Download

1 / 111

1.11k likes | 1.24k Views

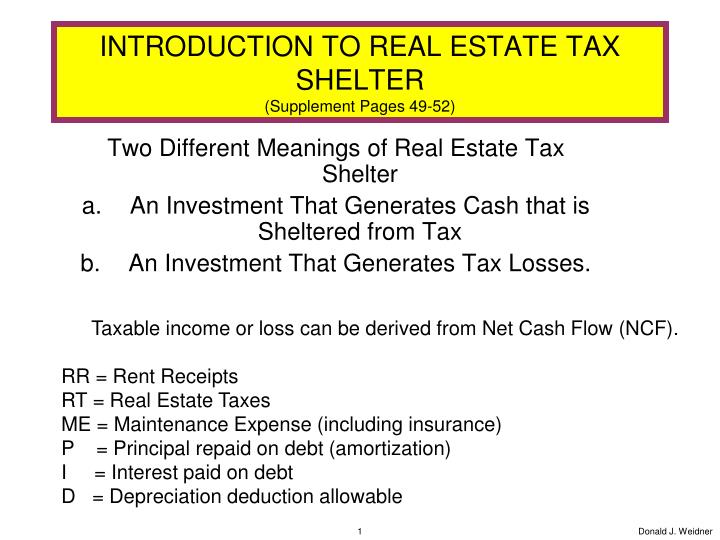

INTRODUCTION TO REAL ESTATE TAX SHELTER (Supplement Pages 49-52). Two Different Meanings of Real Estate Tax Shelter An Investment That Generates Cash that is Sheltered from Tax An Investment That Generates Tax Losses. Taxable income or loss can be derived from Net Cash Flow (NCF).

E N D

INTRODUCTION TO REAL ESTATE TAX SHELTER(Supplement Pages 49-52) Two Different Meanings of Real Estate Tax Shelter An Investment That Generates Cash that is Sheltered from Tax An Investment That Generates Tax Losses. Taxable income or loss can be derived from Net Cash Flow (NCF). RR = Rent Receipts RT = Real Estate Taxes ME = Maintenance Expense (including insurance) P = Principal repaid on debt (amortization) I = Interest paid on debt D = Depreciation deduction allowable Donald J. Weidner

Example of Tax Shelter in Second Sense Example of tax shelter in second sense NCF = RR – RT – ME – (P + I) = $10,000 – 500 – 400 – (900 + 8,000) = $200 Caveat: Capital Expenditures T.I. = NCF + P – D = 200 + 900 – 1,200 = ($100) Collapse of tax shelter T.I. = NCF + P – D = 200 + 8,000 – 700 = $7,500 Donald J. Weidner

MONEY RECEIVED + FMV OF PROPERTY RECEIVED AMOUNT REALIZED AMOUNT REALIZED - ADJUSTED BASIS GAIN INITIAL BASIS (GENERALLY COST) - DEPRECIATION ALLOWABLE + CAPITAL IMPROVEMENTS (ADDITIONAL COST) ADJUSTED BASIS (UNRECOVERED COST) BASIC TAX RULES OF GAIN OR LOSS ON SALE Donald J. Weidner

On Purchase of Land and Building • Allocate cost between land and building. • The investment in the land is an investment in a non-depreciable asset—an asset that does not waste away and therefore has an unlimited useful life. • The building is presumably a wasting asset (through obsolescence or physical deterioration). The investment in the building is depreciable if the building is: (a) used in a trade or business; or (b) held for the production of income. Ex. A $100 total cost of land and building must be allocated, say, $20 to the land and $80 to the building. Only the $80 is depreciable. Donald J. Weidner

On Purchase of Land and Building (cont’d) 3.Determine the “applicable [cost] recovery period” (formerly known as “useful life”) for the asset being depreciated). • Code sec. 168(c) says • 39 years for nonresidential, • 27.5 years for residential rental. Donald J. Weidner

On Purchase of Land and Building (cont’d) 4. Allocate the building cost over the applicable recovery period (39 years for nonresidential). • Code sec. 168(b)(3) says the “straight line” method is the only method that may be used to compute depreciation deductions on either nonresidential property or residential rental property. • The depreciation deduction will be the same every year of the cost recovery period • That is, the deductions may not be “accelerated”—bunched up in the beginning of the cost recovery period. Donald J. Weidner

