Demand

Section 4.1. Demand. Demand. Two requirements for demand the desire to own something, and the ability to pay for it An inverse relation of quantity demanded and price of a good . The Law of Demand. Consumers buy more if price decreases and less if price increases

Demand

E N D

Presentation Transcript

Section 4.1 Demand

Demand • Two requirements for demand • the desire to own something, and • the ability to pay for it • An inverse relation of quantity demanded and price of a good

The Law of Demand • Consumers buy more if price decreases and less if price increases • As price drops, demand rises

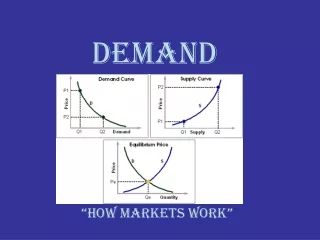

Demand Curve • A graphic representation of a demand curve • Vertical axis • Price of the good • Horizontal axis • Number of units demandedof the good Price $ Demand units

Demand Schedules • Demand Schedule • A table that lists the quantity of a good each person will buy at each different price • Market Demand Schedule • A table that lists the quantity of a good that all consumers in a market will buy at each different price

Simple Demand Curves Demand Curve Market Demand Curve

Demand for Cookies Demand Schedule Demand Curve

Substitution Effect • A substitute is a nearly equivalent good • If the price of pizza goes up, you might substitute tacos. • When consumers react to an increase in a good’s price by consuming less of that good and more of other goods

Income Effect • The change in consumption resulting from a change in real income • Consumption – the amount of a good that is bought • As income increases, demand increases

Section 4.2 Shifts in the Demand Curve

Ceteris paribus • “all other things held constant” • Economists simplify models by changing only one thing at a time

Shift in the Demand Curve Left ShiftDecrease in Demand Right ShiftIncrease in Demand DemandDecrease DemandIncrease Change Along a Curve Price $ Price $ Price $ Demand units Demand units Demand units

Changes in Demand • Income • People buy more if income increases • Expectations • People buy more if the economy is improving • Population • Demand increases if the number of customers increases • Tastes and advertising • Prices of related goods

Related Goods • Complements – purchased along with other goods • skis • ski boots • • • • • Substitutes – purchased in place of other goods • skis • snowboards • • • •

Effect of Related Goods on Demand • Increase in price for one good reduces demand for complementary goods • Price of skis ↑ • Demand for skis ↓ • Demand for ski boots ↓ • Increase on price of one good increases demand for substitute goods • Price of skis ↑ • Demand for skis ↓ • Demand for snowboards ↑

Section 4.3 Elasticity of Demand

Definitions • Elasticity of Demand • How consumers react to a change in price • Inelastic Demand • Demand is NOT SENSITIVE to a change in price • If price changes, demand does NOT change • Elastic Demand • Demand is VERY SENSITIVE to a change in price • If price changes, demand DOES change

Factors Affecting Elasticity • Availability of substitutes • Relative importance • Necessities vs. luxuries • Changes over time

Test for Elasticity of Demand ELASTIC INELASTIC There are no substitutes, or Buyer’s budget is not limited , or Good is perceived as a necessity • There are substitutes, or • Buyer’s budget is limited , or • Good is perceived as a luxury

Supply Chapter 5

Section 5.1 Understanding supply

Thinking Backwards • Now you understand DEMAND • You naturally think like a CONSUMER • Demand occurs AFTER the goods are made • You must think backwards to understand SUPPLY • You must think like a SUPPLIER • Supply planning occurs BEFORE the goods are made

Supply • Supply • The amount of goods available • Quantity Supplied • The amount of a good offered for sale at a specific price

The Law of Supply Price $ • Law of Supply • The tendency of suppliersto offer more of a goodat a higher price • New suppliers will entera market as prices rise • DIRECT relationship between price and supply Quantity Supplied units

Simple Supply Curves Individual Supply Curve Market Supply Curve

Supply of Cookies Supply Schedule Supply Curve

Elasticity of Supply • Elasticity of Supply • The measure of the way quantity supplied reacts to a change in price • Inelastic Supply • Supply is NOT SENSITIVE to a change in price • Agricultural products in the short term • Elastic Supply • Supply is VERY SENSITIVE to a change in price • Barber shops in the short term

Section 5.2 Costs of production

Cost Elements (Consumables) • Labor • Workers assigned to production of a good or service • Materials • Other resources required to produce a good or service

Production Costs • Fixed • Does not change, no matter how much output is produced • Variable • Rises or falls depending on the level of output • Total • Fixed plus variable costs • Marginal • Cost of producing one more unit of output

Marginal Analysis - Revenue • Marginal Revenue • Revenue received from one additional unit of output • Usually the market price • Total Revenue • Revenue received from all units of output at each level

Marginal Analysis - Cost • Marginal Cost • Cost to produce one additional unit of output • Total Cost • Cost to produce all units of output at each level

Marginal Analysis - Profit • Profit • Total Revenue minus Total Cost • MarginalProfit • Profit generated by one additional unit of output • Marginal Revenue – Marginal Cost

Optimum Production Level - 1 Total Cost and Revenue Marginal Cost and Revenue

Conclusion • The optimum production level is the one that gives maximum profit • Maximum profit occurs whenMarginal Cost = Marginal Revenue

Marginal Product of Labor • Increasing the number of workers increases the output of the good or service, until … Increasing Marginal ReturnsMore workers – more output Diminishing Marginal ReturnsMore workers – less output Negative Marginal ReturnsMore workers – output stops

Marginal Product of Labor – cont’d. Adding workers improves productivity … until it doesn’t “Too many cooks spoil the broth”

Section 5.3 Changes in Supply

Shifts in the Supply Curve • Firms change the supply in order to maximize profits

Factors That Affect Supply • Input Costs • Government Influence • Global Economy • Other Influences • Supplier Location

Input Costs • Higher Costs → Lower Profits • e.g., higher raw material costs • Marginal costs increase • Firms reduce supply • Lower Costs → Higher Profits • e.g., higher process efficiency from improved technology • Marginal costs decrease • Firms increase supply

Government Influence • Subsidies • Payments by the government to firms • Encourage production by lowering costs • e.g., farm subsidies • Excise taxes • Payments collected by the government from firms • Discourage production by raising costs • e.g., cigarette and alcohol taxes

Government Influence (cont’d.) • Regulation • Government intervention in the market that affects price, quantity or quality • Usually increases costs • Compliance with regulation • Design changes • Can decrease revenue • Restrictions on advertising • Firms often reduce supply

Influences of Global Economy • Changes in supply in manufacturing countries • Import restrictions • Ban – import not allowed • Quota – limited number of imports • Duty – tax on imports • Import restrictions affect supply • Reduce supply directly • Increase costs

Other Influences on Supply • Future Expectations • Expected price rise • Sellers hold product off the market until prices rise • Expected price drop • Seller push supply onto the market to capture the current price • Number of Suppliers • As suppliers enter the market, supply increases • As suppliers leave the market, supply decreases