FINC4101 Investment Analysis

640 likes | 2.28k Views

FINC4101 Investment Analysis. Instructor: Dr. Leng Ling Topic: Asset Pricing Models. Learning objectives. Distinguish between systematic and unsystematic risk. Define the single index model and identify its components. Relate a security’s beta to its systematic risk.

FINC4101 Investment Analysis

E N D

Presentation Transcript

FINC4101 Investment Analysis Instructor: Dr. Leng Ling Topic: Asset Pricing Models

Learning objectives • Distinguish between systematic and unsystematic risk. • Define the single index model and identify its components. • Relate a security’s beta to its systematic risk. • Describe the Capital Asset Pricing Model (CAPM) and list its assumptions. • Identify the implications, applications and limitations of the CAPM. • Use the CAPM to compute an asset’s expected return. • Define the Security Market Line (SML). • Understand the concepts of fairly priced, underpriced and overpriced. • Describe the implementation of the CAPM.

Why do we need an asset pricing model? • An asset pricing model allows us to figure out the required return of an asset. • Required rate of return can be used for: • Valuation of assets. • Identification of attractive investments. • Capital budgeting.

Preparation for CAPM • To understand the CAPM, we need to know the following: • Systematic vs. unsystematic risk • Single index model

Unsystematic risk • Unsystematic risk: uncertainty or variability in returns that affects a specific asset without affecting other assets. • Also known as unique risk, firm-specific risk, diversifiable risk. • Sources of unsystematic risk: litigation, patents, R&D, management style and philosophy, financial leverage, etc

Systematic risk • Systematic risk: uncertainty or variability in returns that affects all risky assets. • Also known as: market risk, nondiversifiable risk • Sources of systematic risk: fluctuation in the stock market, business cycles, inflation rate, monetary policy, exchange rates, wars, political unrest, technological change etc.

Systematic vs unsystematic risk • Diversification works but has its limit. • At the very most, diversification eliminates unsystematic risk. When there is no unsystematic risk, only systematic risk remains, but that is not diversifiable. • It is risk that investors bear in exchange for enjoying the return from investing. After all, bearing risk is a fundamental part of investment. • Investors holding well-diversified portfolios will only demand a risk premium for bearing the systematic risk.

Graphical depiction of systematic and unsystematic risks Well-diversified portfolio virtually eliminates unsystematic risk. As the number of stocks in the portfolio increases, unsystematic risk decreases.

Single-index model of security returns • Statistical model that estimates the systematic and unsystematic risk of a security or portfolio. • Looks at “excess return”, denoted by “R” What is a security’s excess return Security’s HPR in excess of the risk free rate. Excess return of security i, Ri = security i’s HPR – risk-free rate = ri – rf The following discussion focuses on excess returns.

Anatomy of single-index model • Uses a broad index of securities (e.g., S&P500) to represent systematic risk. • This broad index is called, “market index”, “market factor”, or just “market” for short. • Market excess return is denoted RM . • The model says that a security’s excess returnconsists of 3 parts:

Using the single-index model to decompose security risk(p.168) Variance of Ri = Systematic risk + Firm-specific risk = Variance(biRM) + Variance(ei) = bi2 sM2 + s2(ei) Variance of market excess return.

Graphical representation of single-index model: Ri = ai + biRM + ei Scatter diagram Security Characteristic Line

Measuring the importance of systematic risk 2 is the ratio of systematic risk to total risk. = Systematic Risk/Total Risk = bi2sM2 /[ bi2sM2 + s2(ei) ] 2 ranges from 0 to 1 • As 2 1, • Systematic risk becomes a bigger part of total risk. • Points on scatter diagram lie close to regression line. • As 2 0, • Unsystematic risk becomes a bigger part of total risk. • Points on scatter diagram lie away from regression line.

Relevant risk measure for diversified investors • In highly diversified portfolios, unsystematic risk can be virtually eliminated and thus becomes irrelevant. • Only systematic risk remains in diversified portfolios. • In measuring security risk for diversified investors, we focus on the security’s systematic risk, i.e., bi2 sM2 . • Equivalently, we can use bi as the measure of the security’s systematic risk.

Capital Asset Pricing Model (CAPM) • Equilibrium model that underlies all modern financial theory • Derived using principles of diversification with simplified assumptions • Markowitz, Sharpe, Lintner and Mossin are researchers credited with its development • Theoretical model based on a list of simplifying assumptions

Assumptions of the CAPM (1) • Individual investors are price takers • Single-period investment horizon • Investments are limited to traded financial assets • No taxes, and transaction costs • Information is costless and available to all investors • Investors are rational mean-variance optimizers • Homogeneous expectations

Implications of the CAPM • All investors will hold the same portfolio for risky assets – market portfolio (M). • Market portfolio contains all securities. The proportion of each security is its market value as a percentage of total market value of all securities. • Market portfolio will be on the efficient frontier and will be the tangency portfolio. • Capital Allocation Line is now called the Capital Market Line (CML).

