Download

1 / 13

130 likes | 248 Views

This article examines the fundamental dynamics between consumer demands and producer offerings in market equilibrium. It explores the conditions for market balance, where supply meets demand, and the implications of disequilibrium, resulting in surpluses or deficits. The article emphasizes the role of price in determining consumer and producer welfare, as well as how flexibility and elasticity affect market responses. It also delves into the concepts of consumer and producer surplus, price elasticity of demand, and supply elasticity, essential for understanding market behaviors and outcomes.

E N D

Balancing Equilibriums: What happens when Consumer Wants and Producer Offers match or don’t: In equilibrium consumer wants are set in such a way that the independent activities of producer offers match and the market clears. In disequilibrium the match is not complete and as a result there is a surplus or deficit in quantity. If there is a persistent surplus or deficit there is a welfare loss as Consumers or Producers take alternative measures to mitigate the welfare loss. This is the basic interaction between consumers and producers and price determines which actor gains or losses.

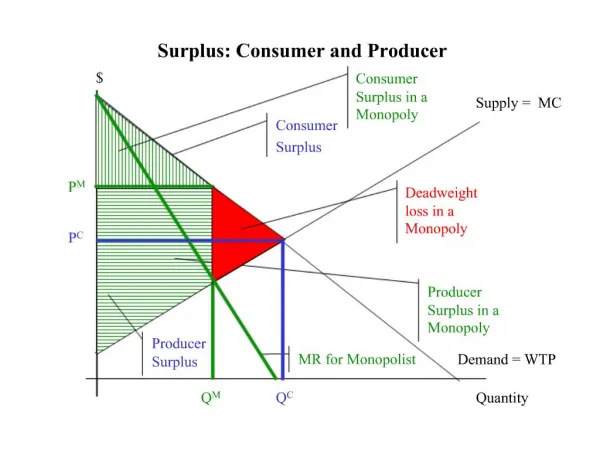

Market in Equilibrium • Consumer Surplus [Prp:E:Pe] plus Business Surplus [Producers Surplus [Pe:E:Pme] plus Supplier Surplus [0:Pme:E:Qe]] equals total welfare gain through market activity. Quantity Demanded equals Quantity Offered. Price Prp Demand E Supply Pe Pme 0 Quantity Qe

Market in Disequilibrium(1) • Too much offered: • Producers offer Qs hoping to get Ps as a price, but consumers are only willing to pay Pd for this quantity. Note in this situation the Pd is below the Pme for producers and they will leave the market. Quantity Qe and all the resources put into producing it is a total welfare loss to society. Price Demand Prp Ps Pme Supply Pd Quantity 0 Qs

Market in Disequilibrium(2) • Too little offered: • Producers offer Qs hoping to get Ps as a price, but consumers are willing to pay Pd for this quantity. Note in this situation the Pd is below the Prp so there is a market but area A:B:E is lost due to unsatisfied demand and Pe:E:B:Pe is the incentive for producers to expand quantity. Price Prp A Demand Pd Supply E Pe Ps B Pme 0 Quantity Qs Qe

Reactions to Disequilibrium • Consumers or Producers • Facing too much supply or too little supply have the Flexibility to: - Abandon the market and demand or supply disappear • Search for substitutes and substitute those goods for the shortage or use surplus goods for other purposes in other markets. • Change the boundaries of the market by arbitraging surpluses elsewhere or backing up markets that are short often using “black market activities”. • Changing complementarities : finding alternative ways of using the good that do not require this particular market. • Bidding prices upwards or downwards • Appealing to government.

Flexibility and Elasticity • The Flexibility of action by economic actors is dependent upon the elasticity of the market or how responsive a change in quantity is to a change in price. • An elastic market is one where there is a high responsiveness and an inelastic market is one where there is a low responsiveness. • If we have a complete knowledge of all of the factors that affect elasticity then we have a fundamental relationship which states that the product of the elasticity of a market and the flexibility of economic actors are constant and for the market in question is normalized to be unity. • Therefore the Flexibility of economic actors (f) is the inverse of the elasticity (e) • f = 1/e

Price Elasticity of Demand • Price Elasticity of Demand is calculated by the midpoint of two observed periods in time in which there is a change in quantity and price: • Price Elasticity of Demand = [Q2-Q1)/[(Q2+Q1)/2] [(P2-P1)/[(P2+P1)/2] • An inelastic elasticity has a value of 0 an increase in price leaves the quantity unchanged while an elastic demand curve has infinite quantity at only one price.

Changing Market Conditions due to changes in Demand Elasticity Demand Elasticity Elasticity = 1 Perfectly Inelastic Demand =0 Inelastic Demand <1 Elastic Demand >1 Perfectly Elastic =infinity

Special Issues with Demand Elasticity • When the Price Elasticity of Demand is unity (=1) Total Business Surplus is maximum. By adjusting price producers and suppliers cannot increase total revenue because an increase in price will lower total revenue and a decrease in price will also lower total revenue. • Unless producers can manipulate the demand for its own products or the relationship with its own suppliers , the limitation on total revenue means that with standard technologies total profit is also maximized.

Other Demand Elasticities Income Elasticity of Demand is a measure of how the demand quantity for a good changes as incomes increase. {Negative for inferiors goods, positive for superior goods and 0 for sticky goods.} [Percentage change in quantity demanded]/Percentage change in income] Cross Price Elasticity of Demand is a measure of how the demand changes for one good when the price of another good changes. {Negative for complements and positive for substitutes.} [Percentage change in quantity demanded]/Percentage change in price of another good]

Supply Elasticities • The Price Elasticity of Supply is the responsiveness of quantity supplied to the market price of that good: • Price Elasticity of Supply = [Percentage change in quantity supplied/percentage change in market price.] • The market price is determined by experience and is more valuable to the producer dependent upon the degree of control that the producer has in the market. • The degree of control is determined by the number of competitors that the producer has in the market and the ways in which each competitor reacts to the decisions undertaken by each other market participant.

Changing Market Conditions due to changes in Supply Elasticity • Supply Elasticity Elastic Supply > 1 Perfectly Inelastic Supply = 0 Pme Inelastic Supply <1 Unit Elastic Supply =1 Perfectly Elastic Supply = infinity Q* 0 Note: For Inelastic Supply Pme <0 and there is a quantity 0:Q* that must be “given away” In order to enter the market. -Pme

Summary: • Economic actors can change the circumstance of the market by being aware of the way markets work and exercising substitution for consumers and market control for the business sector. • The effectiveness of these strategic choices depends upon the nature of the government with respect to quantity regimes (quotas and contracts), price regimes (taxes and subsidies), and market regimes (consumer protection, market regulation and criminal investigations). • In each market situation all of these factors combine to produce an outcome which contributes to the welfare of society at the minimum disruption to alternative and complementary markets such that welfare is expanded through market activities.