Nonrecourse Financing and Crane(Text p. 640) • Text discusses “mortgage financing as part of an investor’s depreciable basis in the property—i.e., ‘leveraged depreciation.’” • “The investor’s tax basis in acquired property normally is his cost, which includes not only his investment but any debt incurred to purchase or improve the property.” • “This includes not only funds borrowed by the investor, but any debt to which the property is subject at the time of the acquisition.” • “The Supreme Court has held that basis includes debt on which the investor has no personal liability.” • Citing Crane v. Commissioner, 331 U.S. 1 (1947). Donald J. Weidner

Crane v. Commissioner331 U.S. 1 (1947) (discussed in Text at p. 640 and inMayersonat Supp. p. 52) Ms. Crane sold apartment bldg for (1) $ 2,500 cash “subject to” (2) 255,000 Mortgage (principal) ______ IRS said: $257,500, the sum of the cash plus the principal balance on the mortgage, is the “amount realized” on the sale. Recall: The Code defines “Amount Realized” as “the sum of [1] any money received plus [2] the fair market value of the property (other than money) received.” Donald J. Weidner

Crane (Cont’d) • Ms. Crane conceded “that if she had been personally liable on the mortgage and the purchaser had either paid or assumed it,” the amount so paid or assumed would be a part of her amount realized. • Previous cases had said that an “actual receipt” was not necessary. If the buyer paid or promised to pay the mortgage, the seller was “as real and substantial” a beneficiary as if the money had been paid by buyer to seller and then to the creditor. Donald J. Weidner

LENDER Buyer pays Seller’s $ debt Loan $ Sale BORROWER (SELLER) BUYER AMOUNT REALIZED • No actual receipt is necessary • Buyer discharging the seller’s indebtedness is deemed the equivalent of a payment by buyer to the seller Donald J. Weidner

Crane (Cont’d) • Ms. Crane said it was not the same as if she had been paid the amount of the mortgage balance: (1) she was not personally liable on the mortgage (2) nor did her buyer become personally liable. • She had inherited the property 7 years earlier, when the mortgage encumbering it was already in default. • She entered into an agreement that gave the mortgagee all the net cash flow • Even so, no principal was paid and the interest in arrears doubled. • The transaction was, she said, “by all dictates of common sense, a ruinous disaster.” Note: she had been claiming depreciation deductions. Donald J. Weidner

Crane v. Commissioner (cont’d) Supreme Court in Crane stated what has become known as the “economic benefit” theory: “We are rather concerned with the reality that an owner of property, mortgaged at a figure less than that at which the property will sell, must and will treat the conditions of the mortgage exactly as if they were his personal obligations.” • She will have to pay off the mortgage to access the equity “If he transfers subject to the mortgage, the benefit to him is as real and substantial as if the mortgage were discharged, or as if a personal debt in an equal amount had been assumed by another.” Donald J. Weidner

Crane’s Footnote 37 As a result of the economic benefit theory, Ms. Crane, a seller who was “above water,” was required to include, as part of her “amount realized,” the full amount of the nonrecourse mortgage from which she was “relieved” when she sold the property. Crane’s footnote # 37 reflected the economic benefit theory in a way that gave hope to sellers in a down market--who were “underwater”--that they would not be required to include the amount of their nonrecourse mortgage in “amount realized:” “Obviously, if the value of the property is less than the amount of the mortgage, a mortgagor who is not personally liable cannot realize a benefit equal to the mortgage. Consequently, a different problem might be encountered where a mortgagor abandoned the property or transferred it subject to the mortgage without receiving boot.” Commissioner v. Tufts (text p. 645) put FN. 37 to death. Donald J. Weidner

Crane v. Commissioner (cont’d) • There is one other part of the opinion that got less attention. • Recall that Ms. Crane had been taking depreciation deductions. • Near the end of its opinion, the Court said: • “The crux of this case, really, is whether the law permits her to exclude allowable deductions from consideration in computing gain.” • We’ll return to the proper analysis to apply to mortgage discharge when we consider the Supreme Court’s more recent opinion in Tufts. • First, we consider Mayerson, a major taxpayer victory on the ability to include a nonrecourse mortgage in basis Donald J. Weidner

Mayerson v. Commissioner(Supplement p. 52 and Text p. 654)Nonrecourse Seller Financing • Mayerson made a $10,000 downpayment • Balance paid with a note in the face amount of $322,500 • Note required no repayment of principal until the expiration of 99 years • Did require monthly “interest” payments of $1,500 • Interest at 6% after the principal was reduced below $300,000 • Note was fully non-recourse as to principal • Note was with recourse as to the $1,500 monthly “interest” payments as they accrued • Provided for substantial discounts if retired in the next one ($275,000) [the initial cash asking price] or three ($298,000) years • Buyer’s obligations ended if Buyer reconveyed • In fact, five years later, Mayerson negotiated a reduced purchase price of only $200,000 Donald J. Weidner

