Fin 307-Stocks Valuation | Dr. Menahem Rosenberg