Two Liquidation Modes

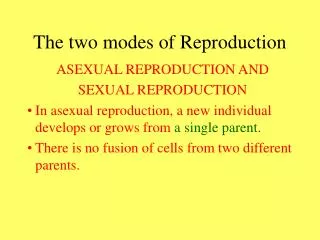

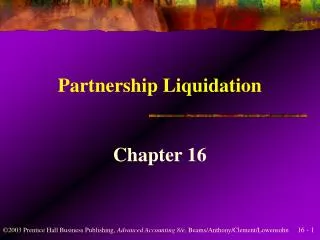

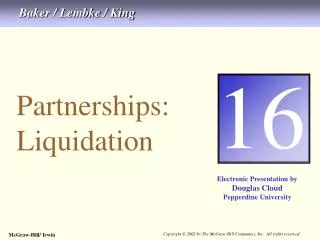

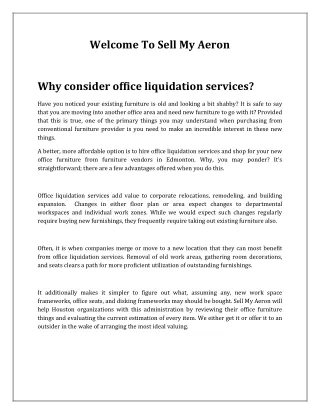

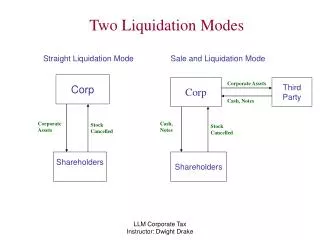

Two Liquidation Modes. Straight Liquidation Mode. Sale and Liquidation Mode. Corp. Corp. Third Party. Corporate Assets. Cash, Notes. Corporate Assets. Cash, Notes. Stock Cancelled. Stock Cancelled. Shareholders. Shareholders. Complete Liquidation – Shareholder Impact.

Two Liquidation Modes

E N D

Presentation Transcript

Two Liquidation Modes Straight Liquidation Mode Sale and Liquidation Mode Corp Corp Third Party Corporate Assets Cash, Notes Corporate Assets Cash, Notes Stock Cancelled Stock Cancelled Shareholders Shareholders LLM Corporate Tax Instructor: Dwight Drake

Complete Liquidation – Shareholder Impact General Rule: Per 331, complete liquidation treated as sale or exchange of stock, producing capital gain or loss equal to difference between cash and FMV of property received and shareholder’s basis in stock. Section 301 not apply. Timing Issues: - When did liquidation began and dividends (non-liquidating) distributions end. Fact question. Look to corporate resolutions and adoption of plan. - 453 installment sales treatment applies when liquidating distributions over time. Open transaction treatment very risky; appears trumped by 453. - 453 installment treatment permitted even as to installment obligations acquired by non-public corp in asset sell-off and distributed to shareholders. To qualify under 453, corp sale that created obligation must be within 12 month period after liquidation plan adopted and liquidation must be completed within same period. Inventory and “dealer” property qualify allowed only if part of bulk sale of assets. LLM Corporate Tax Instructor: Dwight Drake

Complete Liquidation – Corporation Impact General Rule: Per 336, Corp recognizes gain or loss on property distributed or sold as part of complete liquidation. 267 related-party loss limitations not apply in complete liquidation. (d)(1) Related Party Exception: No loss at all on distribution to related party (per 267) in complete liquidation if: - Distribution not pro rata, or - Distributed property acquired by corp in 351 transaction or as contribution to capital within 5 yrs of distribution (“Disqualified Property”). (d)(2) Tax Avoidance Exception: No built-in loss (loss at time of acquisition) allowed if property acquired in 351 transaction or contribution to capital and principal purpose was to recognize loss on liquidation. If acquired within 2 yrs of plan of liquidation, bad purpose a done deal unless there is “clear and substantial relationship” between property and conduct of business and solid explanation. If outside 2yr window, probably safe except in “most rare” cases. LLM Corporate Tax Instructor: Dwight Drake

