Download

1 / 22

220 likes | 346 Views

Prescription for Chaos The New Medicare Drug Benefit Starts Up in January. AFSCME Retiree Program Fall, 2005. Standard Medicare Drug Benefit (As Passed by Congress in November, 2003). Monthly premium: $32 Annual deductible: $250 Seniors’ co-pay: 25%

E N D

Prescription for ChaosThe New Medicare Drug Benefit Starts Up in January AFSCME Retiree Program Fall, 2005

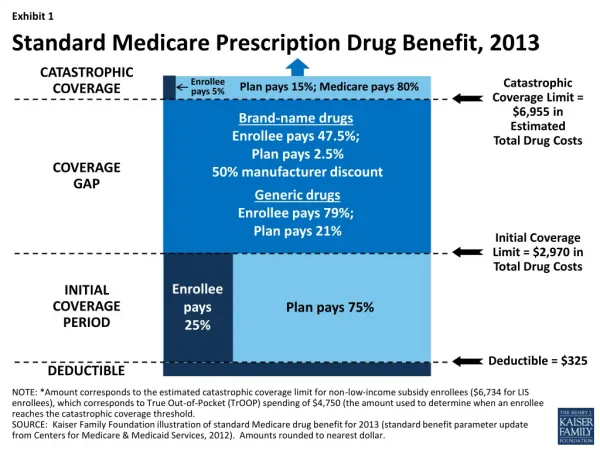

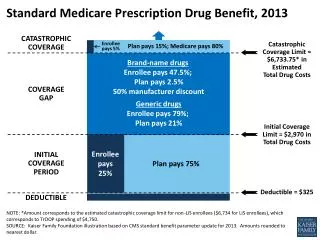

Standard MedicareDrug Benefit (As Passed by Congress in November, 2003) • Monthly premium: $32 • Annual deductible: $250 • Seniors’ co-pay: 25% • “Donut” hole: $2,250 to $5,100 • Catastrophic: Pays 95% • Effective Date: Jan. of 2006

The Bad News • Under-funded, skimpy drug benefit with huge donut hole. • While in the “hole,” seniors continue to pay premiums, but get no benefits. • Benefit provided by private insurance, rather than Medicare itself. • Weak employer subsidy - retirees could lose coverage. • Drugs will vary from plan to plan.

Where’s the Cost Containment ? • Law provides no real cost-containment. • Bans Medicare (and the power of its 40 million beneficiaries!) from negotiating lower prices with drug companies. • Relies on private insurance plans, which divide market, limit bargaining power. • Disallows re-importation from Canada without HHS approval.

Part D – Forms of Coverage The new Part D benefit will be provided by two types of competing private plans: • Stand-alone “Medicare Prescription Drug Plans” (PDPs), or • “Medicare Advantage” plans that include prescription drugs (MA-PDs)

Already Covered by Employer? If you are among the 1/3 of seniors who enjoy a comprehensive drug plan paid by a former employer, union or pension fund, you probably don’t need to buy a Medicare Part D plan. So, don’t buy Part D from a private insurer unless your plan’s sponsor says you should.

Employers Have Choices, Too. • They can continue providing own Rx plan instead of Part D and receive a subsidy from Medicare. • Subsidy is only available to plans with benefits at least equivalent to Part D. • Provide a new drug plan with benefits designed to supplement Part D.

More Employer Choices • Employers can purchase Part D drug coverage from a Medicare Prescription Drug Plan (PDP) or Medicare Advantage Plan (MA-PD). • Become an Employer PDP or MA-PD under Medicare. • Pay part or all of retirees’ Part D premium, with or without additional benefits.

Which option is most likely? • For 2006, most employers are expected to continue their current retiree drug plan and apply for the cash subsidy. • The subsidy is considered the easiest option because employers/plan sponsors • have more time to apply for the subsidy than waivers for other options. • won’t have to make big design changes.

