Download

1 / 5

0 likes | 2 Views

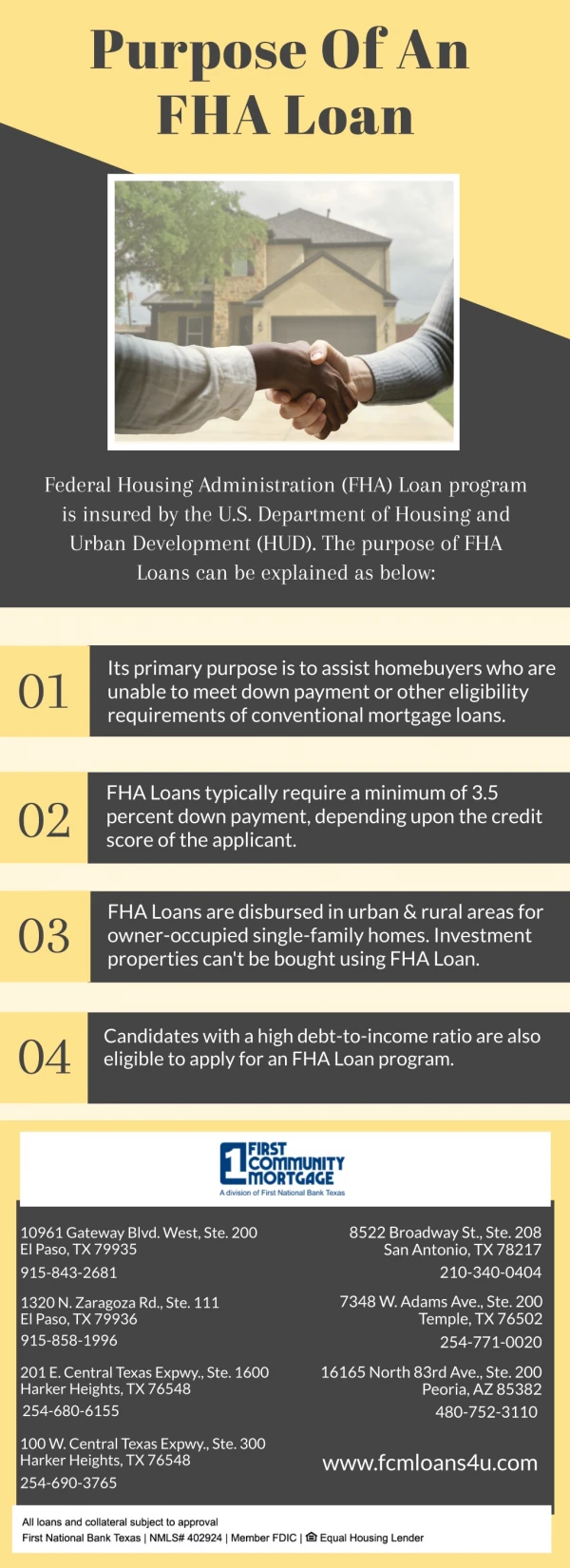

The Federal Housing Administration (FHA) insures these loans, protecting lenders against potential losses and allowing them to offer better terms.

E N D

Introduction Navigating the world of home loans can be a daunting experience, especially for first-time buyers. One particular option that has gained popularity is the FHA loan. But how do interest rates factor into this? In this comprehensive guide, we will explore Understanding How Interest Rates Affect Your Monthly Payments on an FHA Loan and delve into various aspects of FHA loans, from eligibility criteria to repayment terms. What Is an FHA Loan? The Federal Housing Administration (FHA) insures loans made by approved lenders to borrowers with low to moderate incomes. This insurance protects lenders against losses that might occur if a borrower defaults on their loan. As a result, FHA loans often come with lower down payment requirements and more flexible credit score guidelines, making them attractive options for first-time homebuyers. Why Are Interest Rates Important? Interest rates play a critical role in determining your monthly mortgage payments. A lower interest rate means lower monthly payments and less money paid over the life of the loan. Conversely, higher interest rates can significantly increase your financial burden. The Basics of Interest Rates Interest rates are essentially the cost of borrowing money. They fluctuate based on various factors, including: Economic conditions Inflation Federal Reserve policies Market demand for mortgage-backed securities These variables contribute to the overall cost of obtaining an FHA loan. Understanding How Interest Rates Affect Your Monthly Payments on an FHA Loan When you take out an FHA loan, your monthly payment consists of several components: Principal: The amount you borrowed. Interest: The cost of borrowing that principal. Taxes: Property taxes that need to be paid. Insurance: Homeowner's insurance and possibly mortgage insurance premiums (MIP). The formula for calculating monthly payments is complex but generally follows this structure: [ M = P \times \fracr(1+r)^n(1+r)^n - 1 ] Where:

