Download

1 / 16

160 likes | 175 Views

Explore the survey results on the scope, system, effectiveness, and entities of external audit of municipalities in Eurosai countries. Understand the various methodologies used and the role of private auditors.

E N D

EXTERNAL AUDIT OF MUNICIPALITIES IN DIFFERENT EUROSAI COUNTRIES Edita Remizovienė, Adviser Audit Department 3 7 October 2015

SURVEY RESULTS • Distributed to all (50) EUROSAI members; • 33 countries sent completed surveys and 3 countries - short information about systems of external audit of municipalities; • Results (as in survey) divided in the 4 main aspects: SCOPE of external audit SYSTEM of external audit of municipalities RELATIONSHIPbetween SAI and other EFFECTIVENESSof audit system

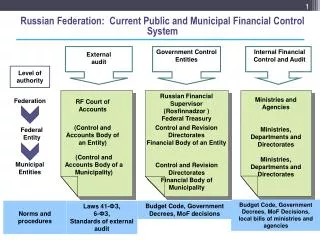

SYSTEM OF EXTERNAL AUDIT Groups of entities that carry out external audit of municipalities in different countries:

VISUAL SYSTEM OF ENTITIES that carry out external audit of municipalities

SAI • SAIs in 7 countries have no mandate to audit municipalities (Belgium, Czech Republic, Germany, Ireland, Luxembourg, Norway, The Netherlands) • Carry out all types of audits (compliance, financial and performance) • Exceptions: • Estonian SAI does not perform financial audits; • Hungarian SAI performs only compliance audits; • Italian SAI – financial audits. • 10 SAIs havespecial methodology for the audit of municipalities • (Albania, Bulgaria (for FA), Hungary, Israel, Latvia, Malta, Croatia, Georgia, Slovakia, Spain)

REGIONAL PUBLIC SECTOR AUDIT INSTITUTIONS (not under SAI) • 9 countries - Lithuania, Poland, Germany, Ireland, Kazakhstan, Norway, Slovakia, Spain and The Netherlands. • Entities which establish these institutions,appoint heads, provide funding and audit institutions are accountable to them: • Mostly carries out all types of audits. In Slovakia only compliance audits are conducted. • Uses methodology prepared by the SAI (Lithuania, Kazakhstan), also by the entity/institution to which the audited entities are subordinate (Poland). In Ireland - Code of Practice prepared and published in accordance with legislation. In other countries use their own. • Heads appointed by the superior entities that supervise their activity – Minister. • Funding – State budget. Resources are passed by the institutions to which the entities are subject.

PRIVATE AUDITORS • In 17 countries private auditors carry out external audits – Azerbaijan, Bulgaria, Czech Republic, Denmark, Estonia, Hungary, Latvia, Malta, Montenegro, Georgia, Greece, Lithuania, Poland, Norway, Serbia, Slovakia, The Netherlands. • Audit entities that select, contract and fund private auditors could be divided into: • Exception – in Montenegro municipalities select and contract private auditors, but remuneration to private auditors for such audits is funded from the state budget. • Mostly private auditors carry out financial audits, but in other countries other types of audits too.

SCOPE OF EXTERNAL AUDIT FINANCIAL STATEMENTS on accrual basis • Municipalities prepare financial statements on accrual basis (balance sheet, cash flow, income statements etc.) in 26 countries. • Financial audits of financial statements of municipalities are carried out by: OnlySAI in Bulgaria, Romania, Bosnia and Hercegovina, Croatia, Moldova, Portugal Only Private auditors in Denmark, Estonia, Latvia, Switzerland, The Netherlands. Azerbaijan, Hungary, Malta, Georgia, Greece, Slovakia, Lithuania, Poland, Portugal, Kazakhstan, Turkey, Serbia, Spain. SAI and Other in Regional audit institutions in Germany, Ireland • in Czech Republic financial audit of financial statements is not required - act 420/2004 Col. requires to perform compliance audit.

FINANCIAL STATEMENTS on accrual basis • Financial statements prepared on accrual basis are consolidated at the national level with financial statements of the State and other funds in 12 countries (Bulgaria, Estonia, Latvia, Lithuania, Romania, Croatia, Germany, Luxembourg, Moldova, Slovakia, Serbia and Turkey) • SAI is responsible for the financial audit of consolidated set.

MUNICIPAL BUDGET EXECUTION Bosnia and Herzegovina (FA), Croatia (FA, CA PA), Estonia (CA), Moldova (FA CA PA),Romania (FA CA PA). Only SAI • Entities that carry out different types of audits on Municipal budget execution statements: • Subsidies allocated to municipalities from the State budget mostly are included to the budget revenue of municipalities (totally – in 28 countries). SAIs carry out audits of the subsidies, but in some countries other audit entities too. Only Private auditors Czech Republic, Denmark Only Regional AI Ireland Albania, Azerbaijan, Bulgaria, Hungary, Greece, Israel, Kazakhstan, Latvia, Lithuania, Malta, Macedonia, Montenegro, Poland, Slovakia, Slovenia, Serbia, Spain and Turkey. SAI and other

SCOPE OF EXTERNAL AUDIT Financial statements prepared by municipality owned enterprises: • Financial audits mostly are carried out by private auditors; • Regional public sector audit institutions - in countries where these institutions are established; • OnlyinAlbania, Bosnia and Herzegovina, Macedonia and Romania SAIs conduct financial audits; • In Israel it is conducted by the Ministry of Interior.

RELATIONSHIP BETWEEN SAI AND OTHER EXTERNAL AUDITORS REGARDING THE EXTERNAL AUDITS OF MUNICIPALITIES

RELATIONSHIPS Clear separation of functions, duties and responsibilities between different audit entities in legislation, but 8 countries also mentioned that there is some duplication of work when different audit entities carry out audits of municipalities: NAO of Lithuania: Duplication when there are specific subjects audited both by the SAI and by the Municipal Control and Audit Service: • Measures to avoid duplications - NAO works with Municipal Control and Audit Services on the basis of Cooperation Agreements.

EFFECTIVENESS OF THE EXTERNAL MUNICIPALITY AUDIT SYSTEM • Mentioned reasons why the system is not effective : • Lack of sanctioning powers in case of improper use of municipality funds; • Auditees are not obliged to execute the post-audit recommendations, as well as due to the fact that most of the conducted audits are ex-post audits; • No possibility to carry out audit of all municipalities every year, which would ensure continuous monitoring of municipalities; • Insufficient IT system linking and coordination, as well as the sharing of audit results; • Duplication of external audit subjects.

EFFECTIVENESS OF THE EXTERNAL MUNICIPALITY AUDIT SYSTEM Changes, improvements in the system that would be beneficial and would make the system more effective: • Intensifying/increasing cooperation between audit entities; • Linking the SAI with the computer systems of audited entities and other audit institutions; • Coordination and access to the audit results of other audit institutions; • Increase the scope/number of municipality audits annually; • Combine audits in several municipalities in areas such as environment, public services, use of assets, water resources; • Enhance human resources ☺