Download

1 / 5

0 likes | 1 Views

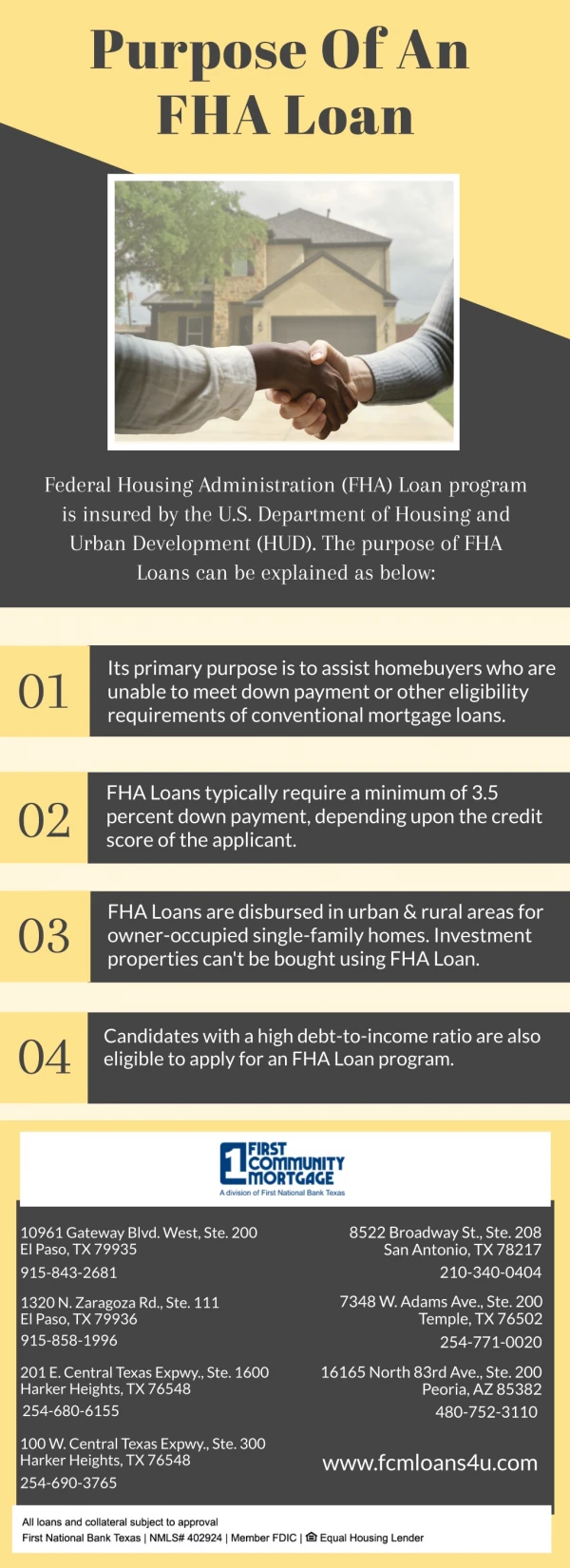

Homebuyers using an FHA loan can also receive assistance through local or state programs aimed at promoting affordable housing initiatives.

E N D

Introduction Navigating the world of home financing can be daunting, especially for first-time buyers. With various options available, understanding the nuances of conventional loans versus FHA loans is paramount. Both loan types serve distinct purposes and attract different buyer demographics. In this article, we will delve into the exploration of alternatives—specifically, when one should consider a conventional loan over an FHA loan. As we journey through this topic, we'll discuss various elements such as eligibility requirements, down payment assistance programs, credit score implications, and regional considerations like FHA loan Ann Arbor MI and FHA mortgage lender Ann Arbor MI. By the end of this extensive guide, you’ll have a clearer perspective on which option may best suit your financial goals. Understanding FHA Loans What is an FHA Loan? An FHA (Federal Housing Administration) loan is a government-backed mortgage designed to promote homeownership among individuals who may have lower credit scores or limited funds for a down payment. It typically allows for lower down payments—sometimes as low as 3.5%—making it accessible for many first-time homebuyers. Key Features of FHA Loans Lower Down Payments: As mentioned earlier, the minimum down payment for an FHA loan can be as low as 3.5%. Flexible Credit Requirements: Borrowers with credit scores as low as 580 can qualify for an FHA loan, while those with scores between 500 and 579 might still be eligible with a larger down payment. Mortgage Insurance: FHA loans require both upfront and annual mortgage insurance premiums (MIP), which protect lenders in case of borrower default. Benefits of FHA Loans Easier Qualification: The flexible credit requirements make it easier for individuals with less-than-perfect credit to secure financing. Assistance Programs: Various FHA down payment assistance Ann Arbor programs exist to help buyers overcome financial barriers. Property Versatility: An FHA 203k rehab loan Ann Arbor allows buyers to finance both the purchase price and renovation costs in one mortgage. Exploring Conventional Loans What is a Conventional Loan? A conventional loan is not backed by any government entity; instead, it’s offered by private lenders such as banks and credit unions. These loans generally adhere to standards set by Fannie Mae and Freddie Mac.

