Download

1 / 11

110 likes | 236 Views

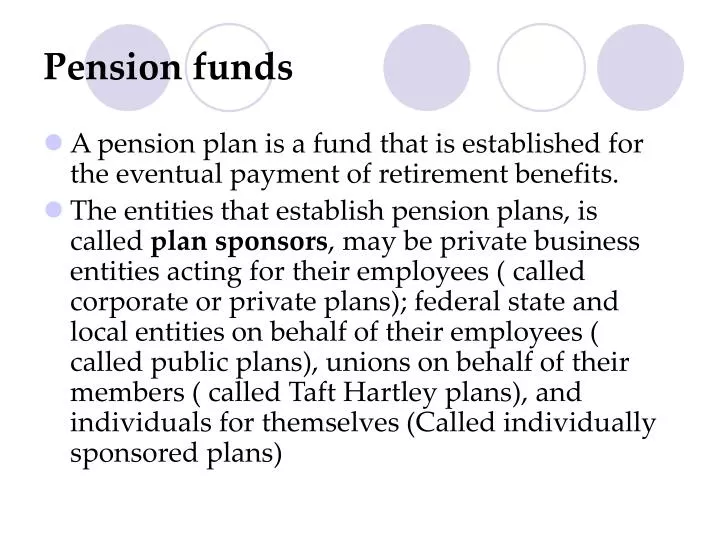

Pension funds. A pension plan is a fund that is established for the eventual payment of retirement benefits.

E N D

Pension funds • A pension plan is a fund that is established for the eventual payment of retirement benefits. • The entities that establish pension plans, is called plan sponsors, may be private business entities acting for their employees ( called corporate or private plans); federal state and local entities on behalf of their employees ( called public plans), unions on behalf of their members ( called Taft Hartley plans), and individuals for themselves (Called individually sponsored plans)

Types of pension plans • Defined benefit plans • Defined contribution plans

Defined benefit plans • The plan sponsor agrees to make specified dollar payments annually to qualifying employees beginning at retirement (or in case of death before retirement). • These payments occur monthly. • The retirement payments are determined by a formula that usually takes into account the length of service of the employees and the employee’s earnings. • Defined benefit plans that are insured by the life insurance products are called insured benefit plans.

Defined contribution plan • The plan sponsor is responsible only for making specified contributions into the plan on behalf of qualifying participants, not specified payments to the employees after retirement.

Differences between Defined benefit plans & Defined contribution plans • In Defined benefit plan – The Plan Sponsor, 1. Guarantees the retirement benefit, 2. Makes the investment choices, 3. Bears the investment risk, if the investment doesn’t earn enough. • In a Defined contribution plan, the employer doesn’t guarantee any retirement benefit.

Hybrid Pension plans • Hybrid pension plans are combinations of defined benefit plans and defined contribution plans. • The most common hybrid pension plan is cash balance plan.

Cash balance plan • A cash balance plan is a defined benefit plan in that, the plan benefits are fixed based on a formula. • Investment responsibility is borne by the employer. • A cash balance plan is a defined contribution plan in that, each participant has an account, which is credited with the individuals contribution and the account is credited with interest linked to some fixed or variable index, such as consumer price index.

Properties and pricing of financial assets • Properties of financial assets are – • Money ness • Divisibility and denomination • Reversibility • Cash flow • Term to maturity • Convertibility • Currency • Liquidity • Return predictability • Complexity • Tax status.

Duration • The approximate percentage change in price for a 100 basis point change in interest rates around the prevailing yield. Even for very low yield, the measure of price sensitivity is nicely estimated with duration.

Properties of duration: • Bonds with same coupon rate and same yield, the longer the maturity the greater the duration • Bonds with same coupon rate and same yield, the lower the coupon rate the greater the duration • Lower the initial yield the greater the duration for a given bond.

Please read – • Macaulay duration ( page 187) • Effect of coupon rate ( page 181-182)