Implications of the CAPM (cont’d) • Risk premium on the market depends on: • Average risk aversion of all market participants. • Variance of the market portfolio. • Risk premium on an individual security depends on: • Its beta, b • Market portfolio risk premium

Why all investors hold the market portfolio? All investors • Use identical mean-variance analysis • Apply it to the same set of securities • Have the same time horizon • Use the same security analysis • Have identical tax consequences Arrive at the same efficient frontier and tangency portfolio.

Risk premium of market portfolio E(rM) – rf = A* x (M)2 Expected return: E(rM) = rf+ (A* x M2 ) SD of the return on the market portfolio. Risk aversion of average investor

Risk premium & expected return of single security • For security i, risk premium: E(ri) – rf = i [ E(rM) – rf] Security i’s expected return: E(ri) = rf + i [ E(rM) – rf] Expected return-beta relationship • Formulas also hold for a portfolio of securities.

Portfolio beta, P • The beta of a portfolio, P, • Weighted average of the individual asset betas. • Weights are the portfolio proportions. P = (w1 x 1) + (w2 x 2) + … + (wN x N) Proportion of portfolio invested in asset 1. Asset 1’s beta.

Problem involving portfolio beta • Suppose the market risk premium is 8%. What is the risk premium of a portfolio invested 25% in Coca-Cola and 75% in BellSouth. Coca-Cola has a beta of 0.85 and BellSouth has a beta of 1.2. • Verify that portfolio beta is 1.1125 • Verify that risk premium is 8.9% • Suppose you now invest 20% in the risk-free asset, 25% in Coca-Cola and the rest in BellSouth. What is the portfolio beta and risk premium?

Questions Are the following statements true or false? Explain. • Stocks with a beta of zero offer an expected rate of return of zero. • The CAPM implies that investors require a higher return to hold highly volatile securities. • You can construct a portfolio with a beta of 0.75 by investing 0.75 of the budget in T-bills and the remainder in the market portfolio.

More questions • What is the beta of a portfolio with E(rP) = 20%, if rf = 5% and E(rM) = 15%. • Assume both portfolios A and B are well diversified, and E(rA) = 14% and E(rB) = 14.8%. If the economy has only one factor, and A = 1.0 while B = 1.1, what must be the risk-free rate?

Security market line (SML) Expected return SML M E(rM) Rise Slope = rise / run = (E(rM) – rf)/ 1 = market risk premium Risk-free rate, rf Run 0 1

Security market line (SML) • Graphical representation of the expected return-beta relationship. • Provides a benchmark for evaluating investment performance. • Given an investment’s beta, the SML tells us the return we should require or demand from this investment. • “Fairly priced” assets plot exactly on the SML. “Underpriced” assets plot above the SML. “Overpriced” assets plot below the SML.

Fairly priced security • Suppose stock A is currently priced at $45. Everyone agrees that its year-end price will be $50 and a dividend of $2.02 will be paid then. • Stock A’s beta is 1.2, the market portfolio’s expected return is 14% and the risk-free rate is 6%. • Given the stock price and future cash flows, expected HPR = (50 + 2.02 – 45)/45 = 0.156 or 15.6% • CAPM’s expected return = 6 + 1.2[14 – 6] = 15.6% ! • Stock A is FAIRLY PRICED. Its current price leads to an expected return that is EXACTLY equal to the expected return indicated by the CAPM. • So, CAPM says that $45 is the “correct” price for A given it’s risk. • This stock plots exactly on the SML.

Underpriced security • Now supposed everything stays the same, BUT stock A is now priced at $44.46. • Given the stock price and future cash flows, expected HPR = (50 + 2.02 – 44.46)/44.46 = 0.17 or 17% • But CAPM says stock A should provide 15.6% return and it should be worth $45. • Stock A is UNDERPRICED. It’s price of $44.46 is LESS than the CAPM price of $45. • Also, A’s expected return given its price is 17% which is MORE than the CAPM expected return of 15.6% • Stock A now plots ABOVE the SML.

Overpriced security • Now supposed everything stays the same, BUT stock A is now priced at $46.04. • Given the stock price and future cash flows, expected HPR = (50 + 2.02 – 46.04)/46.04 = 0.13 or 13% • But CAPM says stock A should provide 15.6% return and it should be worth $45. • Stock A is OVERPRICED. It’s price of $46.04 is MORE than the CAPM price of $45. • Also, A’s expected return given its price is 13% which is LESS than the CAPM expected return of 15.6% • Stock A now plots BELOW the SML.

