Download

1 / 28

290 likes | 436 Views

Chapter 3 Accounting Equation and Illustration. Main Points: 1. Assets 2. Liabilities 3. Owner’s Equity 4. Illustrative Transactions Time Allocated: 4 Periods. Learning Objectives. The students are required to --

E N D

Chapter 3Accounting Equation and Illustration Main Points: 1.Assets 2. Liabilities 3. Owner’s Equity 4. Illustrative Transactions Time Allocated: 4 Periods

LearningObjectives The students are required to -- • understand the three elements of the accounting equation: assets, liabilities, and owner’s equity. • understand and grasp the accounting equation. • know how to illustrate transactions. • grasp some important words, phrases, and definitions. Time Allocated: 4 Periods

What? Warm-up 1. What is a sole proprietorship? 2. What is a partnership? 3. What is a corporation? 4. What are the two types of partnerships? 5. Why should all partnerships be based on a written partnership agreement? 6. Compared with the sole proprietorship and partnership, what advantages and disadvantages does a corporation have?

Warm-up (1) 1. What is a sole proprietorship? -- A business owned by one person. 2. What is a partnership? -- A special form of business that joins two or more individuals together as co-owners. 3. What is a corporation? -- a big company, or a group of companies acting as a single organization; a unique entity created by law.

Warm-up (2) 4. What are the two types of partnerships? -- General partnership and limited partnership. 5. Why should all partnerships be based on a written partnership agreement? -- Because the lack of it can result in the internal conflicts between partners when a disagreement arises.

Warm-up (3) 6. Compared with the sole proprietorship and partnership, what advantages and disadvantages does a corporation have? A) Advantages: 1) continuous existence; 2) ease of transferring ownership; 3) less risk of unrecognized equity liquidation;

Warm-up (4) 4) separate legal entity; 5) limited liability of stockholders; 6) ease of raising capital; 7) lack of mutual agency; 8) centralized authority and responsibility; 9) professional management.

Warm-up (5) B) Disadvantages: 1) more time and money needed for incorporation; 2) negative influence of the requisition of personal guarantees on the limitation of liability; 3) obstruction in decision making caused by conflicts and disagreements among stockholders;

Warm-up (6) 4) difficulty in recovering the value of the investment for minority stockholders; 5) more paperwork to prepare; 6) twice- taxed income.

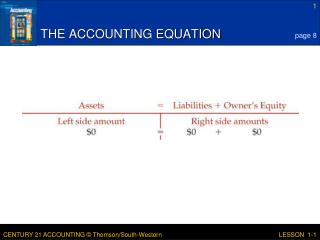

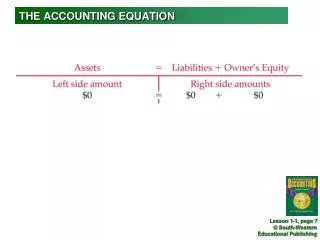

Presentation (1) A business is like a box. In this box, there are many kinds of contents and the claim on these contents. These contents and the claim on these contents should be equal and belong to somebody (owners or creditors). We can use economic resources to describe these contents. Another term for claim is equities. Thus, a company can be viewed as economic resources and equities: Economic Resources = Equities.

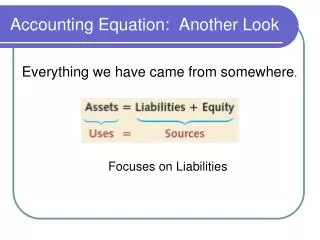

Presentation (2) For each company, some of the economic resources are gained from owners and the other parts are borrowed from creditors. Thus, the equities of economic resources are classified into two types: owner’s equity and creditor’s equity. Thus: Economic Resources = Creditor’s Equities + Owner’s Equities. In accounting, the term for economic resources is assets and creditor’s equity is liabilities, the equation is described as follows: Assets = Liabilities + Owner’s Equity.

What? In-class Activities (1) Reading and Questions (Page 17- 18): 1. Define assets, liabilities, and owner’s equity. 2. Give some examples for assets. 3. Give some examples for current liabilities and long-term liabilities. 4. Why is owner’s equity sometimes considered to equal net assets? 5. What will increase owner’s equity and decrease owner’s equity?

In-class Activities (1-1) Answers: 1. Define assets, liabilities, and owner’s equity. 1) Assets: the economic resources owned or controlled by a business that can benefit future operations for the business. 2) Liabilities: those debts arising from the past transactions and be paid by providing goods or services in the future. 3) Owner’s Equity: the claims by the owner on the net assets of the business.

In-class Activities (1-2) 2. Give some examples for assets. -- cash, inventory, notes receivable, accounts receivable, prepaid expenses, land, buildings, and equipment and so on. 3. Give some examples for current liabilities and long-term liabilities. 1) current liabilities: notes payable, accounts payable; 2) long-term liabilities: bonds payable, mortgages payable.

In-class Activities (1-3) 4. Why is owner’s equity sometimes considered to equal net assets? -- Because it equals the assets after deducting the liabilities. 5. What will increase owner’s equity and decrease owner’s equity? -- Owner’s investment increase owner’s equity and owner’s withdrawal decreases owner’s equity. In accounting, revenues earned increase owner’s equity and expenses incurred decreases owner’s equity.

