Download

1 / 32

340 likes | 596 Views

Chapter 12 - Cost of Capital. Where we’ve been. Basic Skills: (Time value of money, Financial Statements) Investments: (Stocks, Bonds, Risk and Return) Corporate Finance: (The Investment Decision - Capital Budgeting). The investment decision.

E N D

Where we’ve been... • Basic Skills: (Time value of money, Financial Statements) • Investments: (Stocks, Bonds, Risk and Return) • Corporate Finance: (The Investment Decision - Capital Budgeting)

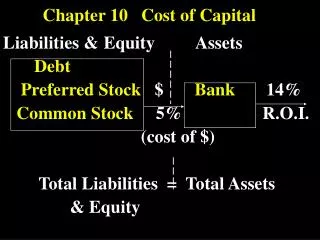

The investment decision Assets Liabilities & Equity Current Assets Current Liabilities Fixed Assets Long-term Debt Preferred Stock Common Equity

Where we’re going... Corporate Finance:(The Financing Decision) • Cost of capital • Leverage • Capital Structure • Dividends

The financing decision Assets Liabilities & Equity Current Assets Current Liabilities Fixed Assets Long-term Debt Preferred Stock Common Equity

Assets Liabilities & Equity Current assets Current Liabilities Long-term Debt Preferred Stock Common Equity } Capital Structure

Ch. 12 - Cost of Capital • For Investors, the rate of return on a security is a benefit of investing. • For Financial Managers, that same rate of return is a cost of raising funds that are needed to operate the firm. • In other words, the cost of raising funds is the firm’s cost of capital.

How can the firm raise capital? • Bonds • Preferred Stock • Common Stock • Each of these offers a rate of return to investors. • This return is a cost to the firm. • “Cost of capital” actually refers to the weighted cost of capital - a weighted average cost of financing sources.

Basic Definitions • Flotation costs: underwriter’s spread and issuing cost associated with issuance and marketing new securities • Tax effect: borrow at 9%, tax rate 34%, what is the after-tax cost of debt? 9% (1 – 34%) = 5.94% • Cost of capital needs to adjust both flotation cost and corporate tax

Cost of Debt For the issuing firm, the cost of debt is: • the rate of return required by investors, • adjusted for flotation costs and • adjusted for taxes.

Example: Tax effects of financing with debt with stockwith debt EBIT 400,000 400,000 - interest expense 0(50,000) EBT 400,000 350,000 - taxes (34%) (136,000)(119,000) EAT 264,000 231,000 • Now, suppose the firm pays $50,000 in dividends to the stockholders.

Example: Tax effects of financing with debt with stockwith debt EBIT 400,000 400,000 - interest expense 0(50,000) EBT 400,000 350,000 - taxes (34%) (136,000)(119,000) EAT 264,000 231,000 - dividends (50,000) 0 Retained earnings 214,000 231,000

1 = - After-tax Before-tax Marginal % cost of % cost of x tax Debt Debt rate Kd = kd (1 - T) .066 = .10 (1 - .34)

Example: Cost of Debt • Prescott Corporation issues a $1,000 par, 20 year bond paying the market rate of 10%. Coupons are annual. The bond will sell for par since it pays the market rate, but flotation costs amount to $50 per bond. • What is the pre-tax and after-tax cost of debt for Prescott Corporation?

Pre-tax cost of debt: N = 20 PMT = 100 FV = 1000 So, a 10% bond PV = -950 costs the firm solve: I = 10.61% = kdonly 7% (with • After-tax cost of debt: flotation costs) Kd = kd (1 - T) since the interest Kd = .1061 (1 - .34) is tax deductible. Kd = .07 = 7%

Cost of Preferred Stock • Finding the cost of preferred stock is similar to finding the rate of return (from Chapter 8), except that we have to consider the flotation costs associated with issuing preferred stock.

D NPo Cost of Preferred Stock • Recall: kp = = • From the firm’s point of view: kp = = NPo = price - flotation costs! Dividend Price D Po Dividend Net Price

Example: Cost of Preferred • If Prescott Corporation issues preferred stock, it will pay a dividend of $8 per year and should be valued at $75 per share. If flotation costs amount to $1 per share, what is the cost of preferred stock for Prescott?

D NPo Cost of Preferred Stock kp = = = = 10.81% Dividend Net Price 8.00 74.00

Cost of Common Stock There are two sources of Common Equity: 1) Internal common equity (retained earnings). 2) External common equity (new common stock issue). Do these two sources have the same cost?

Cost of Internal Equity • Since the stockholders own the firm’s retained earnings, the cost is simply the stockholders’ required rate of return.

D1 Po b Cost of Internal Equity 1) Dividend Growth Model kc = + g 2) Capital Asset Pricing Model (CAPM) kj = krf + j (km - krf )

D1 NPo Net proceeds to the firm after flotation costs! Cost of External Equity Dividend Growth Model knc = + g

Example of Common Stock • Google stock closes at $368.56 at the end of 2007. The company paid $5 dividend in 2007, and expects that dividend to grow at 13%. If Google issue new common stock, the flotation cost will be $50 per share. What is the cost of retained earnings and cost of new common equity capital?

Example of Common Stock • For cost of internal equity: K = D1/ P + g = 5 (1.13) / 368.56 + .13 = 0.145 • For cost of external equity: K = D1/NP + g = 5 (1.13) /(368.56 – 50) + .13 = .148

Example of Common Stock • Issues with dividend growth model -- it is easy -- constant growth is not applicable -- have to estimate the growth rate

Example of Common Stock • If Google’s common stock has a beta of 1.43, and suppose the risk free rate is 5.69%, and the expected rate of return on the market portfolio is 14%. Using the CAPM, what is the cost of capital for Google? K = 0.0569 + 1.43 (0.14 -0.0569) = 0.17 • Note that this is the internal equity, since we do not consider transaction cost

Example of Common Stock • Issues with CAPM -- simple -- does not require dividend growth rate -- need to pick the risk free rate according to the life of the project -- need to estimate beta -- need to estimate the market risk premium

Weighted Cost of Capital • The weighted cost of capital is just the weighted average cost of all of the financing sources.

Weighted Cost of Capital Capital Source Cost Amount Structure debt 6% 2M 20% preferred 10% 1M 10% common 16% 7M 70% 10 M

Weighted Cost of Capital(20% debt, 10% preferred, 70% common) Weighted cost of capital = .20 (6%) + .10 (10%) + .70 (16%) = 13.4%

Cost of New Project • Cost of capital for individual projects should reflect the individual risk of the project • PepsiCo: restaurants, snack foods, and beverages • Use WACC for discount rate for a project only when the project has similar risk to the firm • Cannot use if get into a brand new business