Download

1 / 11

110 likes | 317 Views

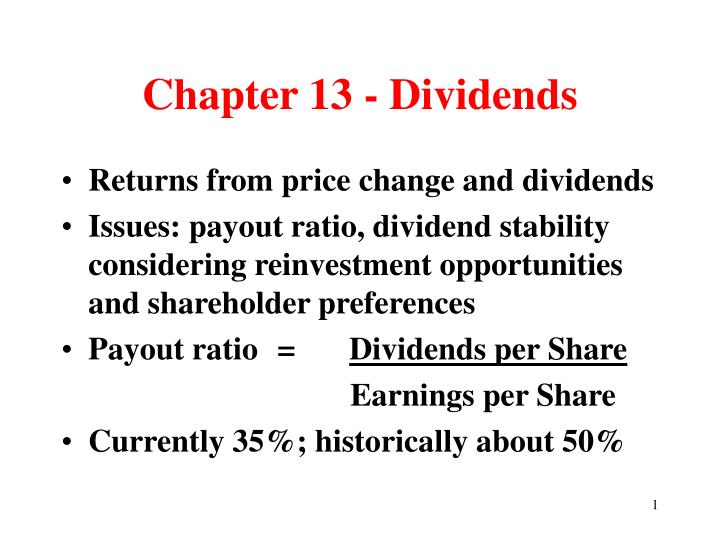

Chapter 13 - Dividends. Returns from price change and dividends Issues: payout ratio, dividend stability considering reinvestment opportunities and shareholder preferences Payout ratio = Dividends per Share Earnings per Share Currently 35%; historically about 50%. What to Do With The Money?.

E N D

Chapter 13 - Dividends • Returns from price change and dividends • Issues: payout ratio, dividend stability considering reinvestment opportunities and shareholder preferences • Payout ratio = Dividends per Share Earnings per Share • Currently 35%; historically about 50%

What to Do With The Money? • Corporate cash holdings growing rapidly • Choices: Reinvest in new products? • Pay dividends? • Make acquisitions? • Do stock buybacks?

Dividends & Stock Price • Major change in tax law: both dividends and long-term capital gains taxed @ 15% • Makes part of chapter irrelevant • Still an issue – should company reinvest profits in itself to take on new projects providing high returns and growing stock price or pay earnings to shareholders? • Reinvestment opportunity – residual theory

Other Approaches • Residual dividend theory – “leftovers” • Clientele effect • Information effect; communications tool • Expectations effect – revise perceptions? • Empirical evidence – very mixed but may slightly favor nonpayers but recently challenged

Dividends in Practice • Usually quarterly as approved by Board of Directors • Legal restrictions • Liquidity position • Other sources of financing • Earnings predictability

Other Dividend Matters • About 75% of S&P 500 pay dividends • Dividend Yield currently 1.95% • Dividend Reinvestment Programs Reinvest dividends by buying same stock • Dividends have been increasing but not as fast as profits and stock prices

Alternative Policies • Constant payout ratio • Small regular plus year-end extra • Stable amount per share – most common • Usually profits grow faster than dividends • “Wait until we’re certain” attitude • Yearly dividends since 1885 – Eli Lily • GE (1894), PPG (1899), Pfizer (1901)

Stock Dividends and Splits • New shares issued on pro rata basis to current shareholders • No economic consequences • Accounting differences only • Split: new shares 25% over existing • Stock dividends – increase under 25% • Reverse splits – reduce number of shares • Should increase price and avoid delisting

Stock Repurchases • Boosts EPS (price?); uses excess cash • Buy as an “undervalued investment” • Don’t have to complete; effect on price? • Can’t go on forever • Buybacks must be publicly announced • Analogy: buybacks = dating; div = marriage • Bottom line: it’s capital restructuring

Microsoft’s Biggie • First annual dividend in 2003 (8¢/share); • Double to 16¢ early 2004 • July 2004 announced Regular dividend doubled to 32¢ ($3.5 bil) + $3/share one-time special dividend ($32 bil) + $30 billion share buybacks over four years • Driven by $56 bil cash, high profits, new tax law.