In-class Activities (2) Illustrative Transactions (Page 19-21): Let us use accounting equation to analyze the effects of some typical transactions. Suppose George Rose opens a photocopy company called George Rose Photocopy Company on March 1. During March, his business engages in the transactions described in the following paragraphs.

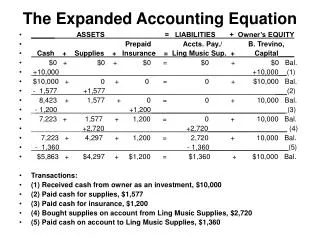

In-class Activities (2-1) 1. Owner’s Investment George takes $10,000 out of his own personal account to open his company. The transfer of cash from personal account to business account is called investment. The investment increases assets (Cash) and owner’s equity (George Ross, Capital). Assets = Liabilities + Owner’s Equity $10,000 $10,000

In-class Activities (2-2) 2. Purchasing Assets with Cash The company purchases paper and stationary for $800 and a computer for $4,000. This transaction doesn’t change the total assets, liabilities, and owner’s equity of the agency, but it changes the composition of the assets (decreasing cash and increasing office supplies and office equipment). Assets = Liabilities + Owner’s Equity $10,000$10,000 +800 (Office Supplies) +4,000 (Office Equipment) - 4,800 (Cash) Bal. $10,000 $10,000

In-class Activities (2-3) 3. Purchasing Assets by Incurring a Liability It is not necessary to buy assets always with cash. You may also purchase assets on credit, on the basis of the promise to pay the money at the fixed future time. Suppose George buys photocopy equipment on credit for $1,500. This transaction increases the assets – equipment and increases the liabilities of this agency (Accounts Payable). Assets = Liabilities + Owner’s Equity $10,000$10,000 +1,500 (Photocopy Equipment) + 1,500 (Accounts Payable) Bal. 11,500 1,500 10,000

In-class Activities (2-4) 4. Paying a Liability If George later pays $1,500 owed for the equipment, both assets (Cash) and liabilities (Accounts Payable) will decrease, but equipment will be unaffected. The accounting equation is still in balance after this transaction. Assets = Liabilities + Owner’s Equity $11,500 $1,500 $10,000 -1,500 (Cash) - 1,500 (Accounts Payable) Bal. 10,000 10,000

In-class Activities (2-5) 5. Earning Revenues (1) George Ross Company earns revenues by providing printing services to customers. Sometimes these revenues are paid to the company immediately in the form of cash, and sometimes the client agrees to pay later. Suppose that the business performs a service by printing brochures for a garment dealer and collects a fee of $3,000. After this transaction, the assets and owner’s equity of George Ross Photocopy both increases. Assets = Liabilities + Owner’s Equity $10,000 $10,000 +3,000 (Cash) + 3,000 (Photocopy Fees Earned) Bal. 13,000 13,000

In-class Activities (2-6) 6. Earning Revenues (2) Now assume that George provides a big service calling for a fee of $2,500 and George agrees to wait for the payment. Since the fee is earned now, a bill or invoice is sent to the client and the transaction is recorded now. This transaction increases both assets (Accounts Receivable) and owner’s equity. Although money isn’t collected now, the revenue has been earned. Assets = Liabilities + Owner’s Equity $13,000 $13,000 +2,500 (Accounts Receivable) + 2,500 (Photocopy Fees Earned) Bal. 15,500 15,500

In-class Activities (2-7) 7. Collecting Accounts Receivable If it is assumed that a month later George receives $2,500 from the client in transaction 6, the asset Cash is increased and the asset Accounts Receivable is decreased. Assets = Liabilities + Owner’s Equity $15,500 $15,500 +2,500 (Cash) - 2,500 (Accounts Receivable) Bal. 15,500 15,500

In-class Activities (2-8) 8. Paying Expenses Just as revenues are recorded when they are earned, expenses are recorded when they are incurred. Expenses may be paid in cash when they occur; or if the payment is to be made later, a liability such as Accounts Payable or Wages Payable is increased. In both cases, owner’s equity is decreased. Suppose that the agency paid $600 to a secretary for the first two weeks’ wages. This transaction decreases assets (Cash) and owner’s equity. Assets = Liabilities + Owner’s Equity $15,500 $15,500 -600 (Cash) - 600 (Office Wages Expense) Bal. 14,900 14,900

In-class Activities (2-9) 9. Withdrawing Money from Business George withdraws $800 from business account to pay for personal living expenses. This transaction decreases the assets (Cash) and owner’s equity of the company. Withdrawals have the same effect as the expenses but withdrawals are not considered as expenses. Assets = Liabilities + Owner’s Equity $14,900 $14,900 -800 (Cash) - 800 (Withdrawals) Bal. 14,100 14,100

Further Practice 1. Exercise One at Page 22. Use the accounting equation to answer the following questions. 2. Exercise Two at Page 22. In the columns, indicate whether each transaction caused an increase (+), a decrease (-), or no change (NC) in assets, liabilities, and owner’s equity.

Further Practice 3. Exercise Three at Page 23. Use the accounting equation to analyze these transactions and record them on a piece of paper similar to the examples in the text.

Homework 1. Revise Chapter 3 to get further understanding. 2. Finish the exercises in this chapter and discuss Exercise Four at Page 23 the following questions with your partners. 1) Define assets, liabilities, and owner’s equity. 2) Describe the accounting equation. 3. Preview Chapter 3.