Audit of the Sales and Collection Cycle

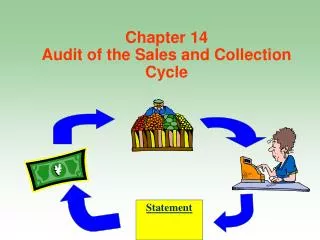

Audit of the Sales and Collection Cycle Chapter 13 Accounts in the Sales and Collection Cycle Sales Cash sales Sales on account Cash in Bank Cash Discounts Taken Accounts Receivable Beginning Cash receipts balance Sales returns Sales on and allowances account

Audit of the Sales and Collection Cycle

E N D

Presentation Transcript

Audit of the Sales andCollection Cycle Chapter 13

Accounts in the Salesand Collection Cycle Sales Cash sales Sales on account Cash in Bank Cash Discounts Taken Accounts Receivable Beginning Cash receipts balance Sales returns Sales on and allowances account Charge-off of Ending uncollectible balance accounts Sales Returns and Allowances Bad Debt Expense

Accounts in the Salesand Collection Cycle Accounts Receivable Beginning Cash receipts balance Sales returns Sales on and allowances account Charge-off of Ending uncollectible balance accounts Allowance for Uncollectible Accounts Charge-off of Beginning uncollectible balance accounts Estimate of bad debt expense Ending balance Bad Debt Expense

Sales Transaction Accounts Sales Accounts receivable Business Functions Processing customer orders, Granting credit, Shipping goods, Billing customers and recording sales Documents and Records Sales invoice, Sales journal or listing, Sales transaction file, Accounts receivable master file and trial balance, Monthly statements

Cash Receipts Transaction Accounts Cash in bank (debits from cash receipts) Accounts receivable Business Functions Processing and recording cash receipts Documents and Records Remittance advice, Prelisting of cash receipts, Cash receipts transaction file, Cash receipts journal or listing

Sales Returns and Allowances Transaction Accounts Sales returns and allowances Accounts receivable Business Functions Processing and recording sales returns and allowances Documents and Records Credit memo Sales returns and allowances journal

Charge-off of Uncollectible Accounts Transaction Accounts Accounts receivable Allowance for uncollectible accounts Business Functions Charging off uncollectible accounts receivable Documents and Records Uncollectible account authorization form General journal

Bad Debt ExpenseTransaction Accounts Bad debt expense Allowance for uncollectible accounts Business Functions Providing for bad debts Documents and Records General journal

Effect of E-Commerce on the Sales and Collection Cycle Business-to-business (B2B) Business-to-consumer (B2C) Management’s assertions for sales and collection activities remain the same.

Effect of E-Commerce on the Sales and Collection Cycle Auditors should obtain an understanding of the design and operation of key internal controls over e-commerce revenues. Evidence for e-commerce activities is likely to be in electronic form.

Methodology for Designing Controlsand Substantive Tests: Sales Design tests of controls and substantive tests of transactions for sales to meet transaction- related audit objectives. Understand internal control – sales Assess planned control risk – sales Audit procedures Sample size Evaluate cost-benefit of testing controls. Items to select Timing

Transaction-Related AuditObjectives for Sales Existence: Recorded sales are for shipments actually made. Completeness: Existing sales transactions are recorded. Accuracy: Recorded sales are for the amount shipped.

Design Substantive Testsof Transactions for Sales Classification: Sales transactions are properly classified. Timing: Sales are recorded on the correct dates. Posting and summarization: Sales transactions are properly included in the accounts receivable master file.

Direction of Tests for Sales Customer order Shipping document Duplicate sales invoice Completeness Start Sales journal General ledger Accounts receivable master file = Existence Start

Major Audit Objectives in the Sales/Collection Cycle Sales Transactions/Balance = Existence Cash Receipts Transactions = Completeness Sales Returns & Allowances = Existence Write off of Bad Debts = Existence Recording Bad Debt Expense = Existence

Role of all Audit Tests in the Sales and Collection Cycle Sales Accounts Receivable Cash in Bank Sales transactions Cash receipts transactions Audited by TOC,STOT, and AP Audited by TOC, STOT, and AP Ending balance Ending balance Audited by AP and TDB TOC+STOT+AP+TDB = Sufficient competent evidence per GAAS