MAYERSON:ARGUMENTS OF IRS 1. Mayerson did not acquire a depreciable interest in the building because he made no investment in it (one depreciates one’s “investment” in business property rather than the property itself). The note does not qualify as an investment because a. It puts nothing at risk; and b. It is too contingent an obligation. • Ex ante and Ex post—look at the discounts. The stated principal was not intended to be paid, as confirmed by the ultimate $200,000 taken in satisfaction of the note. The benefit of the depreciation deduction, a deduction given for a non-cash expense on the assumption that there is or may be economic depreciation taking place, should follow the person who bears the risk of economic depreciation. --Mayerson made no investment that would be subject to a risk of depreciation. Donald J. Weidner

Mayerson (IRS Arguments Cont’d) 2. Alternatively, if Mayerson did acquire a depreciable interest in the building, the not is too contingent to be included in his basis. --His basis was merely his $10,000 cash downpayment 3. The economic substance of Mayerson’s investment was merely a lease with an option to purchase. --Under this theory, how did the IRS recharacterize the $10,000 down payment? • As a $10,000 premium paid for a favorable lease • Which Mayerson could “amortize” over 99 years. 4. Other possibility: The $10,000 payment was a fee for orchestrating a tax shelter. Donald J. Weidner

Mayerson: Present Value • What is the present value of the right to receive $322,500 at the end of 100 years? • That depends upon the discount rate • At a 6% rate, compounded monthly, the present value is $811 • What is the present value of the right to receive $1,500 a month for 100 years? • That depends upon the discount rate • At 6% interest, compounded monthly, the present value of that income stream is $299,245 Donald J. Weidner

MAYERSON The Tax Court agreed with 2 propositions: • “It is well accepted that depreciation is not predicated upon ownership of property but rather upon an investment in property,” and that • “the benefit of the depreciation deduction should inure to those who suffer an economic loss caused by wear and exhaustion of the business property.” How could the taxpayer possibly win? Donald J. Weidner

More on Mayerson • The Court said that, under Crane: “the basis of the property was the value at the date of death undiminished by the amount of the mortgage. The inclusion of the indebtedness in basis was balanced by a similar inclusion of the indebtedness in amount realized upon the ultimate sale of the property to a nonassuming grantee.” • That is, it is not so bad to include the debt in basis when the property is acquired because that inclusion in basis will later be “balanced” or “offset” by an equal inclusion in amount realized when the property is sold (if the debt has not been paid off). Donald J. Weidner

More on Mayerson • Because the Code says that the basis for depreciation shall be the same as the basis for computing gain or loss on a sale or exchange, Crane “constitutes strong authority for the proposition that the basis used for depreciation as well as the computation of gain or loss would include the amount of an unassumed mortgage on the property.” Donald J. Weidner

Yet More on Mayerson • Consider the court’s first policy conclusion: • Equate seller financing with third party financing. • “[A] purchase money debt obligation for part of the price will be included in basis. This is necessary in order to equate a purchase money mortgage situation with the situation in which the buyer borrows the full amount of the purchase price from the third party and pays the seller in cash. It is clear that the depreciable basis should be the same in both instances.” • Are these two situations economically the same? Donald J. Weidner

Yet More on Mayerson • Contrary to the court’s statement under point #1, seller-provided nonrecourse financing must be distinguished from third-party nonrecourse financing • Do you see why nonrecourse financing provided by a seller is more subject to abuse than nonrecourse financing provided by a third party? • In the seller-provided purchase money financing, no third party, or anyone, puts up cash in the face amount of the note • Consider Leonard Marcus, T.C.M. 1971-299 (buyer pays more if he can do it with nonrecourse note). • See longstanding Section 108(e)(5) (Supp. p. 64) Donald J. Weidner

Yet More on Mayerson • Section 108(e)(5) treats the reduction in seller-provided financing as a purchase price readjustment • Rather than as discharge of indebtedness income • Provided the reduction does not occur in a bankruptcy reorganization or insolvency case Donald J. Weidner