Problem 336 Basic Facts: A owns 100 shares of H Corp, cost 10k. H Corp E&P – 12k. H Corp liquidates. A gets 20k cash in liquidation. A has LTCG of 10k per 331(a). A gets 10k yr 1 and 10k yr 2. Under 453, A recognizes 5k LTCG in year 1 and 5k LTCG in year 2. Service allows open reporting if amount uncertain; if so, no gain until basis recovered. Can elect to opt out of 453; then full 10k LTCG in year 1. If no plan a liquidation in year 1, may be issue of whether both distributions are part of liquidation (fact issue). If not, then year 1 distribution 10k ordinary income dividend under 301; yr 2 liquidating distribution and no gain. LLM Corporate Tax Instructor: Dwight Drake

Problem 336 Basic Facts: A owns 100 shares of h Corp, cost 10k. H Corp E&P – 12k. H Corp liquidates. A gets in liquidation 8k cash and 12k note, payable 1k per yr for 12 yrs. H obtained note on sale of capital asset as part of liquidation. A realizes 10k LTCG on sale. Per 453(h), installment reporting available on note if obtained by corp within 12 month period after adoption of plan of liquidation and liquidation completed in 12 months after plan. Gross profit percentage is 50%. Hence, 4k LTCG yr 1 on receipt of 8k and .5k in each following year on receipt of 1k. If H stock publicly traded, 453(k)(2)(A) precludes use of 453. 10k LTCG. Same as (c), but installment obligation received by H two yrs ago and no payments made. No hope for installment reporting because obtained before plan of liquidation. 10K LTCG in year 1 and basis in note 12k. After liquidation, A pays 5k judgment against old H. Per Arrowsmith case, this 5k LTCL to A even though would have been deductible to H Corp. Character of loss determined with reference to LTCG reported by A. LLM Corporate Tax Instructor: Dwight Drake

Problem 349 Basic Facts: X Corp stock owned by I (60) shares and F (40 shares). No liabilities and following assets. On 1/1, adopts plan of liquidation. Basis FMV Gainacre 100k 400k Lossacre 800k 400k Cash 200k 200k All assets distributed to I and F 60-40 pro-rata as tenants-in-common. X Corp has 300k gain on Gainacre and 400k loss on Lossacre. Shareholders take basis equal to FMV per 334(a). 336(d) loss limitation not apply because distribution pro rata and assets held over 5 yrs. I gets Lossacre and cash; F gets Gainacre. X has 300k gain on Gainacre. Loss on Loassacre not allowed per 336(d)(1) because I is related person per 267 (more than 50%) and distribution not pro rata. I’s basis in Lossacre still 400k; loss in permanently gone. LLM Corporate Tax Instructor: Dwight Drake

Problem 349 Basic Facts: X Corp stock owned by I (60) shares and F (40 shares). No liabilities and following assets. On 1/1, adopts plan of liquidation. Basis FMV Gainacre 100k 400k Lossacre 800k 400k Cash 200k 200k X distributes Gainacre and 200k to I and Lossacre to F. X recognizes 300k on Gainacre and 400k loss on Lossacre. Although not pro rata, F not related person under 267 because not over 50% owner. Thus, 336(d) limit not apply. (d) Same pro rata as (a), but X acquired Lossacre 4 yrs ago as contribution to capital. Still 300k gain on Gainacre. 60% portion to Lossacre loss (240k) not allowed per 336(d) because go to I and “disqualified property” because acquired within 5 yrs in 351 transaction. Loss on portion to F (160k) allowed. I and F still take basis equal to FMV . Same result if Lossacre has 1 mill FMV and 800k basis on contribution to capital. For 336(d)(1) purposes, built-in gain or loss not applicable. LLM Corporate Tax Instructor: Dwight Drake

