Download

1 / 69

690 likes | 994 Views

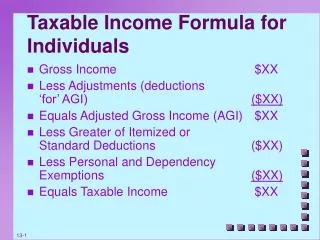

Income Taxation of Individuals. Chapter 11. Individual Income Tax Model. Gross income Less: Deductions for adjusted gross income Equals: Adjusted Gross Income (AGI) Less: Itemized or standard deduction Less: Personal & dependency exemptions Equals: Taxable income.

E N D

Income TaxationofIndividuals Chapter 11

Individual Income Tax Model Gross income Less: Deductions for adjusted gross income Equals:Adjusted Gross Income (AGI) Less: Itemized or standard deduction Less: Personal & dependency exemptions Equals: Taxable income

Tax Model (continued) Taxable income Times: Tax rate Equals: Gross income tax liability Less: Tax credits Plus: Additions to tax Less: Tax prepayments Equals: Net tax due or tax refund

Deductions For AGI • Deductions discussed in previous chapters • Retirement plan contributions including IRAs • Moving expenses • 50% of self-employment taxes • Self-employed health insurance • Alimony paid

Deductions For AGI • Deductions discussed in this chapter • Educator expenses • Student loan interest expense • Tuition and fees deduction • Penalty on early withdrawals of savings • Health savings accounts • National guard & military reserve travel

Educator Expenses • Kindergarten through 12th grade teachers may deduct up to $250 of unreimbursed expenses for books, supplies, computer equipment, software, and other supplemental materials used in the classroom • Expired at end of 2003 but expected to be extended retroactively by Congress

Student Loan Interest • Deduction allowed for interest paid on qualified student loans incurred and used for tuition, fees, room, board, books, and supplies • Deduction limit is $2,500 • Limit is phased out for modified AGI of $50,000 - $65,000 ($100,000 - $130,000 for married persons filing jointly) • Individuals claimed as dependents cannot take deduction on their own tax return • Expenses paid by tax-exempt scholarships or subject to education credits must be excluded from loan amounts and related interest

Tuition & Fees Deduction • $4,000 deduction for 2004-2005 for tuition & fees for taxpayer, spouse, and dependents • Income limits apply ($65,000 if single and $130,000 if married filing jointly) • Deduction is reduced to $2,000 for singles with income $65,000 - $80,000 ($130,000 - $160,000 for joint filers) • Individuals who are claimed as dependents cannot take deduction on their own tax return • No double benefit - no deduction if expense is deductible under any other provision (including education credits)

Penalty on Early Withdrawals • Penalties assessed on premature withdrawals from certificates of deposits or other savings accounts are deductible • Gross interest income, unreduced by the penalty, is included in taxable income • Deducting the penalty ensures that only net interest income is included in taxable income

Health Savings Accounts • Taxpayers covered by high-deductible medical insurance policies only may deduct amounts set aside in an MSA or HSA • Contributions and earnings on MSAs and HSAs are not taxed when withdrawn to pay medical expenses • For MSAs, qualified policies are those with deductibles of $1,700 - $2,600 for individuals ($3,450 - $5,150 for families) in 2004 • Contributions to MSAs are limited to 65% of policy deductible for individuals (75% for families)

Health Savings Accounts • HSAs are similar to MSAs but with different limits • In 2004, individuals with deductibles of at least $1,000 ($2,000 for families) can qualify for a deduction equal to lesser of $2,250 ($4,500 for families) or the annual policy deductible • Distributions not spent on qualifying expenses are included in income and subject to a 10% penalty for HSAs and 15% penalty for MSAs

Special Travel Deduction • For nonreimbursed travel expenses to attend National Guard or military reserve meetings more than 100 miles from home • Maximum deduction is general government per diem rate for the area • Excess expenses can be deducted as miscellaneous itemized deductions (subject to 2% of AGI floor)

Filing Status • Taxpayer’s filing status determines standard deduction and tax rate schedule • Marital status determined on the last day of the tax year • Separated spouses are considered married until divorce becomes final

Filing Status - Married • Can file jointly if both spouses are US citizens or US residents (or if nonresident alien agrees to be taxed on worldwide income) • If the couple file separately, both must itemize deductions or both must use the standard deduction

Surviving Spouse • Marital status is determined at the date of death so a joint return can be filed for the year in which a spouse dies • A surviving spouse may continue to use the tax rates and standard deduction for married persons filing jointly for the next 2 years only if a dependent child lives with the taxpayer

Filing Status – Unmarried • Unmarried taxpayers file as • Head of household - an unmarried person who provides more than half of the cost of maintaining a home in which a child or other qualifying relative lives for more than half the year • Single