Key Features of Conventional Loans Higher Credit Score Requirements: Typically requiring a minimum credit score of around 620 or higher. Down Payment Options: While some lenders offer options as low as 3%, traditional down payments are usually around 20%. No Mortgage Insurance for High Down Payments: Borrowers who put down at least 20% avoid paying Private Mortgage Insurance (PMI). Benefits of Conventional Loans Potentially Lower Interest Rates: A good credit score can yield more favorable rates. Flexibility in Property Types: Unlike FHA loans that have specific property requirements, conventional loans offer more flexibility. No Upfront Mortgage Insurance Premiums: This can save borrowers thousands upfront compared to FHA loans. When Should You Consider a Conventional Loan? Assessing Your Financial Situation Before deciding between an FHA or conventional loan, it's essential to evaluate your financial position meticulously. Factors to Consider: Credit Score: If your score is above 620, you might find better interest rates with a conventional loan. Down Payment Capacity: If you can afford a larger down payment (at least 20%), consider going conventional to avoid PMI. Long-Term Plans: Planning on staying in your home long-term may make higher upfront costs worthwhile if you secure lower monthly payments through interest savings. Comparative Analysis Between Conventional vs FHA Loans | Feature | FHA Loan | Conventional Loan | |--------------------------------|------------------------------|-----------------------------| | Minimum Down Payment | 3.5% | Typically 20% | | Credit Score Requirement | As low as 580 | Usually above 620 | | Mortgage Insurance Required | Yes | Only if <20% down | | Property Eligibility | More strict | More flexible | Trevor Aspriranto Mortgage Broker - Extreme Loans Trevor Aspriranto Mortgage Broker - Extreme Loans Specific Scenarios Favoring Conventional Loans

First-Time Home Buyers in Michigan While many first-time buyers gravitate towards FHA loans Michigan, there are circumstances where a conventional loan is worth considering: Scenario Examples: If you're financially stable yet new to home buying and can meet the conventional loan criteria. Looking at properties that don’t qualify under FHA approved condos Ann Arbor but are perfect under conventional standards. Bad Credit Situations In scenarios where individuals possess bad credit but have substantial assets or income sources: A conventional lender might overlook certain adverse factors when assessing overall financial health. Strategies for Improvement: If you're considering transitioning from an FHA to a conventional loan due to bad credit issues: Work on improving your credit score through timely payments and reducing debt. Save towards that larger down payment which could lead lenders toward approving your application even with existing blemishes on your record. 【Exploring Alternatives】Important Factors Influencing Your Decision 【Interest Rates Comparison】 One significant difference between these two types of loans lies in their interest rates: Current Market Trends As of now, conventional loans often offer slightly lower rates than their FHA counterparts due to perceived risk levels by lenders based on borrower profiles. Predictive Analysis Consider consulting local lenders or online comparison tools—for instance, searching "fha loan rates Ann Arbor"—to determine current market conditions before making decisions. 【Evaluating Additional Costs】 Understanding additional costs associated with each type of mortgage will further clarify which option suits you best: 【Closing Costs Breakdown】 Both types of loans will incur closing costs; however: Closing costs associated with an FHA mortgage lender Ann Arbor MI may differ from those linked to private institutions offering conventional mortgages. Evaluate if certain fees could be rolled into the cost of the home under specific programs associated with either type of financing. 【Exploring Alternatives】Market Conditions Affecting Your Choice 【Local Economy Insights】

Understanding local real estate trends—especially in areas like Ann Arbor County—can influence whether pursuing an FHA or conventional mortgage makes more sense based on demand dynamics. Are homes appreciating quickly? Will renting become more expensive than owning shortly? These questions will require research into regional economic indicators that directly affect housing markets across Michigan and beyond. 【Reputation Matters】 Choosing reputable lenders plays a crucial role regardless if you're leaning toward an FHA or conventional route: 【Checking Lender Credentials】 Before signing any agreements: Verify that they’re registered within Michigan’s real estate framework. Look into customer reviews regarding experiences with both types of financing options available through them—a great way to gauge reliability! 【Frequently Asked Questions (FAQs)】 FAQ #1: What are the primary differences between an FHA loan and a conventional loan? The main differences include eligibility requirements, down payment amounts needed, insurance premiums required for each type, and how they handle income verification processes during applications. FAQ #2: Can I switch from an FHA loan to a conventional one later? Yes! Many homeowners refinance from an FHA refinance Ann Arbor option into a conventional one after building equity or improving their credit scores significantly enough within several years post-purchase! FAQ #3: Are there special programs available for first-time home buyers? Absolutely! Many states—including Michigan—offer unique assistance options tailored specifically made possible through collaborations between local governments along side lending institutions accommodating prospective homeowners looking at acquiring property via either paths mentioned here! FAQ #4: Is there any penalty for paying off my mortgage early? While most traditional mortgages impose penalties against early repayment plans upon completion; however not all do so! Always check fine print when reviewing contracts prior signing anything beforehand! FAQ #5: How do I find out what my local market looks like? Utilize resources like real estate agents’ reports about recent sales activity surrounding neighborhoods plus online platforms summarizing areas’ characteristics based upon historical data compiled over time analyzing statistics relative those regions respectively! FAQ #6: Which option would work best given my current financial situation? Without knowing specifics concerning individual circumstances involved it’s tough saying definitively—but starting conversation centered around current income levels alongside existing debt ratios would provide insight into determining feasible choices available moving forward towards achieving homeownership aspirations successfully! Conclusion

Deciding between an FHA mortgage loan versus pursuing alternatives such as traditional/conventional avenues requires careful consideration rooted deeply within understanding personal finances alongside Visit website broader market conditions affecting potential purchases made today! By evaluating criteria laid out throughout this extensive guide about exploring alternatives when choosing suitable funding routes—it’s clear no one-size-fits-all answer exists—but equipping oneself proudly armed knowledge gained here today means navigating waters ahead confidently without fear stepping forth boldly taking next steps needed toward fulfilling dream owning homes soon becoming reality!