And Even More on Mayerson • Consider the court’s second policy conclusion: 2.Equate nonrecourse financing with recourse financing: “Taxpayers who are not personally liable for encumbrances on property should be allowed depreciation deductions affording competitive equality with taxpayers who are personally liable for encumbrances or taxpayers who own encumbered property.” • In general, this policy continues with respect to real estate • The “at risk” rules discontinue the policy in other contexts Donald J. Weidner

At Risk • The basic idea behind the “at risk” rules is that a taxpayer should not be able to claim deductions from an investment beyond the amount the taxpayer has “at risk” in that investment. • In general (outside real property), a taxpayer is “at risk” only to the extent the taxpayer has either • cash in an investment, or • a recourse liability in the investment Donald J. Weidner

And Even More on Mayerson • “The effect of [the Mayerson]policy [of including a nonrecourse mortgage in depreciable basis] is to give the taxpayer an advance credit for the amount of the mortgage.” • “This appears to be reasonable since it can be assumed that a capital investment in the amount of the mortgage will eventually occur despite the absence of personal liability.” • Sounds like Crane: As a practical matter, the buyer will treat the debt as if it were recourse. • The doctrine is self-limiting: • This assumption that the mortgage will eventually be repaid can not be made if the amount due on the mortgage exceeds the value of the property. • As it did in the “inflated purchase price” Leonard Marcus (bowling alley) case Donald J. Weidner

Seller-Provided Financing: Purchase Price Reduction • What are the tax consequences to a buyer in a Mayerson situation who satisfies the note to his seller at a lower amount than the amount due? • Section 108(e)(5) • Applies to the debt a purchaser of property owes to the seller • If the note is reduced, it will be treated as a purchase price adjustment • rather than discharge of indebtedness income • provided the purchaser/debtor is solvent. • If the debtor is insolvent, the indebtedness is excluded from the taxpayer’s gross income Donald J. Weidner

Notes following Mayerson • What are the tax consequences to me if my bank allows me to prepay my $100,000 home mortgage for only $80,000? • which it might do if the mortgage is more than the value of the property or is at an interest rate significantly lower than the current rate • The mortgage in Rev. Rul. 82-202 (Supp. p. 64) was nonrecourse(saying the same result for recourse) • Rev. Rul. 82-202 says: • I have $20,000 Discharge of Indebtedness Income • Citing Kirby Lumber (my net worth is increased) • The Section 108(a) exclusion is not available unless I am bankrupt or insolvent. Donald J. Weidner

Tax Relief on Mortgage Discharge in the Wake of The Financial Crisis • In December, 2007, President Bush signed the Mortgage Forgiveness Debt Relief Act of 2007. • It amended section 108(a)(1) to allow an exclusion for a discharge of “qualified principal residence acquisition indebtedness.” • Up to $2 million • Not including home equity indebtedness • Even if the person is not insolvent (even if the person has a positive net worth and it is enhanced by the discharge) • The amount excluded reduces (but not below zero) the basis of the principal residence • The exclusion shall not apply if the discharge “is . . . notdirectly related to a decline in the value of the residence or to the financial condition of the taxpayer.” • Initially retroactive to 1/1/07 and expiring 12/31/09. • Extended in 2008 through 2012 and again through 2013. Donald J. Weidner

Seller-Provided Financing: Not “At Risk”(Supp. P. 92) • Section 465(b)(6)(D)(ii) • “Qualified Nonrecourse Financing” is treated as an amount “at risk.” • It must be from a “qualified person.” • The seller is not a “qualified person.” See Section 49(a)(1)(D)(iv)(II). • However, nonrecourse financing from a third person that is related to the taxpayer can qualify • but only if it is “commercially reasonable and on substantially the same terms as loans involving unrelated persons.” Donald J. Weidner

MONEY RECEIVED + FMV OF PROPERTY RECEIVED AMOUNT REALIZED AMOUNT REALIZED - ADJUSTED BASIS GAIN INITIAL BASIS (GENERALLY COST) - DEPRECIATION ALLOWABLE + COST OF CAPITAL IMPROVEMENTS ADJUSTED BASIS (UNRECOVERED COST) BASIC TAX RULES OF GAIN OR LOSS ON SALE (review prior to Tufts) Donald J. Weidner

Commissioner v. Tufts (1983)(Text p. 645) Builder (Pelt) and his corporation formed a partnership to construct an apartment complex. They contributed nothing. The partnership received a $1,850,000 nonrecourse loan from an S & L—100% nonrecourse financing from a third party lender. Later, 4 friends/relatives were admitted to the partnership. The partners contributed $45,000. In first two years, $440,000 in deductions were taken: $395,000 depreciation; $45,000 other. Partnership’s adjusted basis in the property: $ 1,850,000 Initial Basis (Cost) • 395,000 Depreciation $ 1,455,000 Adjusted Basis Donald J. Weidner

