Download

1 / 9

90 likes | 225 Views

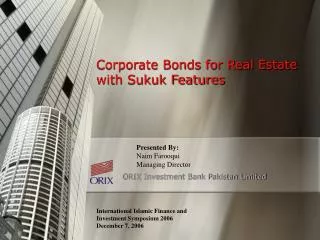

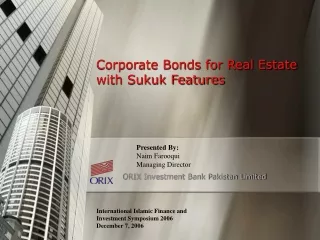

Corporate Bonds for Real Estate with Sukuk Features. Presented By: Naim Farooqui Managing Director. ORIX Investment Bank Pakistan Limited. International Islamic Finance and Investment Symposium 2006 December 7, 2006. 1. Bank Syndication Debt -Rs. 150 m. Corporate House

E N D

Corporate Bonds for Real Estate with Sukuk Features Presented By: Naim Farooqui Managing Director ORIX Investment Bank Pakistan Limited International Islamic Finance and Investment Symposium 2006 December 7, 2006

1 Bank Syndication Debt -Rs. 150 m Corporate House Equity – Rs. 121 m Real Estate Acquisition Transaction Structure Equity + Debt Rs. 271 m Rentals Company 1 Purchase Company 2 Rented Office Building Company 3 Company 4

Making a Case for Securitization for A Real Estate Finance Company (REFC) 2 • Securitization is a process for institutions to turn their locked up assets i.e. mortgages in the instant case, which are illiquid and lumpy, into tradable securities such as bonds. • Securitization is an open market selling of financial instrument backed by asset’s cash flow or asset value (mortgages). • A contractual arrangement whereby the REFC sells its mortgage receivables to a special purpose vehicle (SPV). • SPV issues debt instruments (bonds) to finance the purchase

Normal REFC Business Operations Securitization Structure Receivables 3 Mortgages Typical Structure Mortgage Backed Securitization Real Estate Finance Company Extension of Loans For Real Estate Cash Proceeds Raised Via Issuance of Debt Securities Housing Mortgage Receivables SPV DebtSecurities Safeguarding Investors Interest Cash • Key Issues To be Addressed • Non-Recourse Element • Accounting Clearance • Legal Issues • Market For Instrument • Regulatory Aspects • Security Mechanisms Investors Trustee Private Placements Public Placements

Structure of SPV 4 • Originator: entity that generates receivables • Issuer of the securities: SPV (any form, usually trust, corporation, partnership, etc.) • Advisor/Arranger: structures transaction; prepares documentation alongside legal, liaison with auditors • Underwriter: who places securities in the market

5 Structure of SPV…contd. • Custodian: entity that holds receivables as agent and bailee for the trustee or trustees • Servicer: who collects receivables and transfers funds to accounts of trustees • Trustee: who deals with the administration—holds receivables; receives payment on receivables, makes payment to security holders • Rating agencies: JCR-VIS, PACRA.—helps in structuring; determine opinions needed, etc.

6 General Benefits of Securitization • Why Securitize? • Lower-cost financing • Liquidity crunches? • Equity saving • Leverage restrictions • Reduction of assets – create liquidity to the company • Matched funding / funding strategy • Earnings • Originator capitalizes the future cash flow

Summing Benefits for all Stakeholders 7 • To owner/originator • Alternative financing instruments • Improve liquidity in the balance sheet • Reinvestment and freeing up the low-yield assets • Transfer the interest rate risks to SPV • Reducing corporate gearing • To bondholders/investors • New Investment opportunities for diversification • Direct participation in real estate market by small investors • Building as collateral • To Real Estate Market • An active secondary capital market for institutional investment • Alternative Financing Options

8 Conclusions Similarities of SUKUK with the proposed structure The proposed structure though based on conventional model can easily be converted into a Shariah Compliant Sukuk Bond. It has the following characteristics which are important elements of Sukuks: • Corporate Bonds are easily Tradable – Similarly, SUKUK being liquid real assets, are easily transferred and traded in the financial market. • Corporate Bonds can be Rated – Credit rating increase the credibility of financial instruments. SUKUK are easily analyzed by international and regional rating agencies which facilitates their marketability. Differences in Main features: • Sukuk have share holding in the underlying asset while Bonds are purely a debt instrument. • Sukuk are limited to Sharia permissible ventures/products.