Download

1 / 24

250 likes | 553 Views

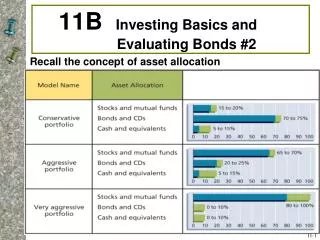

11B Investing Basics and Evaluating Bonds #2. Recall the concept of asset allocation. 11- 1. One Effect of Asset Allocation: A Weighted Total Return. Ultraconservative “Investors” Are Really Just “Savers”. People who invest very conservatively

E N D

11B Investing Basics and Evaluating Bonds #2 Recall the concept of asset allocation 11-1

Ultraconservative “Investors” Are Really Just “Savers” • People who invest very conservatively • They do not get ahead financially over the long term because taxes and inflation offset most of their interest earnings • Remember “The Rule of 72”? • 72/4% = 18 years • 72/8% = 9 years (money doubles much faster)

Identify the Types of Investments You Want to Make Do You Want to Lend Your Money or Own an Asset? • Debts – “loanership” (lending) investments. • Fixed Maturity – the borrower agrees to repay the principal to the investor on a specific date. • Fixed Income – the borrower agrees to pay the investor a specific rate of return for use of the principal. • Equities – “ownership” investments. • Potential for a higher return by sharing in profits

The Risk Pyramid Reveals the Trade-offs Between Investment Risk and Return

Inflation • To beat inflation, one must invest money so that it earns a higher after-tax return than the inflation rate • Real Rate of Return – the return after subtracting the effects of both inflation and income taxes. Example: 10% return, 7.5% after taxes (25% tax bracket), 4% inflation, real rate of return of 3.5% after taxes and inflation

Objective 5Recognize Why Investors Purchase Corporate Bonds Corporate Bonds • A corporation’s written pledge to repay a specified amount of money with interest • An interest-only loan • Considered safer than co. stocks • A “fixed-income” security • A form of debt financing (bond owners repaid in future) 11-7

Corporate Bonds • Face Value • Dollar amount bondholder receives at bond’s maturity date • Usually $1,000 • Coupon rate • Stated interest rate • Interest payments made every six months • Example: $1,000 x 5.8% = $58 (in two $29 payments) • Maturity Date = date on which face value repaid; generally 1 to 30 years 11-8

Corporate Bonds • Bond Indenture • Legal document describing conditions of the bond issue • Trustee • Financially independent firm that acts as the bondholder’s representative • Usually a commercial bank or other financial institution 11-9

Why Corporations Sell Bonds • To raise funds for major purchases • To fund ongoing business activities • When difficult or impossible to sell stock • To improve financial leverage • Interest paid to bondholders is tax- deductible for the firm 11-10

Types of Corporate Bonds • Debenture • Unsecured debt • Investors become “creditors” if company fails • Backed only by the reputation of the issuing company; most corporate bonds are this type • Mortgage Bond • Secured by various assets of the issuing firm, such as real estate and property • Lower interest (coupon) rate since debt is secured 11-11

Types of Corporate Bonds • Convertible Bond • Can be exchanged, at the owner’s option, for a specified number of shares of the corporation’s common stock • Generally, coupon rate on a convertible bond is 1% to 2% lower than the rate paid on traditional bonds • Would only want to convert when stock price gets higher than the bond’s equivalent value in stock 11-12

Provisions For Repayment Call Feature of Bonds • Corporation can “call in” or buy back outstanding bonds before the maturity date • Most corporate bonds are callable • Call-protected for first 5 to 10 years after issue • A firm calls a bond issue if the coupon rate they are paying is much higher than the market rate • Like consumers refinancing to lower-rate mortgage What is the effect of called back bonds on investors? 11-13

Bond Provisions For Repayment • Sinking Fund • Corporations deposit money annually • Trustee uses the money to retire the bond issue prior to maturity • Serial Bonds • Bonds of a single issue that mature on different dates • Example: After first 10 years, over the next 10 years, 10% of bonds mature each year 11-14

Bond Why Investors Purchase Corporate Bonds • Interest Income - “Fixed Income” • Registered Bond- tracked electronically • Coupon and principal paid to registered owner (check or direct deposit) • Registered Coupon Bond • Registered for principal only • Coupon must be presented to obtain payment • Zero-Coupon Bond • Pays no interest • Sold at a discount from face value • Redeemed at face value at maturity 11-15

Why Investors Purchase Corporate Bonds • Dollar Appreciation of Bond Value • Bond values change with market interest rates • Bond value vs. Interest rates = inverse relationship • If Market rate< Coupon rate Price > Face value • If Market rate > Coupon rate ← Price < Face value • Bond values change with the financial condition of the issuing company or government unit • Bond Repayment at Maturity • Face value repaid on maturity date (will be worth less due to inflation) • Bondholders may keep till maturity or sell • Portfolio diversification beyond stock and cash assets 11-16

Approximate Bond Value Formula • 5.875% interest on ($1,000 bond) = $58.75 • New issues paying 5% (decrease in coupon rate) • Dollar amount of interest$58.75 Comparable interest rate = 5% (.05) = $1,175 • Bond worth more than face value because it pays interest rate higher than current market rate • New issues paying 6.5% (increase in coupon rate) • Dollar amount of interest$58.75 Comparable interest rate = 6.5% (.065) = $903.85 • Bond worth less than face value because it pays interest rate lower than current market rate

Premiums and Discounts When a bond is first issued, it is sold in one of three ways: • at its face value • at a discount below its face value or • at a premium above its face value.

Price Changes for Bonds What does this graph tell you?

Objective 6Evaluate Bonds When Making an Investment • Sources of Information – The Internet • The issuing firm’s website • www.bondsonline.com • http://bonds.yahoo.com • Financial coverage of bond transactions • Wall Street Journal, Barrons, Internet • Other Sources of Information • Business Periodicals • Federal Agencies • www.federalreserve.gov • www.treasury.gov • www.sec.gov 11-20

Corporate Bond Quotes • The first bond in the list: • Matures in 2036 • Current price = 93.51% of par (discount) = $935.10 • Pays an annual coupon rate of 5.875% = $58.75 • Yield-to-Maturity = 6.365% (considers bond maturity date) • Current yield = 6.283% = 5.875/93.51 (interest/price) 11-21

Decisions Bond Investors Must Make • Decide on risk level. • Investment grade bonds: top 4 grades (BBB, A, AA, AAA) • Junk bonds (a.k.a., high yield bonds): lower rated and higher risk • Decide on maturity. • Match to financial goals • Determine the after-tax return. • Taxable versus tax-exempt

Wrap Up • Chapter Quiz • Concept Check 11-5- Calculate Semi-annual Interest and Reasons That Investors Buy Bonds • Concept Check 11-6- Current Value of Bonds; Explain Bond Ratings