Download

1 / 40

400 likes | 421 Views

Learn about the fundamental economic problem, factors of production, productivity, and more in this comprehensive guide to economics. Explore concepts such as scarcity, utility, circular flow, and economic growth.

E N D

The Fundamental Economic Problem • Most people seem to want more than they already have. • Scarcity is the condition that results from society not having enough resources to produce all the things people would like to have.

The Fundamental Economic Problem • Economicsis the study of how people try to satisfy what appears to be seemingly unlimited and competing wants through the careful use of relatively scarce resources. • Needs and Wants • A need is a basic requirement for survival and includes food, clothing, and shelter • A want is a way of expressing a need

Three Basic Questions • WHAT to Produce • society cannot have everything its people want, so it must decide WHAT to produce. • HOW to Produce • Should factory owners use mass production methods that require a lot of equipment and few workers, or should they use less equipment and more workers? • FOR WHOM to Produce • the things produced must be allocated to someone

Factors of Production • Land • Natural resources not created by humans • Capital • The tools, equipment, machinery, and factories used in the production of goods and services • financial capital, the money used to buy the tools and equipment used in production • Capital is unique in that it is the result of production

Factors of Production • Labor • people with all their efforts, abilities, and skills • Unlike land, labor is a resource that may vary in size over time • Entrepreneurs • a risk-taker in search of profits who does something new with existing resources • They provide the initiative that combines the resources of land, labor, and capital into new products

What is Economics? • There are four key elements to this study: • description, analysis, explanation, and prediction. • Description • we need to know what the world around us looks like • The Gross Domestic Product (GDP) is the most comprehensive measure of a country’s total output and is a key measure of the nation’s economic health

What is Economics? • Analysis • it helps us to discover why things work and how things happen. • Explanation • it is useful and even necessary to communicate this knowledge to others • If we all have a common understanding some economic problems will be much easier to address

What is Economics? • Prediction • The study of economics can help to make the best decision in many situations • Economics can help predict what may happen in the future, as well as consequences of different courses of action

Goods and Services • Economic products– goods and services that are useful, relatively scarce, and transferable to others • Good–an item that is economically useful or satisfies an economic want • consumer goodis intended for final use by individuals • capital goodsWhen goods are used to produce other goods and services • Service– work that is performed for someone

Paradox of Value • Is water a want or a need? • Are diamonds a want or a need? • Which is more valuable? • Scarcity is required for value • But Scarcity is not enough Utility • Utility – The satisfaction or usefulness of an item. • For something to have value it must be scarceand have utility

Circular Flow Model • Factor Markets • the markets where productive resources are bought and sold • Product Markets • These are markets where producers sell their goods and services to consumers • Markets serve as the main links between individuals and businesses

Economic Growth • Economic growth occurs when a nation’s total output of goods and services increases over time

Productivity • Productivity, is a measure of the amount of output produced by a given amount of inputs in a specific period of time • Getting more out of the same amount put in.

Division of labor takes place when work is arranged so that individual workers do fewer tasks than before Workers doing a specific task. Specialization takes place when factors of production perform tasks that they can do relatively more efficiently than others Welders welding and electricians doing the wiring. Division of Labor and Specialization

Investing in Human Capital • One of the main contributions to productivity comes from investments in human capital • human capital -- the sum of the skills, abilities, health, and motivation of people • Businesses can invest in training and other programs that improve their workers • Individuals can invest in their own education – high school, college, etc

Trade off • People face trade-offs, or alternative choices, whenever they make an economic decision.

Trade Off • Using a decision-making grid… • forces you to consider a number of relevant alternatives. • requires you to identify the criteria used to evaluate the alternatives. • forces you to evaluate each alternative based on the criteria you selected.

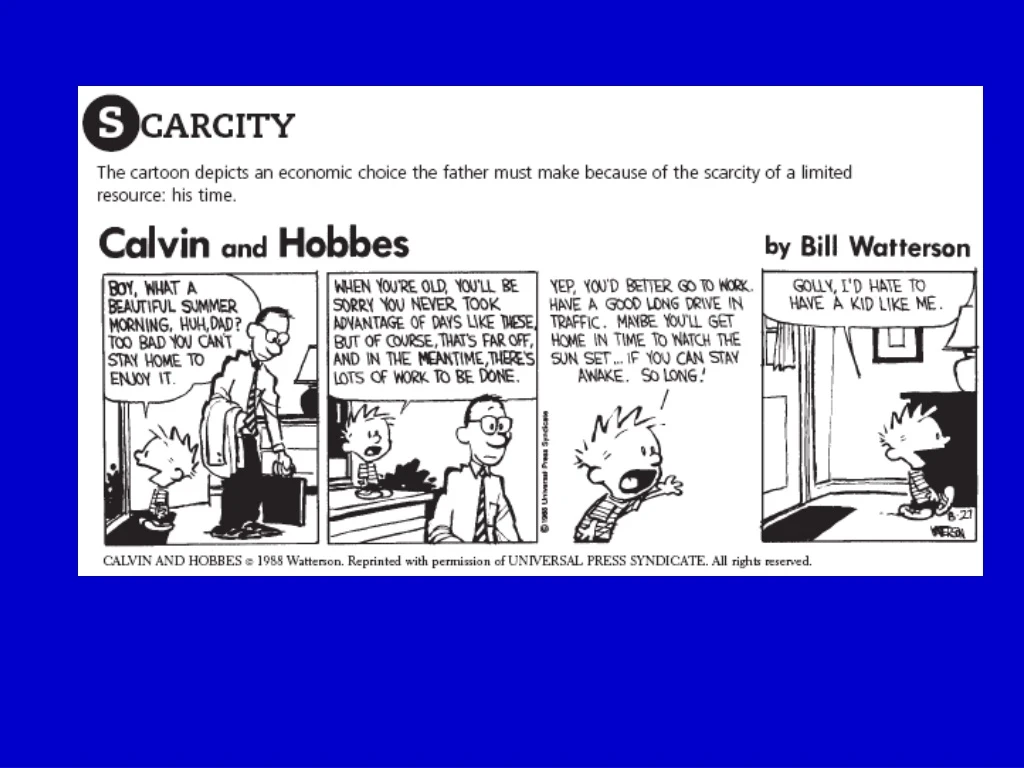

Opportunity Cost • Cost often means more than the price tag placed on a good or service. • opportunity cost–the cost of the next best alternative when one choice is made rather than another. • Even time has an opportunity cost

Production Possibilities Frontier • a diagram showing various combinations of goods or services that can be produced when all resources are fully employed. • Fully employed – all resources are being used

Production Possibilities Frontier • The graph shows all possible combinations • A business can produce anything on or inside the “frontier” • Any point ON the line means resources are fully employed.

Opportunity Cost • Opportunity cost is expressed in terms of things given up to get something else. • not always measured in terms of dollars and cents.

Production Possibilities and Opportunity Cost • You own a Factory • You can only produce 2 goods • Your options are Tennis Bags, Tennis Shoes, or Tennis Hats • Each machine in your factory can produce any of the 3

Production Possibilities and Opportunity Cost • Each Machine can produce the following: • 100 Hats per day • 25 Bags per day • 15 Shoes per day • Your Factory has 10 machines $12 $70 $35

Economic Growth • The production possibilities frontier represents potential output at a given point in time • Over time an economy will grow • This means more goods can be produced

Economic Growth • Economic growth causes the production possibilities frontier to move outward.

Chapter 2 Vocab • Economy • Economics System • Traditional economy • Command economy • Market economy • Social security • Inflation • Fixed income • Capitalism • Profit • Competition • Consumer sovereignty