Head of Household Qualifying relatives • Unmarried child who lives with the taxpayer for more than half of the taxable year (does not need to be taxpayer’s dependent) • A parentof the taxpayer who is a dependent (does not need to live in taxpayer's home) • Other qualifying relatives must live with the taxpayer for more than half the year and be a dependent

Head of Household • Qualifying relatives include brothers, sisters, parents, grandparents, nieces and nephews by blood, aunts and uncles (defined as brother or sister of father or mother) • Cousins and more distant relatives are not included in the definition of qualifying relatives

Abandoned Spouse • A taxpayer who is married but whose spouse did not live with him or her at any time during the last six months of the tax year and who provides more than half the cost of maintaining the home in which a dependent child lives • A qualifying abandoned spouse uses head of household tax rates and standard deduction

Exemptions • Each taxpayer (who is not a dependent) is entitled to one personal exemption • Exemption deduction is $3,100 for 2004 • Additional exemptions allowed for each person who is considered a dependent • Anyone who is claimed as a dependent cannot claim a personal exemption

Dependency Exemptions An individual qualifies as a dependent only if all 5of the requirements are satisfied: 1.Relative or member-of-household test 2. The support test 3. Gross income test 4. Joint return test 5. Citizenship or residency test

Relative or Member-of-Household Test • The dependent must be either be a qualifying relative (including a child, grandchild, brother, sister, parent, grandparent, niece, nephew, aunt and uncle) or • A member of the taxpayer’s household for the entire taxable year

The Support Test • Taxpayer must provide more than 50% of the dependent's total support • Support includes amounts spent for food, clothing, shelter, medical care, education and capital expenditures such as a car • Value of services and scholarship funds are omitted in determining support received by a student • Nontaxable income used for support must be included in support determination

Multiple Support Agreement • Multiple support agreements allow one member of group of support providers to claim the exemption when • Together the group meets the support test • All other dependency tests are met • Member who claims exemption must provide more than 10% of the total support and other members providing 10% support agree to exemption

Gross Income Test • The dependent's gross income from taxable sources must be less than the exemption amount ($3,100 for 2004) • The gross income test is waived for • Child of taxpayer who is under age 19 at year end or • Child of taxpayer who is under age 24 at year end and was a full-time student for at least 5 months during the year

Phaseout of Exemptions • Both personal and dependency exemptions are phased out at a rate of 2% (4% for MFS) for each $2,500 (or fraction thereof) of AGI above thresholds • $142,700 if single • $178,350 if head of household • $214,050 if married filing jointly • $107,025 if married filing separately

Exemption Phaseout (1) (AGI – threshold AGI)/$2,500 = Phaseout Factor (always round up to next whole number) (2) Phaseout Factor x 2% = Phaseout Percentage (3) Exemption Amount x (1 – Phaseout Percentage) = Adjusted Exemption Deduction • Once AGI exceeds the threshold AGI by more than $122,500 ($61,250 for MFS) the exemption deduction is completely phased out

Standard Deductions • Standard Deductions • $9,700 married filing a joint return • $4,850 married filing separately • $7,100 head of household • $4,850 single individual • Add on standard deduction if taxpayer is elderly (age 65 or older) or blind • $1,200 if single or head of household • $950 if married

Dependent’s Standard Deduction • Dependent’s standard deduction is limited to the greater of: (1) $800 or (2) Earned income + $250 (up to otherwise allowable standard deduction) • Earned income includes salary and wages • Earned income does not include interest income, dividend income, capital gains, or income as beneficiary of a trust

Itemized Deductions • Itemized deductions provide tax benefit only to the extent that, in total, they exceed the taxpayer’s standard deduction • Taxpayers can maximize use of the standard deduction and itemized deductions by timing certain deductible payments

Medical Expenses • Medical expenses paid for the taxpayer, spouse and dependents, after reduction for insurance reimbursements, are deductible only to the extent they exceed 7.5% of AGI for the year • Qualified medical costs includes prescription drugs and insulin, costs of a hospital, clinic, doctor, dentist, eyeglasses, contract lenses, transportation for medical care and health insurance costs

Medical Expenses • Health insurance premiums for taxpayers and their dependents are deductible only if paid from after-tax income • Premiums paid through an employer-sponsored cafeteria plan are not deductible • Premiums for disability insurance and for loss of life, limb or income are not deductible • Premiums for long-term care insurance are deductible, subject to limits based on age

Taxes • Deductible taxes include • State, local, and foreign real property taxes • State and local personal property taxes • State, local, and foreign income taxes • Other federal, state, local, and foreign taxes incurred in a business or other income-producing activity

