Download

1 / 24

240 likes | 261 Views

This lecture discusses the general modeling and evaluation of risk attitudes, including the concepts of expected utility, probability weighting, and risk aversion. It explores the historical development of risk theory and challenges the assumption of universal risk aversion.

E N D

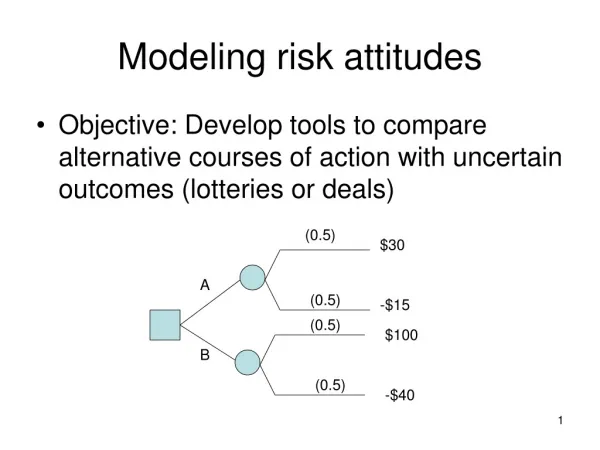

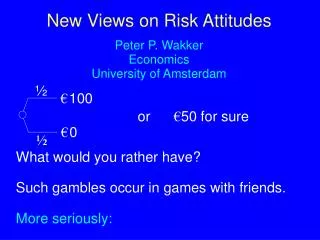

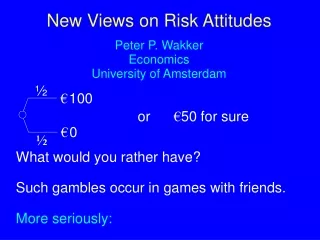

½ €100 €0 or €50 for sure ½ New Views on Risk Attitudes Peter P. WakkerEconomicsUniversity of Amsterdam What would you rather have? Such gambles occur in games with friends. More seriously:

2 In public lotteries, casinos, and horse races. More seriously: - Whether you can study medicine in theNetherlands; - In the US in the 1960s, whether youhad to serve in Vietnam (only for men …) Even more seriously: Investments, insurance, medical treatments, etc. etc. This lecture is on the history of risk-theory.

3 Two questions/lines-of-talk: • General modeling of risk attitude. • Is it determined by: • -sensitivity towards outcomes (utility); • -sensitivity towards chance (probability weighting)? • 2) Particular form of risk attitude. • Is risk-aversion • -universally valid (modulo noise); • - systematically violated?

½ €100 €0 ½ p1 x1 . . . . . . xn pn 4 Simplest way to evaluate risky prospects: Expected value ½100 + ½0 = 50 General: p1x1+ ... + pnxn

€50 ½ €100 €0 ½ 5 However, empirical observations: Risk aversion! Falsification of expected value. To explain it, “expected utility.”

p1 x1 . . . . . . xn pn 6 Expected utility is the classical economic risk theory. p1 x1 + ... + pn xn U( ) U( ) Departure from objectivity. U is subjective index of risk attitude. Bernoulli (1738).

p1x1+ ... + pnxn p1 U x1 . . . . . . € xn pn 7 Risk aversion in general: Theorem (Marshall 1890).Risk aversion holds if and only if utility U is concave. U is used as thesubjective index of risk attitude!

8 Line (1) of this talk: the general modeling of risk attitude. Psychologists objected: U=sensitivity towards money ≠risk attitude.

p1 U(x1)+ ... + pn U(xn) w p1 x1 . . . . . . xn pn p 9 Intuition: risk attitude (also) in terms of processing of probabilities. w( ) w() 1 w(p) w(0) = 0, w(1) = 1, w is increasing. 0 p 0 1

utility 10 Lola Lopes (1987): “Risk attitude is more than the psychophysics of money.” Prob. weighting already considered in 1950s (Ward Edwards). Called subjective expected utility (unfortunate term). 'sargument intuitive, not theoretical. economists: Such argumentation is an error! Subj. exp. ut. theory never became “big.”

11 Line (2) of this talk: risk aversion. • Economic arguments for universal risk aversion: • diminishing marginal utility is intuitively plausible; • concave utility needed for existence of equilibria; • no concave U market for lotteries;

12 Marshall, A. (1920)Principles of Economics about risk-seeking individuals: ... since experience shows that they arelikely to engender a restless, feverishcharacter, unsuited for steady work as wellas for the higher and more solid pleasures of life.

U € 13 Problem: Public lotteries!?!? Friedman & Savage (1948):

14 Arrow (1971, p.90) (about lotteries) I will not dwell on this point extensively,emulating rather the preacher, who,expounding a subtle theological point to hiscongregation, frankly stated: Brethren, here there is a great difficulty; let us face it firmly and pass on. Psychologists: ?????

15 Back to line (1), the general modeling of risk attitude. End of seventies: renewed interest in probability weighting, a.o. because of violations of EU. A.o. by Handa (1978, J. of Pol. Econy), Kahneman & Tversky (1979, Econometrica, "prospect theory"). Prominent economic journals ... !

16 To Handa (1978), the JPE received some 10 comments! Of those, Fishburn (1978, JPE) was published. (Among non-published reactions, one by the unknown Australian John Quiggin.) Prospect theory is an exceptionally big succes; theoretically problematic.

17 Probability-weighting violates stochastic dominance! Amazing, that model could survive in the psychological literature for 30 years ...

18 Yet, "risk-attitude through probability weighting" is good intuition. Only, one should weight the "right“ probabilities. Not probability at: a specific outcome, but probability at: at least an outcome.

p1 x1 . . . . . . xn pn 19 Evaluation of lottery with x1… xn 0: w(p1)U(x1) + (w(p2+p1) - w(p1))*U(x2) + ... (w(pj+...+p1) - w(pj-1+...+p1))*U(xj) + ... (w(pn+...+p1) - w(pn-1+...+p1))*U(xn) Idea of Quiggin (1981), Rank-Dependent Utility.

20 Back to line 2, risk aversion. In the beginning, economists' views: Risk-aversion is universal. U concave and prob. weighting wsimilar. Impulses from empirical investigations by psychologists (Tversky and others).

21 Systematic risk-seeking for: Small chances at large gains Large chances at small losses Amazing, that “universal” risk aversion could survive in the economics literature for 30 years …

22 Synthesis: Tversky, A. & D. Kahneman (1992),“Advances in Prospect Theory: Cumulative Representation of Uncertainty," Journal of Risk and Uncertainty 5, 297-323.

23 Cumulative prospect theory: Risk-attitudes in terms of - utilities ánd - probability weighting (- ánd loss aversion). Risk-aversion prevailing,but, systematic deviations. Reference point ("framing"). Theory combines - descriptive force of prospect theory - theoretical force of econ. theories.

24 Summary: 1. Classical econs: Expected utility; Risk at- titude=U(€) (Bernoulli1738, Marshall1890). 2. s: risk attitude also = w(p) (Edwards, 1954). Took wrong p’s. 3. Econs: Take right ("cumulative“) p’s(Quiggin, 1981). Thought universal risk aversion; convex/cave. 4. s: diminishing sensitive iso risk aversion (Tversky & Kahneman, 1992); S-shaped. Synthesis: Cumulative prospect theory