Problem 349 Basic Facts: X Corp stock owned by I (60) shares and F (40 shares). No liabilities and following assets. On 1/1, adopts plan of liquidation. Basis FMV Gainacre 100k 400k Lossacre 800k 400k Cash 200k 200k Gainacre and cash to I; Lossacre to F; Lossacre have no relationship to X business and acquired by 351 transfer from I and F 18 months prior to plan of liquidation when FMV 700k and basis 800k. 336(b)(1) disallowance not apply because F not 267 related party. But 336(b)(2) anti-stuffing rule might apply because 351 transaction within 2 yrs of plan. If 362(e)(2) basis adjustment made at contribution, no need for 336(b)(2) anti-stuffing – loss never realized. If no 336(e)(2) adjustment, then 100k pre-contribution loss disallowed per 336(b)(2), but 300k post-contribution loss allowed. No hope of rebutting 2 yr taint presumption because asset not related to X business. LLM Corporate Tax Instructor: Dwight Drake

Problem 349 Basic Facts: X Corp stock owned by I (60) shares and F (40 shares). No liabilities and following assets. On 1/1, adopts plan of liquidation. Basis FMV Gainacre 100k 400k Lossacre 800k 400k Cash 200k 200k I and F own X Corp 80-20. I contributed Gainacre and Lossacre; F contributed cash in 351 deal. Lossacre is 336(d)(1) “disqualified property”, 362(e)(2) applied at contribution, 336(d)(2) not apply because no “plan” for X to recognize loss on liquidation. X distributes each asset pro-rata to parties in liquidation. - 362(e)(2) basis reduction is 100k (900k less 800k) based on I’s contibution of assets. - Of remaining 300k built-in loss on Lossacre, 80% (240k) disallowed because I related party. Remaining 20% (60k) allowed as loss to X. LLM Corporate Tax Instructor: Dwight Drake

Problem 349 Basic Facts: X Corp stock owned by I (60) shares and F (40 shares). No liabilities and following assets. On 1/1, adopts plan of liquidation. Basis FMV Gainacre 100k 400k Lossacre 800k 400k Cash 200k 200k (g) Same as (f), but there was plan to have X recognize built-in loss. Then entire built-in loss disallowed per 336(d)(2). Fact that portion of Lossacre went to F (20% shareholder) irrelevant. LLM Corporate Tax Instructor: Dwight Drake

Subsidiary Liquidation Impacts of qualifying as 332 subsidiary liquidation: - No gain or loss recognized by parent corp per 332. - Parent corp takes transferred basis in Sub’s assets per 334(b)(1). - Parent corp inherits Sub’s E&P and other tax attributes (pro rata) per 381(a)(1). - No gain or loss to Sub corp per 337, which overrides 1245, to extent distributions to “80-percent distributee”. - No relief to minority shareholders: liquidation gain recognized and basis FMV. - Loss assets to satisfy Parent corp debt not trigger loss per 337(b)(1). - No 337 relief if tax exempt owns stock. 337(b)(2). LLM Corporate Tax Instructor: Dwight Drake

Qualification Under 332 Requirements: Plan of complete liquidation adopted. 80% of total of Sub voting stock owned by corporate parent from adoption of plan until liquidation. 80% of total value of Sub stock owned by corporate parent from adoption of plan until liquidation. Timing either: - One-shot liquidation within one taxable year. - Plan provides competed within 3 years after year of first distribution. LLM Corporate Tax Instructor: Dwight Drake

Problem 361-1 Basic Facts: P Inc. (“P”) owns 90% X Corp stock; I owns 10%. P basis 3k; I basis .2k. X E&P 2k. Following X assets: Basis FMV Land 3,000 8,000 Equip 2,500 1,000 Inventory 100 1,000 Liquidation scenarios: Inventory to I; other assets to P. - 332 requirements all met: Both 80% tests; one-shot liquidation that meets timing requirements of 332(b)(2). - P recognizes none of 6k (9k less 3k basis) gain recognized. - I (10% individual) recognizes 800 gain (1k less 200 basis) - I basis in inventory 1k. LLM Corporate Tax Instructor: Dwight Drake

Problem 361-1 Basic Facts: P Inc. (“P”) owns 90% X Corp stock; I owns 10%. P basis 3k; I basis .2k. X E&P 2k. Following X assets: Basis FMV Land 3,000 8,000 Equip 2,500 1,000 Inventory 100 1,000 Liquidation scenarios: Inventory to I; other assets to P (Continued). - P basis in land 3k, equip 2.5k – both carryover per 334(b)(1). P stock basis disappears. - X has 900 gain on inventory. No gain or loss on other assets because P “80-percent” distributee” per 337(c). - P picks up X’s tax attributes per 381 and 90% E&P. X E&P is 2k plus .9k on inventory distribution for 2.9k total. Thus P’s E&P goes up 2.61k (90%). LLM Corporate Tax Instructor: Dwight Drake

