Download

1 / 81

820 likes | 1.04k Views

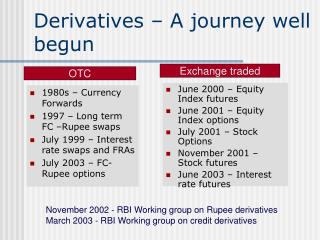

Derivatives – A journey well begun. Exchange traded. OTC. June 2000 – Equity Index futures June 2001 – Equity Index options July 2001 – Stock Options November 2001 – Stock futures June 2003 – Interest rate futures. 1980s – Currency Forwards 1997 – Long term FC –Rupee swaps

E N D

Derivatives – A journey well begun Exchange traded OTC • June 2000 – Equity Index futures • June 2001 – Equity Index options • July 2001 – Stock Options • November 2001 – Stock futures • June 2003 – Interest rate futures • 1980s – Currency Forwards • 1997 – Long term FC –Rupee swaps • July 1999 – Interest rate swaps and FRAs • July 2003 – FC-Rupee options November 2002 - RBI Working group on Rupee derivatives March 2003 - RBI Working group on credit derivatives

Rupee Interest rate swaps • Swap market is now 6 years old • FY ‘04 has seen tremendous growth in volumes and outstanding contracts • Increasing volumes have led to lower bid-offer spreads for some of the price points • No of market players have increased • More banks and PDs have joined the market • Corporate activity has also increased • Emerging consensus about benchmark rates • OIS and MIFOR have emerged as two key swap curves

Agenda • Introduction to Interest Rate Swaps (IRS) • Overnight Index Swaps • Uses of Overnight Index Swaps

What is an Interest Rate Swap (IRS)? • IRS is an agreement between two counterparties to exchange interest payments based upon a ‘notional principal’ on specified dates over a specified period • Interest payments are calculated on a notional principal which is not exchanged • Typically one party pays interest based on an agreed fixed rate (fixed rate payer) and the other party pays interest linked to a floating benchmark rate (floating rate payer)

Receives fixed Pays fixed Bank B Bank A Pays floating Receives floating Interest Rate Swap (IRS) • Typical Interest Rate Swap

The Swap Mechanism IOC borrows from the fixed market due the absolute advantage and ACC Borrows from the Floating Rate Market due to the comparative advantage. And both the companies enter a Swap Deal. 9.95% IOC Ltd AAA-Rated ACC Cement AA Rated MIBOR 10.00% MIBOR+1.00%

The swap of coupon flows results in benefit to both the companies Cost to IOC after swap

Therefore the total gain of 50 bps is equal to the Quality difference spread. • The total gain is 0.25%+0.25% = 50bps = 1.20% -0.7%

Elements of a typical IRS • Notional Principal • there is no exchange of principal • the floating and fixed interest rate calculations are for a pre-decided principal • Exchange of coupon streams • Normally fixed rate coupon for a floating rate coupon; can also be floating rate for another floating rate • Fixed rate • predetermined rate, valid for the entire life of the swap • Floating rate • linked to a benchmark rate which is reset periodically • Interest payments are net settled

Rupee Swaps • 6 Month MIFOR and overnight MIBOR as popular floating rate benchmarks • MIFOR swaps more liquid • Lack of liquid term money market based benchmark • Interest in long tenure swaps has also grown • MIFOR curve has lengthened upto 10 yrs OIS curve is active upto 5 yrs • However, bid –offer spreads are still relatively high (15-20 bps) for more than 5 year swaps • Bid-offer on 15 year GOI Sec is less than 1 bps

Floating rate benchmark • Should be a market determined rate which is transparent and mutually acceptable to counterparties • Possible floating rate benchmarks in India are: • Overnight or ‘Call Money” Rates • Inter-bank term money rates • Commercial Paper yields • INBMK

Overnight rates are likely to be the most relevant and acceptable floating rate benchmark • Overnight money markets are deep and liquid and the Overnight Index is well accepted and extensively used as a market standard • The methodology for calculating the Overnight Index is transparent and accepted by counterparties • Overnight rates have been the most widely accepted benchmark for floating rate bond issues in the cash market. • Therefore, Overnight Index Swaps (OIS) with the floating rate indexed to an Overnight reference rate are expected to be the main product in the swap market initially