Nondeductible Taxes • Federal income taxes • Employee's share of payroll taxes • Federal excise taxes not incurred for business • State and local sales taxes on goods for personal use • Assessments on property that increase property value

Interest Expense • Deductible interest includes • Investment interest • Home mortgage interest • No deduction for most other personal interest such as interest on auto loans, life insurance loans, credit card debt, and delinquent tax payments (except previously mentioned student loan interest)

Investment Interest Expense • Investment interest includes interest on loans to acquire or hold investment property and margin account interest paid to a broker • Investment interest expense is only deductible to the extent of net investment income • Net investment income = excess of investment income over investment expenses • Excess is carried forward (indefinitely) subject to same limit in future years

Investment Interest Expense • Investment incomeincludesgross income from interest, annuities, and short-term capital gains from investment property • Long-term capital gains or dividends taxed at favorable rates are excluded unless election made to forgo the favorable rate • Investment expenses includes safe deposit box rental fees, investment counsel fees, brokerage account maintenance fees • Limited to the lesser of total investment expenses or net miscellaneous itemized deductions after reduction for 2% AGI floor

Qualified Residence Interest • Interest paid for acquisition debt or home equity debt for up to 2 qualified residences • Interest on acquisition debt of up to $1 million principal amount (combined limit for 2 homes) is deductible • Acquisition debt includes mortgage to buy, construct, or improve the residence

Qualified Residence Interest • Interest on up to $100,000 principal amount of home equity loan is deductible • Loan proceeds can be used for any purpose • Points (loan origination fees) paid on initial home mortgages are deductible • Points paid to refinance an exiting loan must be amortized over life of loan

Charitable Contributions • Congress allows individuals, corporations, estates and trusts to deduct contributions to certain qualified organizations • Partnerships and S corporations pass the contributions through to their partners and shareholders who then claim the deductions on their own income tax returns

Charitable Contributions • Qualified charitable organizations • Governmental units (federal, state and local governments) and entities formed and operated exclusively for religious, charitable, scientific, literary or educational purposes, including churches, nonprofit hospitals, school and universities, libraries, and social service agencies • Direct contributions to needy individuals are notdeductible

Charitable Contributions • No deduction allowed to the extent that valuable goods or services are received in return for the contribution • Exception - contributors to universities who receive preferred rights to purchase tickets for university athletic events may deduct 80% of the amount of their contribution • Individuals can deduct up to 50% of AGI • Excess contributions may be carried forward up to 5 years

Charitable Contributions • No deduction for contributions of the taxpayer’s services and rent-free use of the taxpayer’s property • Out-of-pocket costs incurred for volunteer work for a qualifying charity are deductible • Property other than long-term capital gain property is valued at lesser of FMV or basis

Contributions of LTCG Property • LTCG property is valued at FMV (which is usually greater than adjusted basis) • Tangible personalty given to a charity which does not use the property in its tax-exempt activity is valued at the lower adjusted basis • Deduction for LTCG property valued at FMV is limited to 30% of AGI • 30% limit can be avoided (and 50% AGI limit applied) if taxpayer elects to use lower basis • If made, election applies to all LTCG contributions that year

Charitable Contributions • Stocks or other income producing property that have declined in value should be sold so that the loss can be claimed with the sale proceeds donated • Fees incurred for appraisals of donated property may be deducted as a miscellaneous itemized deductions

Casualty and Theft Losses • Loss is the lesser of • Asset’s adjusted basis or • Decline in asset’s fair market value as a result of the casualty • Loss is reduced for any insurance proceeds received • $100 floor applies to each casualty • Deductible only to extent total losses exceed 10% of AGI

Miscellaneous Deductions • Only excess over 2% of AGI is deductible • Unreimbursed employee business expenses • Job hunting expenses (in searching for a new job in current line of business) • Investment-related expenses • Hobby expenses (up to hobby income) • Tax preparation and planning advice

Phaseout ofItemized Deductions • Total deductions phased out by 3% of AGI in excess of $142,700 in 2004 ($71,350 if MFS) • Exception - deductions not phased out for • Medical expenses • Investment interest • Casualty and theft losses • Total deductions are not reduced by more than 80% regardless of type

Tax Rates forMarried Filing a Joint Return • For married filing a joint return for 2004 • 10% on first $14,300 taxable income • 15% on $14,301 - $58,100 • 25% on $58,101 - $117,250 • 28% on $117,251 - $178,650 • 33% on $178,651 - $319,100 • 35% over $319,100

Tax Rates forMarried Filing Separately • For married filing separately for 2004 • 10% on first $7,150 taxable income • 15% on $7,151 - $29,050 • 25% on $29,051 - $58,625 • 28% on $58,626 - $89,325 • 33% on $89,326 - $159,550 • 35% over $159,551