Download

1 / 2

0 likes | 6 Views

ufeffDemystifying Bank Loan Rates: What You Need to Know Before BorrowingBank loan rates are the interest rates that financial institutions charge on the money they lend to individuals

E N D

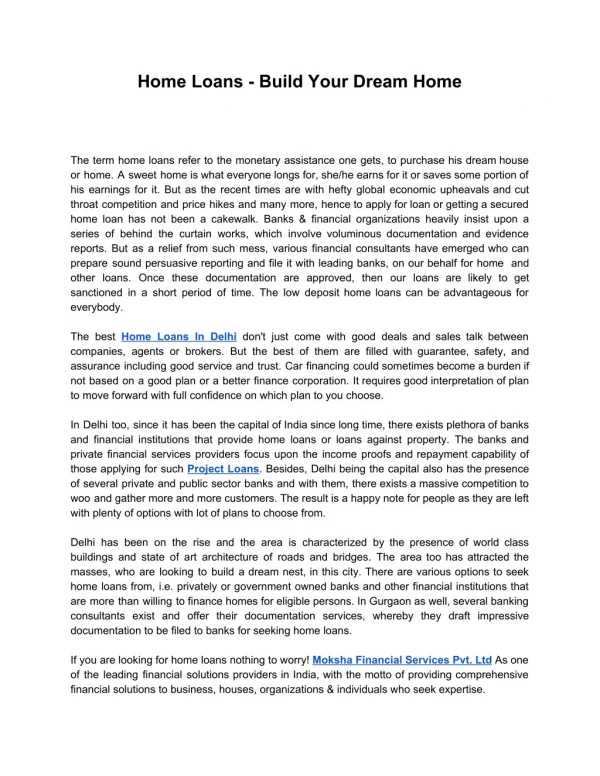

From Dream Home to Reality: Navigating the World of Real Estate Loans Real estate loans are a crucial aspect of the real estate industry, providing individuals and businesses with the financial means to purchase property. These loans are typically secured by the property itself, making them a lower risk for lenders and allowing borrowers to access larger sums of money than they might otherwise be able to. Understanding the ins and outs of real estate loans is essential for anyone looking to enter the property market, whether as a buyer or a seller. Real estate loans come in various forms, each with its own set of terms, conditions, and requirements. From traditional mortgages to commercial real estate loans, the options available to borrowers are diverse and can be tailored to suit specific needs and circumstances. It's important for borrowers to understand the different types of real estate loans available to them, as well as the implications of each, in order to make informed decisions about their financial future. Types of Real Estate Loans: Exploring Your Options When it comes to real estate loans, there are several options available to borrowers, each with its own set of advantages and disadvantages. The most common type of real estate loan is the traditional mortgage, which is typically used by individuals to purchase residential property. These loans come with fixed or adjustable interest rates and can be repaid over a period of 15 to 30 years, depending on the terms of the loan. For those looking to invest in commercial property, commercial real estate loans are the go-to option. These loans are designed for businesses and investors looking to purchase or refinance income-producing properties, such as office buildings, retail spaces, or industrial facilities. Commercial real estate loans typically come with higher interest rates and shorter repayment terms than traditional mortgages, reflecting the higher risk associated with commercial property investments. The Application Process for Real Estate Loans: What to Expect The application process for real estate loans can be complex and time-consuming, requiring borrowers to provide a significant amount of documentation and information about their financial situation. Lenders will typically require proof of income, tax returns, bank statements, and other financial records in order to assess the borrower's creditworthiness and ability to repay the loan. In addition, borrowers will need to provide details about the property they wish to purchase, including appraisals and inspections. Once the application has been submitted, lenders will review the borrower's financial information and assess the property's value before making a decision on whether to approve the loan. This process can take several weeks or even months, depending on the complexity of the loan and the lender's internal processes. It's important for borrowers to be patient and prepared for potential delays during the application process, as well as to be proactive in providing any additional information or documentation requested by the lender. Factors That Affect Real Estate Loan Approval: Tips for Success There are several factors that can affect a borrower's ability to secure a real estate loan, including credit score, income, debt-to-income ratio, and the property's value. Lenders will typically look for borrowers with a credit score of 620 or higher, as well as a stable income and a low debt-to-income ratio. In addition, the property being purchased will need to meet certain criteria in order to be eligible for financing. To improve their chances of loan approval, borrowers should take steps to improve their credit score, reduce their debt, and increase their income before applying for a real estate loan. It's also important for borrowers to carefully consider the property they wish to purchase and ensure that it meets the lender's requirements in terms of value and condition. By taking these factors into account and being proactive in addressing any potential issues, borrowers can increase their chances of securing a real estate loan. Real Estate Loan Terms and Conditions: What You Need to Know Real estate loans come with a variety of terms and conditions that borrowers need to be aware of before signing on the dotted line. These include interest rates, repayment terms, fees, and penalties, all of which can have a significant impact on the overall Browse this site cost of the loan. It's important for borrowers to carefully review these terms and conditions before agreeing to a loan in order to ensure that they fully understand their obligations and rights as a borrower. Interest rates are one of the most important factors to consider when taking out a real estate loan, as they will determine the amount of interest that accrues on the loan over time. Borrowers can choose between fixed-rate and adjustable-rate

mortgages, each with its own set of advantages and disadvantages. Fixed-rate mortgages offer stable monthly payments but may come with higher initial interest rates, while adjustable-rate mortgages offer lower initial rates but can fluctuate over time. Real Estate Loan Repayment Options: Making the Right Choice When it comes to repaying a real estate loan, borrowers have several options available to them, each with its own set of implications for their financial future. The most common repayment option is a traditional amortizing loan, which involves making regular monthly payments that include both principal and interest. This type of loan is designed to be fully repaid over a set period of time, typically 15 to 30 years, depending on the terms of the loan. For those looking for more flexibility in their repayment schedule, interest-only loans may be an option. These loans allow borrowers to make interest-only payments for a set period of time before beginning to repay the principal. While this can provide short-term relief in terms of cash flow, it can also result in higher overall costs over the life of the loan. It's important for borrowers to carefully consider their financial situation and long-term goals before choosing a repayment option for their real estate loan. Real Estate Loan Risks and How to Mitigate Them Like any financial product, real estate loans come with a certain level of risk that borrowers need to be aware of in order to make informed decisions about their financial future. One of the biggest risks associated with real estate loans is the potential for foreclosure if borrowers are unable to make their monthly payments. This can result in the loss of the property and significant damage to the borrower's credit score. To mitigate this risk, borrowers should carefully consider their ability to repay the loan before taking it out and ensure that they have a stable source of income that will allow them to meet their monthly obligations. It's also important for borrowers to have an emergency fund in place that can cover several months' worth of mortgage payments in case of unexpected financial hardship. By taking these steps and being proactive in managing their finances, borrowers can reduce the risk of defaulting on their real estate loan and protect their investment in the long run.