Download

1 / 34

340 likes | 464 Views

Valuation and levered Betas. Some interesting questions to consider in applications. Today’s plan. Review what we have learned in the last lecture An example of a cash-flow calculation Examine the impact of financing on the cost of equity (levered Betas) Two approaches to calculate NPV

E N D

Valuation and levered Betas Some interesting questions to consider in applications FIN 819: lecture 5

Today’s plan • Review what we have learned in the last lecture • An example of a cash-flow calculation • Examine the impact of financing on the cost of equity (levered Betas) • Two approaches to calculate NPV • WACC ( weighted average cost of capital approach) • APV (adjusted present value approach)

What have we learned • Risk, returns and WACC • Your view of risk in finance • measure investment performance • measure risk • portfolio diversification and two types of risk • systematic risk and its measurement • three portfolio rules • CAPM and the security market line • Cost of capital and WACC • The things you have to pay attention to in calculating WACC

Example 1 • Based on the CAPM, ABC Company has a cost of capital of 17%. (4 + 1.3(10)). A breakdown of the company’s investment projects is listed below. • 1/3 Nuclear Parts: β=2.0 • 1/3 Computer Hard Drive: β =1.3 • 1/3 Dog Food Production: β =0.6 • When evaluating a new dog food production investment, which cost of capital should be used and how much?

Solution • Since dog food projects may have similar systematic risk to the dog food division, we use a beta of 0.6 to measure the risk of the projects to be taken. • Thus the expected return on the project or the cost of capital is 0.04+0.6*(0.1)=0.l or 10%

Example 2 • Stock A has a beta of .5 and investors expect it to return 5%. Stock B has a beta of 1.5 and investors expect it to return 13%. What is the market risk premium and the expected rate of return on the market portfolio?

Solution • According to the CAPM

Example 3 • You have $1 million of your own money and borrow another $1 million at a risk-free rate of 4% to invest in the market portfolio. The expected return for the market portfolio is 12%, what is the expected return on your portfolio?

Solution • We can use two approaches to solve it: • First, the expected rate of return of a portfolio is the weighed average of the expected rates of return of the securities in the portfolio. • Second , the beta of a portfolio is the weighed average of the betas of the securities in the portfolio. Then use the CAPM to get the expected rate of return.

Solution (continue) • First approach • Second approach

The cost of capital Cost of Capital • The expected return the firm’s investors require if they invest in securities or projects with comparable degrees of risk.

Cost of capital with tax benefit • When tax benefit of debt financing is considered, the company cost of capital is as

The cost of capital for the bond • The cost of capital for the bond • It is the YTM, the expected return required by the investors. • That is • The expected return on a bond can also be calculated by using CAPM

Example 2 • A bond with a face value of $2000 matures in 5 years. The coupon rate is 8%. If the market price for this bond is $1900. (a) What is the expected return on this bond or what is the cost of debt for this bond? (b) Suppose that the YTM is 9%, what is the market value of this bond?

Solution (a) (b)

The cost of capital for a stock • The cost of capital for a stock is calculated by using • CAPM • Dividend growth model

Example 3 • Sock A now pays a dividend of $1.5 per share annually, It is expected that dividend is going to grow at a constant rate of 2%. The current price for stock A is $25 per share. What is the expected return or the cost of capital by investing in this stock?

Another cash flow problem! Company A has a very old packaging machine which can be used for another two years. It has no book and market values. The maintenance cost for this old machine is $20,000 every year. Now a new packaging machine is available at the price of $ 300,000, which is depreciated in three years. If the new packaging machine is used, the maintenance cost is $10,000 every year. If there is no inflation, the cost capital is 10%, and the tax rate is 40% for company A. Questions: a. What is the valuation horizon used in this problem? b. Should company A invest in the new packaging machine now or waiting two years later?

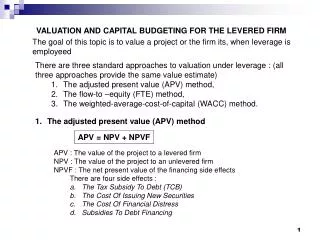

How does debt financing affect investment? • When firms issue debt, tax-shield and thus introduced financial risk impact the valuation of the projects and thus investments. • To understand how financing affects investments or real project valuations, we will introduce several variables.

Some terminology • D: the market value of debt • E: the market value of equity • UA: the value of the unlevered asset of the firm ( the value of the asset when D=0) • A: the value of the levered asset of the firm, i.e., D is positive; sometimes, V is used to refer to the same thing. • TX: the present value of the tax shield

Some terminology (continues) • : the beta of debt • : the beta of equity • : The beta of the unlevered asset • : the beta of the levered asset • : the beta of the tax-shield

Some terminology (continues) • : the cost of debt • : the cost of equity • : the cost of the unlevered asset • : the cost of the levered asset • : the cost of the tax-shield

The balance sheet Assets Liabilities and Equity Debt D Debt Tax shield (TX) Unlevered asset (UA) Equity E

The relationship among all kinds of values • From the balance sheet, we can have the following relationships

The present value of tax-shield • If the tax-shield is as risky as debt, and the firm issues risk-free perpetual debt, then the present value of the tax-shield can be regarded as a simple perpetuity with the amount of level cash flow as • Clearly,

The beta of equity • Using portfolio, we have • In this text book, we can assume that is not affected by firms’ capital structure, but decided by firms’ business risk.

The betas of equity and asset (continues) • Thus, for firms with the same business line, should be the same theoretically. • Two questions? • Is this making sense? • Why are we interested in the betas of unlevered assets?

An example • Firm D has the same business as firms A, B and C, whose betas and market values of debt and equity are given in the table in the next slide. Suppose all the firms have the risk-free debt and the risk free rate is 4%, the risk premium on the market portfolio is 8.4% annually and the corporate tax rate is 34%, what is the WACC for firm D?

Information for example Beta Debt Equity Firms 96 A 0.75 4.0 770 230 1.00 B 790 1.08 210 C 800 150 D

The two approaches for calculating NPV • WACC approach: • Basic idea: calculate free cash flows, as if the project is all-equity financed • Lower the cost of the capital to incorporate tax-shield; this is taken care of by WACC • Discount free cash flows by WACC to get NPV

APV approach • In contrast to the WACC approach, the APV approach is strongly recommended in academics. • Basic idea: • Calculate free cash flows • Use the cost of unlevered asset to discount the free cash flows • In addition, calculate the NPV of the tax shield • The sum of the two NPVs is the NPV of the project

What are the pros and cons of the two approaches • Which approach would you like ? Why or why not? • Can you predict which approach will be used more in the future?

An example • Firm D wants to expand its business. Currently the firm has D/V of 40%. The cost of the firm’s equity is 14.6%, the risk free rate is 8% and the debt is risk-free. Suppose that the firm wants to finance the expansion project by issuing $20 million of risk-free perpetual debt and $80 millions of equity. The expansion project will generate a perpetual free cash flow of $5 million at every year, starting next year. The tax rate is 35%. Please use two approaches to calculate the present value of the expansion project?

Solution • First approach: Suppose that the tax-shield is as risky as debt.