Tufts (cont’d) • Oversimplified somewhat, each partner “sold” the partner’s interest in the partnership for zero cash. • For our purposes, assume that the partnership “sold” the building directly. In effect, this is how the Court treats it. • The Court was incorrect when it said that the Buyer “assumed the nonrecourse mortgage.” • The Buyer only took “subject to” the nonrecourse mortgage. Donald J. Weidner

Tufts (cont’d) • It was stipulated: on the date of the transfer, the Fair Market Value of the property was only $1,400,000 ($450,000 less than the outstanding mortgage balance). • In today’s parlance, the property was $450,000 “underwater” • Hence the facts fell squarely within footnote 37 in Crane: • “Obviously, if the value of the property is less than the amount of the mortgage, a mortgagor who is not personally liable cannot realize a benefit equal to the mortgage.” Donald J. Weidner

Tufts: Taxpayer versus IRS TX argues: Crane footnote 37 limits the Amount Realizedon account of the mortgage to the property’s FMV AR $1,400,000 (Mortgage amount up to FMV) AB -1,455,000 (Cost minus Depreciation) Loss $ (55,000) IRS argues:Crane fn. 37 should be ignored and the entire M should be included in AR AR $ 1,850,000 (Full Mortgage amount) AB 1,455,000 (Cost minus Depreciation) Gain $ 395,000 Donald J. Weidner

TUFTS THEORIES OF TAX TREATMENT ON “RELIEF” FROM THE MORTGAGE THEORIES MENTIONED BY JUSTICE BLACKMUN • Economic Benefit • Cancellation of Indebtedness • Co-Investment • Tax Benefit • Double Deduction • Bifurcated Transaction • Balancing Entry Donald J. Weidner

Economic Benefit • “Crane ultimately does not rest on its limited theory of economic benefit.” • Crane said she was a “real and substantial [economic] beneficiary” of the mortgage discharge because it enabled her to receive her equity in the property • In Crane, there was no economic loss that should have been reflected in a tax loss • Nor did Tufts involve an economic loss that should have been reflected in a tax loss • Crane “approved the Commissioner’s decision to treat a nonrecourse mortgage in this context as a true loan.” Donald J. Weidner

Cancellation of Indebtedness Assets = Liabilities $ 100 (cash) $80 + Equity $20 Consider the balance sheet after you exercise an opportunity to satisfy the $80 liability with a $65 cash payment: Assets = Liabilities $ 35 (cash) $ 0 + Equity $35 Cancellation of indebtedness income theory has traditionally focused on the taxpayer’s increase in net worth, or equity, as the enhancement in wealth (income) ($15 in this example). Blackmun stated: “the doctrine relies on a freeing of assets theory to attribute ordinary income to the debtor upon cancellation.” He also stated: Crane’s economic benefit theory “also relies on a freeing of assets theory.” Donald J. Weidner

Coinvestment Theory • Basic concept: the nonrecourse lender is a co-investor with the borrower Court says Crane stands for the proposition that the lender gets no basis (made no investment). See fn. 5: “The [IRS] might have adopted the theory . . . that a nonrecourse mortgage is not true debt, but, instead, is a form of joint investment by the mortgagor and the mortgagee. On this approach, nonrecourse debt would be considered a contingent liability, under which the mortgagor’s payments on the debt gradually increase his interest in the property while decreasing that of the mortgagee. Because the taxpayer’s investment in the property would not include the nonrecourse debt, the taxpayer would not be permitted to include that debt in basis.” • Court (and the IRS) rejects the coinvestment theory. Donald J. Weidner

Tax Benefit A tax benefit approach might focus on the $395,000 depreciation deductions that were taken by a taxpayer who suffered no economic depreciation. • That is, there is a need to offset an earlier deduction that was permitted because of an economic assumption that was subsequently proven to have been incorrect • Analogy: if I deduct a payment as a business expense this year, and get a refund of that payment next year, I must correct the error. • Conversely, if I report a retainer as income this year and have to refund it next year, I get to correct the earlier inclusion in income. Tufts rejected a tax benefit approach: “Our analysis applies even in the situation in which no deductions are taken.” Donald J. Weidner