Problem 361-1 Basic Facts: P Inc. (“P”) owns 90% X Corp stock; I owns 10%. P basis 3k; I basis .2k. X E&P 2k. Following X assets: Basis FMV Land 3,000 8,000 Equip 2,500 1,000 Inventory 100 1,000 Liquidation scenarios: Equipment to I; other assets to P. Same result as in (a) except no inventory gain to X, and E&P carryover gain to P is 1.8k (90% of 2k). No loss recognition to X on 332 liquidation per 336(d)(3). Improve by transferring loss equipment to P or selling loss equipment. If 336(d)(2) not apply to sale, 1.5k loss recognized by X and transferred E&P reduced to 450 (90% of 500). Smart to sell loss asset if possible. Note, I basis in equipment 1k (step-down basis loss). LLM Corporate Tax Instructor: Dwight Drake

Problem 361-1 Basic Facts: P Inc. (“P”) owns 90% X Corp stock; I owns 10%. P basis 3k; I basis .2k. X E&P 2k. Following X assets: Basis FMV Land 3,000 8,000 Equip 2,500 1,000 Inventory 100 1,000 Liquidation scenarios: Same as (b), but P basis in S stock 30k and X basis in land 30k. P recognizes no loss; X recognizes no loss. Land 30k basis carries over to P per 334(b)(1). I still has step down 1k basis in equipment and 800 gain. E&P carryover to P still 1.8k. If flunk 332, P gets loss on stock. X still won’t get loss because of 336(d)(1)(A) (P owns over 50%). Two ways to flunk. P sells off over 20% stock per Day & Zimmerman case. Or X stretches liquidation over 3 yr. period. Also, X could sell loss asset and recognize loss (smartest). LLM Corporate Tax Instructor: Dwight Drake

Problem 361-2 Basic Facts: C Corp 100 shares out. M Corp owns 75 shares (basis 1k); U owns 25 shares (basis 3k). C has no E&P; 10k NOL; following assets: Basis FMV Cash 2,000 2,000 Note 1,000 4,000 Land 100 1,000 Equip 100 1,000 Total 3,200 8,000 (a) C liquidates; 2k cash to U; rest to M. No 332 because no 80%. M has 5k gain (6k less basis of 1k). U has 1k loss (2k less 3k basis). C has 3k gain on note, .9k gain on equip, and .9k gain on land, all offset by NOL carryover. No carryover attributes to M. M and U have basis equal to FMV of assets received per 334(a). LLM Corporate Tax Instructor: Dwight Drake

Problem 361-2 Basic Facts: C Corp 100 shares out. M Corp owns 75 shares (basis 1k); U owns 25 shares (basis 3k). C has no E&P; 10k NOL; following assets: Basis FMV • Cash 2,000 2,000 • Note 1,000 4,000 • Land 100 1,000 • Equip 100 1,000 • Total 3,200 8,000 • 2k to redeem U stock. Complete liquidation of C one week later. If 332 apply, M have no gain, C has no gain, no gain on installment note per 453B(d), no 1245 gain to C per 1245(b)(3), no land gain and full 10k NOL carries over to M. No E&P to carry over. • Will 332 apply? Not per Rev. Rule 70-106 if prearranged and plan adopted before redemption (likely here). But see Riggs case – much room to plan. LLM Corporate Tax Instructor: Dwight Drake

Problem 361-3 Basic Facts: P Corp own all stock of S Corp and holds bonds at face and book value of 1k. Before 332 liquidation, S corp distributes inventory with 10k basis and 1k fair market value to retire debt. Objective: To recognize 9k loss before 332 liquidation. Result: No hope. Step transaction will kill. Note, P corp does pick up 10k basis in inventory per 334(b)(1). LLM Corporate Tax Instructor: Dwight Drake