(M) is your monthly payment (P) is the loan amount (principal) (r) is your monthly interest rate (annual rate divided by 12) (n) is the number of payments (loan term in months) Example Calculation For instance, let’s say you take out an FHA loan for $200,000 at a 4% interest rate over 30 years: Convert annual interest rate to a monthly rate: (0.04 / 12 = 0.00333) Total number of payments: (30 \times 12 = 360) Plugging those numbers into our formula gives us a rough estimate of your monthly payment before taxes and insurance. Factors Influencing Interest Rates on FHA Loans Interest rates are influenced by both external economic factors and individual borrower circumstances. Economic Factors Inflation Rate: Higher inflation may lead to increased interest rates as lenders seek compensation for decreased purchasing power. Federal Reserve Policies: The Fed sets benchmark interest rates that influence lending practices across financial institutions. Market Demand: High demand for mortgages can push interest rates up as lenders capitalize on competition. Borrower Factors Credit Score: Higher credit scores generally lead to lower interest rates. Down Payment Size: A larger down payment reduces risk for lenders and can result in better interest rates. Debt-to-Income Ratio: Lenders prefer borrowers whose debts do not exceed a certain percentage of their income, affecting their perceived risk level. Comparing Fixed vs Adjustable Rates When considering an FHA loan, you'll encounter two primary types of interest rates: fixed-rate and adjustable-rate mortgages (ARMs). Fixed-Rate Mortgages These loans maintain the same interest rate throughout their term—typically 15 or 30 years—providing stability in monthly payments. Pros: Predictability in budgeting Protection against rising interest rates Cons: Generally higher initial rates compared to ARMs Adjustable-Rate Mortgages (ARMs) ARMs offer lower initial rates that adjust periodically based on market conditions after an introductory period. Pros: Lower initial costs Potentially lower long-term costs if market rates remain stable Cons:

Uncertainty regarding future payments Risk of significant increases in payments if market conditions change unfavorably Importance of Locking In Your Rate Locking in your interest rate with your lender during the application process can protect you from fluctuations while you finalize your loan details. What Does It Mean to Lock In? Locking in means securing your current rate for a specified period—usually between 30 to 60 days—protecting you from potential increases during this time frame. How Does Down Payment Impact Your Rate? While many people think about down payment percentages primarily concerning affordability, it also affects your loan’s overall cost—including its interest rate. Standard Down Payment Requirements Typically, FHA loans require a minimum down payment of just 3.5%. However, putting down more than this could yield benefits like lower overall costs and potentially better terms. Role of Mortgage Insurance Premiums (MIP) FHA loans come with MIP—an added expense that protects lenders against borrower default risks but adds to your total financing costs each month. Types of MIP Upfront MIP: Paid at closing; typically around 1.75% Annual MIP: Paid monthly as part of your mortgage payment; varies based on factors such as LTV ratio and loan amount Understanding Amortization Schedules An amortization schedule outlines how much principal vs. interest you'll pay over the life of the loan, providing clarity on how these components evolve over time. | Month | Principal Payment | Interest Payment | Remaining Balance | |-------|-------------------|------------------|--------------- ----| | 1 | $500 | $667 | $199,500 | | 2 | $503 | $664 | $198,997 | | … | … | … | … | Trevor Aspiranti with Extreme Loans Trevor Aspiranti with Extreme Loans

Evaluating Loan Offers from Lenders As you embark on finding an appropriate lender for your FHA loan in Ann Arbor MI or beyond, it’s crucial to evaluate offers critically based not only on quoted rates but also other fees associated with securing the mortgage. Key Considerations Compare Annual Percentage Rate (APR), which reflects total borrowing costs Negotiate terms where possible Look for customer service ratings among different lenders Common Misconceptions About Interest Rates and FHA Loans Throughout discussions surrounding mortgages there often arise misconceptions worth clarifying: Myth #1: Lower Credit Scores Always Mean Higher Rates This isn’t universally true; some lenders may have specialized programs accommodating lower scores without imposing excessive fees or penalties. Myth #2: All Lenders Offer Identical Terms Each lender structures its products differently; shopping around can lead you toward unexpected savings! FAQs About FHA Loans and Interest Rates FAQ #1: Can I refinance my existing FHA loan? Yes! You can refinance through options like the FHA streamline refinance, which allows homeowners with existing FHA loans who meet specific criteria access reduced paperwork and quicker processing times! FAQ #2: What happens if I can't afford my payments due to changing rates? If you're struggling financially due to increasing payments consider speaking directly with your lender about possible relief options they may offer! FAQ #3: Do I need perfect credit to qualify for an FHA mortgage? Not at all! While having good credit helps secure favorable terms many lenders accept applicants with scores below traditional thresholds provided they demonstrate reliability through alternative measures! FAQ #4: Are there limits on how much I can borrow with an FHA loan? Absolutely! Each county has specific limits set by HUD; checking these beforehand ensures realistic expectations when budgeting! FAQ #5: When should I lock my rate during my application process? Typically locking once you've settled on preferred terms makes sense—and doing so early helps mitigate risks tied into fluctuating markets so always stay vigilant! FAQ #6: What are common pitfalls new homeowners face when applying for an FHA mortgage? Common missteps include failing to understand fee structures or neglecting research regarding local housing markets which leads unwary buyers astray—research thoroughly before signing anything! Conclusion

Understanding how interest rates affect your monthly payments on an FHA loan is crucial if you're looking to make informed decisions about home financing options available today! By grasping key concepts like fixed versus adjustable- rate loans along with recognizing Look at more info various influences upon both market trends as well individual circumstances—mortgage seekers gain clarity needed when navigating through complexities inherent within real estate transactions! Whether you're exploring options such as bad credit fha loans Ann Arbor or seeking advice tailored specifically towards first-time homebuyers—the knowledge gleaned here empowers individuals toward confident choices moving forward!