Overnight Index (contd.) • Interest rate swaps indexed to other floating rate benchmarks such as 14 day,1 month, 3 month MIBOR should ‘hopefully’ develop as well

Overnight Index Swaps (OIS) - An Example • Bank A wants to pay fixed rates and receive Overnight floating rates • Bank B wants to pay Overnight floating rates and receive fixed rates • The two banks enter into an OIS • Terms to consider • Day Count Conventions • Actual/365 • Start Date of the transaction - Tomorrow • Overnight Benchmark • NSE Overnight MIBOR, Reuters MIBOR, Reuters MIOR • Settlement date convention • Modified following business day • Interest computation methodology • Compounding of Overnight rates for every business day

OIS Details • Bank A enters into a 7 day OIS with Bank B, where Bank A pays a 7 day fixed rate @ 8.50% and receives Overnight MIBOR • Terms • Trade Date 23rd August,2004 • Day Count Basis Actual number of days/365 • Amount INR 100 crores • Start Date 24th August,2004 • End Date 31st August,2004

OIS Details (Continued) • Terms • O/N benchmark NSE O/N MIBOR Act/365 (Bank B pays) • Fixed Rate 8.50 % simple Act/365 (Bank A pays) • Interest Computation The fixed rate is computed on a simple basis, but the floating rate would be compounded every Mumbai business day. • Interest Settlement The settlement on the swap would be on a net basis. For e.g.., if the interest as per the fixed rate is higher than floating rate, Bank A pays the difference

Computing OIS Cashflows Overnight index for 7 days O/N MIBOR Notional Principal Accrued Interest Day 1 7.83% 1,000,000,000 214,521 Day 2 7.76% 1,000,214,521 212,648 Day 3 7.32% 1,000,427,169 200,634 Day 4 8.02% 1,000,627,803 219,864 Day 5 & 6 8.11% 1,000,847,666 444,760 Day 7 8.22% 1,001,292,427 225,497 Total interest accrued on the floating leg (Bank B pays) = 1,517,923 Interest accrued on fixed leg (Bank A pays) = 1,630,137 1,000,000,000*8.50%*7/365 Net interest payment by Bank A on the settlement date = 112,214

Swap Pricing • No-arbitrage pricing condition • PV (Fixed Cash Flows) = PV (Floating Cash Flows) • Zero value contract on start date : The PV of floating rate cash flows less PV of fixed rate cash flows should be zero • A swap is a zero value contract on the Start Date of the transaction : SV = 0 V1 -- V2 = 0 OR V1 = V2

Swap Pricing • Fair Pricing on initiation • based on market’s expectation of future short-term rates . On the start date, the value of the floating leg is equal to par • For the fixed leg to be equal to par, the coupon rate should be equal to the yield on a par coupon bond (assuming no default risk)

OIS - Uses • As per RBI guidelines • Banks • Financial Institutions • Primary Dealers and • Corporates have been permitted to transact in OIS • OIS can be used for • Asset-Liability Management • Hedging Interest Rate Risks • Reducing Interest cost without sacrificing liquidity and by utilising minimal capital, thereby ensuring a higher return on capital

Terminology of IRS and FRA markets • To buy a swap = buying a FRA pay a fixed rate under a swap pay a fixed rate under a FRA • To sell a swap = selling a FRA receive a fixed under a swap receive a fixed rate under a FRA

Summary : IRS and FRA important tools for money markets • Credit risk minimal compared to other Money-Market Instruments • Replicate cash market transactions, but with lower capital requirements • Will reinforce the development of the cash market benchmarks • Easy to unwind, if required • Efficient trading & hedging tool

Example2: • A company accepts a 1 year FD for a Face Value of Rs 5 crores. • Deposits was issued at a rate of 8.00% • Fixed Deposits has a residual maturity maturity of 12 days • The company is the view that the Call rates will remain in the band of 5.60%-5.90%. • Thus the Company is of the view that by entering a IRS it can reduce its effective cost.

Example 3: IRS to Improve the Effective Yield on Asset. • A company has invested Rs 5 crores in Treasury bills whose residual maturity is 12 days at a Money market yield of 5.70% • The company is of the view that the Overnight rates will be high in a particular range over the next fortnight. • Hence the company strikes a deal, wherein it will receive floating rate and pay fix rate.

Valuation of Swap • Part I : Accrual part • Part II :Mark to market

Identify and calculate Possible Payoffs and cashflow from IRS Swaption