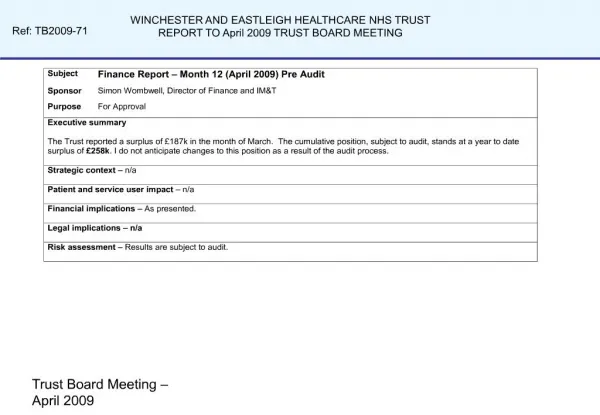

kpmg

kpmg. An Introduction to Workers Compensation Alternative Risk Transfer Mechanisms and the Bermuda Insurance Market James Matusiak FCAS,MAAA. Overview. Workers Compensation Overview Captives and Fronting Arrangements Finite Reinsurance The Bermuda Insurance Market. Workers Compensation.

kpmg

E N D

Presentation Transcript

kpmg An Introduction to Workers Compensation Alternative Risk Transfer Mechanisms and the Bermuda Insurance Market James Matusiak FCAS,MAAA

Overview • Workers Compensation Overview • Captives and Fronting Arrangements • Finite Reinsurance • The Bermuda Insurance Market

Workers Compensation • Workers Compensation is one of the largest risks for businesses around the world. • Workers Compensation benefits reimburse employees for lost wages and medical expenses incurred as a result of work-related injuries or disease. • Benefits are usually dictated by state workers compensation statutes. In addition, benefits are no-fault, they are paid without regard to fault of the employer or the employee.

Workers Compensation • To handle the workers compensation exposure, there are two main options: Workers Compensation Risk • Traditional Insurance Programs • Traditional Insurance • Experience Rating • Retrospective Rating • Large Dollar Deductible Programs • Alternative Risk Transfer Programs • Captives • Finite Reinsurance

Workers Compensation Traditional Risk Transfer • Historically, businesses purchased traditional insurance policies to cover their workers compensation risk. The insured paid a premium and the insurer took on all of the risk (minus a small deductible). Insurer Business (Insured) Premium Coverage

Workers Compensation Traditional Risk Transfer • As workers compensation rates rose, large businesses looked to control their insurance costs. This evolved into experience and retrospective rating schemes. • Experience rating: A company’s premium is derived by looking at their own historical loss experience. • Retrospective rating: A company pays a deposit premium based on historical losses but may have to pay more or receive a premium refund based on their current year losses. Retrospective premiums are capped at a minimum and a maximum. • Both of these options are within the scope of traditional insurance programs

Workers Compensation Alternative Risk Transfer • Companies still wanted more options to control their insurance costs. This demand created the need for captives and finite reinsurance. • Captives: A subsidiary of a corporation who insurers the risks of its parent. Premium is collected and losses are paid into and out of a separate balance sheet. • Finite Reinsurance: An insurance contract written by a third party reinsurer that covers the risks of an insured. Loss payments are capped at an aggregate or “finite” amount. • Both of these options are typically referred to as alternative risk transfer.

Captives • As mentioned above, captives are usually subsidiaries that cover the insurance risks of their parent company. Other ownership structures are possible. • Captives operate under a separate balance sheet. • Captives operate as reinsurers of the risk through what is referred to as a fronting arrangement. • The majority of captives are managed by third parties. • Parent companies still have to provide coverage up to statutory limits.

Insurer Business (Insured) Premium Coverage How a Captive Arrangement Works Profit/Loss Coverage Premium Captive (Insured)

Captives – Fronting Arrangements • Due to the fact that workers compensation rates and policy forms are regulated, the traditional insurance process is kept in place for policy issuance purposes. • The fronting insurer issues the policy on its own paper (“policy form”). • The fronting insurer then cedes the risk to the captive using a reinsurance contract. • For this service the fronting insurer collects a fronting commission. • It is common practice for the insured to post a letter of credit to the fronting company to cover the credit risk of the captive.

Captives – In operation • Captives are domiciled in jurisdictions that have special insurance legislation in place. • Most captives are managed in their jurisdictions by a captive manager. The captive manager handles the accounting and will assist the captive in placing its reinsurance. • Claims are either adjusted using a Third Party Administrator (“TPA”) or the fronting insurer. • Captives seldom retain all of the risk of the parent. This is mostly due to the capital restraints of the captive.

Captives – Advantages • Captives allow a company to retain its own risk. Most companies are more likely to engage in risk control if they are ultimately responsible for the cost of that risk. • By “self-insuring”, an insured does not fund the profit provisions built into the rates of a third-party insurer. • Captives allow companies to insure themselves for unique risks, where coverage may not be available in the marketplace. • Captives allow the insured to access the reinsurance markets that may have more favorable policy terms than the traditional marketplace. • Captives generally have some tax advantages for the parent company.

