Stock Valuation

Stock Valuation. The price of stocks in the market place is the present value of the cash flows that stockholders have claim to: These cash flows consist generally of two components, dividends and capital gains. They are generally divided as follows:. Stock Valuation (Continued).

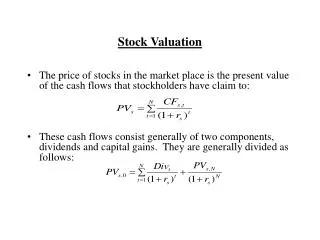

Stock Valuation

E N D

Presentation Transcript

Stock Valuation • The price of stocks in the market place is the present value of the cash flows that stockholders have claim to: • These cash flows consist generally of two components, dividends and capital gains. They are generally divided as follows:

Stock Valuation (Continued) • What are the differences between bond and stock cash flows? • Interest vs Dividends • Interest is paid before dividends. • Interest is generally fixed ; dividends are variable. • Interest is a contractual obligation; dividends are discretionary. • Principal vs. Future Stock Prices • Principal is contractually binding to the firm; future stock prices are not. • In liquidation, claims to both principal and interest must be satisfied before payments can be made to stockholders • What do these differences imply about potential differences between rs and rd?

Stock Valuation (Continued) • If, for simplicity, we assume that dividends grow forever at a constant rate, g, and that that rate is lower than the required rate of return on the stock, rs, then the present value of the dividends and future stock price can be expressed as • This says that the price of the stock today equals the expected dividend one year from today (Div1) divided by the difference between the required rate of return and the constant growth rate (rs-g) • Under these same assumptions, the required return on the stock could be estimated as

Stock Valuation (Continued) • Another useful way to think about the price of a stock is as • The first component, EPS1/rs, is the price of the stock if equity cash flows (or earnings) remain constant forever. The second component is the expected NPV from future growth opportunities. • What determines whether NPVGO is positive or negative?

Stock Valuation (Continued) • By setting the two stock pricing relationships equal to each other and recognizing that (Div1/EPS1) equals 1-b, where b is the firm’s retention ratio, and g is the ROE*b, we can express NPVGO as • The above relationship tells us that NPVGO will be positive so long as the ROE on the investment exceeds the required rate of return,rs

Stock Valuation (Continued) • Numerical Example: Suppose a firm’s expected earnings per share next year and every year thereafter are $2.50 and that the required return on the firm’s stock is 15%. What is the price of the firm’s stock? • PV,s,0 = EPS1/rs = 2.50/.15 = $16.67 • Now suppose the firm discovers an opportunity to invest in new assets that produce additional earnings annually forever of $.20 per share. The investment will be funded by a one-time dividend reduction of $1.00 per share. What is the value of this investment to current shareholders if investors can make it only once? • NPV1 = -$1 + [$.20/.15] = $.33

Stock Valuation (Continued) • If the firm could retain 40% of its eps in year 2 to make an investment that costs $1.08 and the ROE on this investment would also be 20%, what would be the value of this investment to shareholders? • NPV2 = -$1.08 + .2*1.08/.15 = .36 • What would happen if the firm could make these investments indefinitely by retaining 40% of its earnings and producing ROEs of 20%? • What would be the price of the stock? • EPS1/rs + NPVGO = $2.5/.15 + $4.76 = $21.43

Stock Valuation (Continued) • How does that coincide with the earlier model