All together now Alpha: Difference between expected HPR and the return predicted by the CAPM.

Fairly priced, underpriced, overpriced When stock A is UNDERPRICED, it plots above the SML. When stock A is fairly priced, it plots exactly on the SML. 13 When stock A is OVERPRICED, it plots below the SML.

Capital Allocation Line (CAL) CAL becomes CML when the market portfolio is used as the risky portfolio

CML Graphs expected return of market portfolioagainst standard deviation. Efficient portfolios SD is the valid risk measure. SML Graphs expected return of individual assetagainst beta. Individual assets, portfolios Beta is the valid risk measure Capital Market Line (CML) vs. Security Market Line (SML)

Questions • The SML depicts: • A security’s expected return as a function of its systematic risk. • The market portfolio as the optimal portfolio of risky securities. • The relationship between a security’s return and the return on an index. • The complete portfolio as a combination of the market portfolio and the risk-free asset.

Applications of the CAPM • Identification of attractive investments. • Positive alpha / underpriced assets. • Valuation of assets. • CAPM expected return is used as discount rate to find the value of assets. • Capital budgeting. • “Hurdle rate” for project under consideration. • Rate-setting for utilities. • Rate of return that a regulated utility should be allowed to earn.

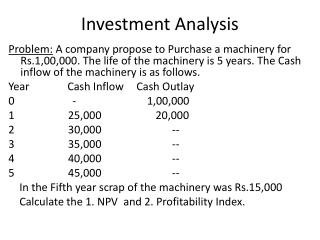

Karen Kay, a portfolio manager at Collins Asset Management, is using the CAPM for making recommendations to her clients. Her research department has developed the information shown in the following exhibit Identifying attractive investment (1)

Calculate expected return and alpha for each stock. Identify and justify which stock would be more appropriate for an investor who wants to: Add this stock to a well-diversified equity portfolio. Hold this stock as a single-stock portfolio. Identifying attractive investment (2)

Valuation of assets (1) • The market price of a security is $40. its expected rate of return is 13%. The risk-free rate is 7%, and the market risk premium is 8%. What will the market price of the security be if its beta doubles (and all other variables remain unchanged)? Assume the stock is expected to pay a constant dividend in perpetuity.

Valuation of assets (2) • The risk-free rate is 4%. Suppose that the expected return required by the market for a portfolio with a beta of 1.0 is 12%. According to the CAPM: • What is the expected return on the market portfolio? • What would be the expected return on a zero-beta stock? • Suppose you consider buying a share of stock at a price of $40. the stock is expected to pay a dividend of $3 next year and to sell then for $41. The stock’s beta is -0.5. is the stock overpriced or underpriced?

Capital budgeting (1) • Texaco is considering a new oil rig in the Gulf of Mexico. The business plan forecasts an internal rate of return of 17% on the investment. Research shows that the beta of similar projects is a whopping 2.2! The risk-free rate is 4% and the market risk premium is 8%. Compute the hurdle rate for the project. • Should the project be accepted?

Capital budgeting (2) • You are an analyst at Goldman Sachs. You are covering a company which is considering a project with the following net after-tax cash flows : an outlay of $20 mil right now (t= 0), $10 mil at the end of each of the first nine years and $20 mil at the end of year 10. The project is terminated after 10 years. The project’s beta is 1.7. Assuming rf= 9% and E(rM) = 19%, what is the project’s NPV?

Rate-setting for utilities • Example: Suppose GPower is a utility providing power to Georgia. The state of Georgia decides the rate of return that GPower can earn on its investment in plant and equipment. • Suppose the firm is 100% equity-owned and assets are $100 million. The firm’s beta is 0.8. The risk-free rate is 5% and the market risk premium is 8%. • If regulators use the CAPM for setting rates, they will allow GPower to set prices at a level to generate what level of profits?

Implementing the CAPM (1) The CAPM can be used in several ways. To apply it, we need to calculate a security’s beta. There are two major problems in calculating beta: • Market portfolio of all assets is unobservable. • The CAPM gives a relationship between expected return and beta. Expected returns are unobservable. How do we get round these problems?

Implementing the CAPM (2) Solutions: • Use an actual portfolio, e.g., S&P 500 stock index, as a proxy for the theoretical market portfolio. The proxy represents systematic risk in the economy. • Use realized (i.e., past) returns instead of expected returns to estimate beta. .

Implementing the CAPM (3) • Use linear regression to estimate the single-index model: ri - rf = i + i(RM-rf)+ ei Excess return due to firm-specific events. Excess return of stock i Excess return on stock index (e.g., S&P500). Excess return when index portfolio has 0 excess return. Period can be month, week, day.