Download

1 / 25

250 likes | 423 Views

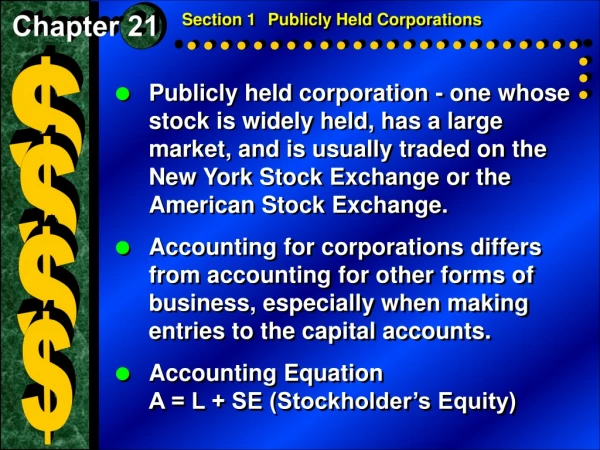

Section 1 Publicly Held Corporations. Chapter 21. $. Publicly held corporation - one whose stock is widely held, has a large market, and is usually traded on the New York Stock Exchange or the American Stock Exchange.

E N D

Section 1 Publicly Held Corporations Chapter 21 $ • Publicly held corporation - one whose stock is widely held, has a large market, and is usually traded on the New York Stock Exchange or the American Stock Exchange. • Accounting for corporations differs from accounting for other forms of business, especially when making entries to the capital accounts. • Accounting EquationA = L + SE (Stockholder’s Equity) $ $ $

Chapter 21 Characteristics of a Corporation $ • Legal Permission to Operate • Charter and Articles of Incorporation required • Separate Legal Entity • Stockholders • Professional Management • Board of Directors - Elected by Stockholders $ $ Advantages Disadvantages $ • Easier to raise money • Easy to expand • Easy to transfer ownership • Losses limited to investment • Costs more to start up • Complex to organize • More regulations • Higher taxes

Section 1 Publicly Held Corporations Chapter 21 $ Stockholders’ Equity = PIC + RE Reported by corporations in two parts: $ • Paid-in-Capital - the equity that is paid into the corporation by stockholders • Retained Earnings - the equity earned by the corporation and retained in the business • Permanent account • Credited for a net income • Debited for a net loss • Normal balance - credit $ $

Section 1 Publicly Held Corporations Chapter 21 Paid-in-Capital accounts = CS + PS + PIC exc CS + PIC exc PF $ • Common Stock • Permanent account - Credit balance • Stores the par value of issued shares • Preferred Stock • Permanent account - Credit balance • Stores the par value of issued shares • Paid-in Capital in Excess of Par • Permanent account - Credit balance • Stores the excess over par when a corporation sells its stock at a price that is above par $ $ $

Section 1 Publicly Held Corporations (cont'd.) Chapter 21 $ Capital Stock • The maximum number of shares a corporation may issue is called its authorized capital stock. • The amount assigned to each share is referred to as par value, the per-share dollar amount printed on the stock certificates. $ $ $

Section 1 Publicly Held Corporations Chapter 21 $ Common Stock The owners of common stock participate in the corporation as follows: $ • Elect the board of directors and, through them, exercise control over the operations of the corporation – voting rights. • Share in the earnings of the corporation by receiving dividends declared by the board of directors – amount determined by board of directors. • Entitled to share in the assets of the corporation if it goes out of business. • voting rights (yes), dividend rights (2nd), asset rights (2nd) $ $

Section 1 Publicly Held Corporations Chapter 21 $ Preferred Stock Owners of preferred stock participate as follows: $ • No voting rights • Entitled to receive dividends before common stockholders – amount stated as part of stock description. • Given preference over common stockholders to the assets of the corporation should it go out of business. • voting rights (no), dividend rights (1st), asset rights (1st) $ $

Chapter 21 On Your Mark Athletic Wear On January 3 On Your Mark Athletic Wear was incorporated and was authorized to issue 20,000 shares of $10 par common stock and 1,000 shares of $100 par 6%preferred stock

Section 1 Publicly Held Corporations Chapter 21 Issuing Common Stock at Par Business Transaction On January 3 On Your Mark Athletic Wear issued 10,000 shares for $10 par common stock at $10 per share. Memorandum 3. JOURNAL ENTRY