Employer Subsidy… • for 2006 is 28% of each retiree’s drug costs from $250 to $5000 (indexed yearly). • is estimated to be $668 on average. [Calculated by employer,it depends on plan’s experience and retirees’ drug use.] • is only paid for drug costs of retirees not enrolled in a Medicare Part D plan. • is paid directly to the employer or plan sponsor (e.g.,union health & welfare fund). • is tax-exempt

Creditable Coverage • Employers/plan sponsors must send out notice of “creditable coverage” by Nov. 14. • “Creditable coverage” means plan benefits are at least as good as Part D’s. • If plan coverage is creditable, retirees won’t have to pay a premium penalty if they decide to join Part D in the future. • Save your notice for future reference.

A Note of Caution • Make sure you have the right to rejoin your employer plan if you drop it now for Part D. • Don’t even consider dropping employer-paid drug coverage if it means dropping ALL your retiree health benefits at the same time. • Check with your employer/plan sponsor to be certain of your rights.

Self-Pay Employer Plans • Retirees in these plans pay most or all of the premiums out-of-pocket. • Should contact the plan to see how it will coordinate with Part D. Plan sponsors have several options. • Plan sponsors can coordinate with Part D to reduce premiums for retirees. • Watch for notice of “creditable coverage” from your plan sponsor.

Medigap Insurance • Medigap plans that cover drugs (H, I, J) will continue for current participants only. With no new retirees, cost will rise quickly. • Medigap Rx plans generally don’t offer “creditable coverage,” so participants will pay penalty if they stick with the plan now, but join Part D in the future. • Participants should contact their plan, to learn about new options.

Medicare Part D Plans • Seniors can sign up for 2006 Part D Rx insurance plans between Nov. 15, 2005 and May 15, 2006. Benefits begin Jan. 1. • Joining Part D is voluntary. If, however, you don’t sign up during your initial eligibility period, but sign up in the future, you will pay apenalty: 1% for each monthyou delay. (unless you already have a plan with “creditable coverage”).

Comparing Part D Plans • Look at list of drugs each plan covers (the “formulary”) to see which ones cover the drugs you take. • Be aware that you may have to switch a drug to get full coverage from one plan. • Check to see if a plan works with your pharmacy of choice. • Compare plan designs. Not all plans will follow the standard benefit.

Extra Help • If your income is below $14,355 ($19,245 for couples) you may qualify for a program that pays all or some of Part D costs. • Contact the Medicare Helpline (1-800-633-4227) to get an application for the “Extra Help” program.

Illinois Cares Rx • In June, the state created the IL Cares Rx program to fill-in gaps in Part D coverage for limited-income seniors & disabled. • Those currently in IL SeniorCare and Circuit Breaker will be automatically enrolled in IL Cares RX. • SeniorCare income limits: $19,140 for singles and $25,660 for couples; Circuit Breaker income limits: $21,218 for singles and $28,480 for couples. • Seniors in these programs, or those who think they qualify, must submit a Part D “Extra Help” application to Medicare.

More on IL Cares Rx • Enrollees must get coverage from 1 of 2 private Medicare-approved Part D plans that will coordinate with IL Cares Rx. • They’ll get help with Part D premiums. • They’ll pay only $2 for generics and $5 for brands, up to $1,750 in annual drug costs. • They’ll have 20% co-pays between $1,750 & $5,100 in drug costs; co-pays drop to 5% for additional drugs. • For more information on IL Cares Rx, call the Dept. on Aging: 1-800-252-8966.

Seniors: Expect a Full Mailbox • On October 1, insurers began marketing the new Part D plans to seniors. • Every senior is expected to be inundated with offers (mail, calls, ads) – even if they already have Rx coverage. • Seniors who need drug coverage should compare plans carefully and call their state’s SHIP for information on available plans in their geographic area.

State Health Insurance Assistance Program (SHIP): In Illinois Call: (800) 548-9034

For more Information: • If you get your prescriptions from the VA (US Department of Veteran’s Affairs), call: 1-800-827-1000. • If you have prescription drug coverage with Tri-Care, call: 1-888-363-5433.