Captives – Challenges • Captives must be capitalized. This capitalization is generally dictated by the amount of risk retained by the captive. • Captives may have high administrative costs. The owner must pay someone to manage the captive, pay claims, conduct actuarial work, and audit the company. • A captive is more risky than a large book of business with many insured entities.

Finite Reinsurance • Finite reinsurance contracts are insurance policies containing coverage very similar to traditional policies but differ from traditional policies in their loss limits and premium arrangements. • A contract is written with an aggregate limit offering a fixed maximum amount of coverage.

Finite Reinsurance (cont.) • The premium for the contract is split into two components: the funds withheld account and the underwriting fee. • The fee is paid directly to the reinsurer and is booked as profit on day 1. • The funds withheld account is set up and losses are paid out of this account. The account also earns interest that lowers the amount of premium needed to fund the losses. • In the event the funds withheld account is deficient, the insurer pays for additional losses up until their aggregate limit. Any money remaining in the funds withheld account at the end of the contract period are returned to the insured.

How a Finite Reinsurance Contract Works $120 in Insurance Coverage Purchased for $100 Reinsurer $5 in fees to the reinsurer Funds Withheld Account = $95 $95 to the funds withheld account Year End $5 in interest earned by the FWH account. Result: Reinsurer pays $10, the insured receives no refunded premium. Result: Reinsurer pays nothing and the insured receives $50 refunded premium. Funds Withheld Account = $100 Poor Loss Year, Losses = $110 Good Loss Year, Losses = $50

Finite Reinsurance – Advantages • Finite reinsurance provides many of the risk retention characteristics of a captive because of the return premiums but does not require the capitalization of a captive. • Essentially finite reinsurance allows you to “borrow the balance sheet” of the reinsurer. • Finite reinsurance does not require the administration and setup costs of a captive. • The policyholder is allowed to use the investment gains of the funds withheld account to offset their insurance costs.

Finite Reinsurance – Challenges • Finite reinsurance contracts may contain high reinsurer fees. These fees are high due to: • The reinsurer’s profit provisions. • The use of the reinsurers capital. • The accounting for finite reinsurance contracts is very complex and under certain scenarios may not qualify for insurance accounting treatment.

The Bermuda Insurance Market • Bermuda is an island 600 miles off of the coast of North Carolina. It is roughly 22 square miles in size and has a population of 60,000. • Beginning in the seventies, a significant number of large corporations began forming captive insurance companies in Bermuda. • Currently Bermuda has over 1,500 insurance companies with over 1,300 of those being captives.

The Bermuda Insurance Market • In addition to captives, Bermuda is home to some of the world’s largest reinsurers: • Renaissance Re • Ace Ltd • XL Capital • Almost every player (brokers, insurers, captive managers, audit firms and consultants) in the insurance market has a presence in Bermuda. • “The Silicon Valley of Insurance”

Why Bermuda? • Bermuda has a regulatory system that is favorable to insurers. • Bermuda companies do not pay income tax. • Over the years, Bermuda has attracted some of the most talented players in the insurance industry. • The proximity to financial centers such as London and New York.

Bermuda Regulations • Bermuda has four classes of insurance licenses to meet the needs of companies ranging from small captives to large multinational reinsurers. • Bermuda has an Insurance Advisory Committee which is made up of local executives that advise the government on new applications for insurance licenses. • Bermuda has minimal capitalization standards and requires an annual actuarial opinion.

Bermuda Regulations • Bermuda has become home to many boutique and alternative insurance products due to its regulatory framework. Such as: • Catastrophe Bond Issues • Weather Derivatives • Collateralized Debt Obligations • Shrimp Mortality Insurance????

Who are the big players in Bermuda? • ACE • $38 Billion in assets • Multi-national, multi-line insurer • XL • $28 Billion in assets • Multi-national, multi-line insurer • Renaissance Re • $3 Billion in assets • Major Property Catastrophe Insurer • 20 Other Insurers (and growing) with an asset base over $1 Billion

The September 11th Effect • On September 11th the industry lost as much as $40 Billion. • Within 6 months Bermuda saw an influx of some $10 Billion of capital and five new insurers capitalized at over $1 Billion dollars each: • Arch Capital Group • Axis Specialty Ltd. • Allied World Insurance Company • Endurance Specialty Insurance Ltd. • Montpelier Reinsurance Ltd.

Future Bermuda Challenges • Can a small, highly populated island continue to support the growth of the international business sector: • Housing • Schools • Health Care • Underwriting and Management Talent • Bermuda is subject to political risk both domestically and abroad (ie tax changes).

Contact Information • If anybody has any questions regarding this presentation or just wants to talk about the insurance industry feel free to contact me: James Matusiak KPMG (441) 294-2624 jmatusiak@kpmg.bm