Tax Benefit (cont’d) • See footnote 8: “Our analysis . . . focuses on the obligation to repay and its subsequent extinguishment, not on the taking and recovery of deductions.” • Question: Is not an exclusion a tax benefit that is similar to a deduction? • That is, if you are not focusing on the tax benefit of the depreciation deduction, are you focusing on the prior untaxed receipt of the purchase money loan proceeds (which is not included because of its accompanying obligation to repay)? Donald J. Weidner

Double Deduction • The 3d Circuit had said that a contrary holding to Tufts would result in a “double deduction.” Note that the taxpayer here litigated taking the position that the $395,000 depreciation deduction should be followed by a $55,000 loss on sale • despite an economic break-even result • [setting aside the $45,000 contributed and previously deducted]. Donald J. Weidner

Double Deduction (cont’d) • The Supreme Court said its analysis applies even if no deductions are taken. • “Unless the outstanding amount of the mortgage is deemed to be realized, the mortgagor effectively [1] will have received untaxed income at the time the loan was extendedand [2]will have received an unwarranted increase in the basis of the property.” • This reflects a new emphasis on the prior untaxed receipt. • And on the untaxed receipt’s prior inclusion in basis. Donald J. Weidner

Professor Barnett’s Bifurcated Transaction I. Liability Transaction AR $ 1,850,000 (cash received for a note--the promise to repay) • AB 1,400,000 (FMV of property the borrower transferred to satisfy the liability) Liability Gain $ 450,000 II. Asset Transaction AR $1,400,000 (“Relief” from a N/R loan, which was worth no more than the property pledged to secure it) • AB 1,455,000 (Cost – Depreciation = AB) Asset Loss $ (55,000) Donald J. Weidner

Bifurcated Transaction (cont’d) • In the normal purchase and sale of property, the buyer knows the buyer’s basis (cost) at the purchase, at the outset. • The buyer only knows the buyer’s amount realized when the buyer ultimately sells the property • In a liability transaction, the FIRST thing you know is the amount realized (the amount you get for your note) • The maker doesn’t know the cost of the note until the maker pays it off Donald J. Weidner

Bifurcated Transaction (cont’d) • Barnett’s conception of the Amount Realized on the asset side of the transaction: • The Amount Realized on the transfer of the property was $1.4 million because the only consideration the seller received on the transfer was the cancellation of its nonrecourse liability worth only $1.4 million [the value of the property that secured its payment] • Remember, the only remedy on the nonrecourse note is a foreclosure on the property mortgaged to secure it • With no deficiency judgment possible • As Justice O’Connor put it: “The benefit received by the taxpayer in return for the property is worth no more than the fair market value of the property, for that is all the mortgagee can expect to collect for the [nonrecourse] mortgage.” Donald J. Weidner

Bifurcated Transaction (cont’d) • Justice O’Connor: “I see no reason to treat the purchase, ownership, and eventual disposition of property differently because the taxpayer also takes out a mortgage, an independent transaction.” • Further: “There is no economic difference between the events in this case and a case in which [1] the buyer buys property with cash; [2] later obtains a nonrecourse loan by pledging the property as security; [3] still later, using cash on hand, buys off the mortgage for the market value of the devalued property; and [4] finally sells the property to a third party for its fair market value.” • But, the law treats the two situations differently Donald J. Weidner

Professor Bittker’s Balancing Entry versus Professor Barnett’s Bifurcated Transaction • Bittker’s result is the same result urged by the IRS: The unamortized amount of the mortgage is included in Amount Realized • resulting in a gain of $ 395,000 • An amount equal to the amount of depreciation taken • Barnett’s results total Bittker’s $395,000 (sum of $450,000 liability gain and the $55,000 asset loss) • Barnett says they should not be totaled—they are of a different character • Bittker says his approach is independent of the depreciation deduction. • The Court says the same thing about its approach. Donald J. Weidner

BALANCING ENTRY: BITTKER’S NO DEPRECIATION EXAMPLE 1) Taxpayer buys Blackacre for $100,000, paying: $ 25,000 cash down payment + 75,000 Nonrecourse purchase money N/M to Seller $100,000 total cost to Taxpayer 2) Blackacre skyrockets in value to $300,000. • Taxpayer refinances, increasing the N/M by $175,000 (from $75,000 to $250,000) [pulling $175,000 cash out]. 4) FMV drops to $40,000. 5) Taxpayer gives a deed in lieu of foreclosure. Donald J. Weidner