Download

1 / 17

170 likes | 249 Views

Industry Analysis An analysis of the of the industries best operators. September 2008 quarter V 6 months to June 2008. You can keep “afloat” in this rough market!. Analysis performed We have grouped a selection brands together to keep the study simple yet relevant Group 1 volume brands

E N D

Industry AnalysisAn analysis of the of the industriesbest operators.September 2008 quarter V 6 months toJune 2008

You can keep “afloat” in this rough market! Analysis performed • We have grouped a selection brands together to keep the study simple yet relevant • Group 1 volume brands • Group 2 other non luxury • Group 3 prestige brands • Group 4 luxury brands • Group averages and top 30% performers at the selling gross level for each department have been stated against each other. • These performances have been compared for the 6 month ended June 2008 to the quarter ended September 2008.

What does this analysis tell us Issues: • Pressure on the front end margins due to drop in volumes and inventory levels. • Selling gross contribution under pressure in new and used vehicles. Top 30% dealers • Have managed to keep within benchmark in most • Drive best practices and are prepared to change to match market conditions. • Take advantage of opportunities in used cars • Continue to drive performance in the back end

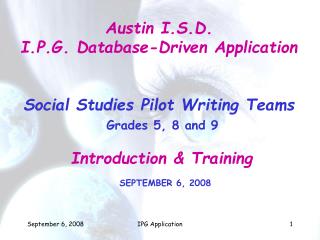

% Net Profit % Sales Top 30% of Dealers V Average

Net Profit % Sales Issues: • The average dealer has experienced a significant drop in Net Profit as a % of sales. • The Top 30% of dealers are still achieving results at or near benchmark levels. Top 30% dealers • Engage all managers and staff – this will develop “buy in” and reduce misunderstanding around required performance and break even levels. • Ensure department managers are aware of their breakeven point. • Compare actual expenses to Benchmark as a percentage of gross whilst maintaining a focus on actual expense $.

New Vehicle Selling Gross % Issues: • All dealers are experiencing pressure on New Vehicle selling Gross % due to the drop in volume and rising inventory levels. • The majority of Top 30% dealers are still achieving results at or near benchmark levels on the back of excellent CRM strategies and maintaining gross profit $ per sales people at levels close to benchmark. Top 30% dealers • Ensure stock levels are within benchmark limits for both dollars and units – based on projected not historic volumes. • Ensure stock vehicles are only ordered with the approval of the DP. • Focus heavily on driving prospect management.

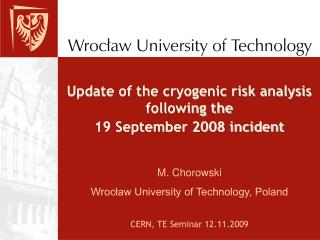

% Used Vehicle Selling Gross % Top 30% of Dealers V Avg

Used Vehicle Selling Gross % Issues: • The Top 30% of used vehicle operators are still operating at benchmark levels. • The current market conditions have seen the gap widen between benchmark and average dealer performance in used vehicles. Top 30% dealers • Adopt a dynamic pricing policy to maximise their R.O.I. • Ensure the utilisation of Stock Provisions • Drive stock turn and have re-assessed their used car strategy for 2009.

% Service Selling Gross % Top 30% of Dealers V Avg

Service Department Selling Gross % Issues: • The current conditions highlight the stability of the dealerships service operations in providing consistent selling gross performance. • Many benchmark dealers have actually improved their performance. Top 30% dealers • Measure and reward individual technician performance. • Have in place a consistent CRM process that drives customer retention. • Have strategies in place that encourage the retention of 3 – 5 year old vehicles. • Understand the financial impact of small improvements in service retention %.

% Parts Selling Gross % Top 30% of Dealers V Avg

Parts Department Selling Gross % Issues: • The current conditions highlight the stability of the dealerships parts operations in providing consistent selling gross performance. Top 30% dealers • Ensure stock levels are within benchmark limits (maximum 45 days) • Drive stock levels by movement code e.g. fast movement parts <14 days • Monitor and drive R.O.I.

Gross Profit per Salesperson per Month Issues: • Falling volumes are impacting on the productivity of sales staff • The ability of salespeople to earn sufficient incomes under current department structures is an issue in some Dealerships and may become a bigger issue moving forward. Top 30% dealers • Compare sales staff productivity levels to benchmark. • Have commission schemes that been reviewed in light of changes in the market, they are exponential in nature.