Section 1 Publicly Held Corporations Chapter 21 Issuing Common Stock in excess of Par Business Transaction On January 5 On Your Mark Athletic Wear issued 5,000 shares for $10 par common stock at $11.50 per share. Memorandum 3. JOURNAL ENTRY

Section 1 Publicly Held Corporations Chapter 21 Issuing Preferred Stock at Par Business Transaction On January 4, On Your Mark issued 250 shares of preferred 6% stock, $100 par, at $100 per share. Memorandum 5. JOURNAL ENTRY

Section 1 Publicly Held Corporations Chapter 21 Issuing Preferred Stock in excess of Par Business Transaction On January 4, On Your Mark issued 250 shares of preferred 6% stock, $100 par, in excess of par at $115 per share. Memorandum 5. JOURNAL ENTRY

Section 2 Distributing the Earnings of a Corporation Chapter 21 $ Dividends • Distribution of profits to the share-holders; done in the form of dividends. • The corporation’s board of directors declares, or authorizes, the dividends. • The corporation should have sufficient cash available to pay the dividend. • There must be an adequate balance in the Retained Earnings account. • Dividends normally declared annually, semi-annually, or quarterly. $ $ $

Section 2 Distributing the Earnings of a Corporation Chapter 21 $ Three Important Dates in the Dividend Process • Date of Declaration – The date on which the board of directors declares or authorizes a dividend. • Journal entry required • Date of Record – Persons who own the stock on this date are entitled to the dividend. • Date of Payment – The date on which the dividend is paid. • Journal entry required $ $ $

Section 2 Distributing the Earnings of a Corporation Chapter 21 $ Dividends Account • Used to record the dividends declared. • A liability account, Dividends Payable, is used to record the amount of dividends that will be paid on the payment date. • When the dividends are paid, Cash is credited and Dividends Payable are debited $ Dividends $ Credit – Decrease Side Debit + Increase Side Normal Balance $

Section 2 Distributing the Earnings of a Corporation Chapter 21 $ Dividends Account • A contra-stockholders’ equity account. • A temporary account • Closed in a separate closing entry (the 4th closing entry) after Income Summary is closed. • Closed directly into Retained Earning $ $ $

Section 2 Distributing the Earnings of a Corporation Chapter 21 Recording declaration of dividends Business Transaction On November 15, the board of directors for On Your Mark declared an annual cash dividend on the 500shares of preferred 6%, $100 par stock issued. The dividend is payable to preferred stockholders of record on November 29. The dividend will be paid on December 15. Memorandum 215. JOURNAL ENTRY

Section 2 Distributing the Earnings of a Corporation Chapter 21 Recording payment of dividends Business Transaction On December 15, On Your Mark issued Check 1373 in payment of the dividend on preferred stock declared November 15. JOURNAL ENTRY

Section 3 Financial Reporting for a Publicly Held Corporation Chapter 21 Financial Reporting Stockholders and managers examine financial reports to determine the health of a corporation. $ $ The Income Statement $ • Federal corporate income taxes paid by a corporation are reported separately on the income statement. • Operating Income (Net income before taxes) • - Less Federal Corporate Income Taxes • = Net Income (Net income after taxes) $

Section 3 Financial Reporting for a Publicly Held Corporation Chapter 21 $ Statement of Stockholders’ Equity • Reports the changes in all of the stockholders’ equity accounts during the period. • Prepared from the worksheet and the general ledger • Includes • the number of shares of each type of stock issued • the total amount received for those shares • the net income for the period • The dividends declared during the period • More detailed for a publicly held corporation • Retained earnings: Beginning RE +/- NI – Dividends Declared = Ending RE $ $ $

Paid-in-Capital Formula for Statement of Stockholder’s Equity: Beginning balance + stock issued +/- net income/loss – cash dividends = ending balance

Section 3 Financial Reporting for a Publicly Held Corporation (cont'd.) Chapter 21 $ Balance Sheet • The stockholders’ equity section of a publicly held corporation’s balance sheet is more detailed than that of a closely held corporation. • Each type of stock issued is listed separately under the heading “Paid-in Capital.” • Retained Earnings is listed separately • Ending Balance on the Statement of Stockholders’ Equity $ $ $

Total # shares issued * Total # shares issued * Amounts come from ending balance of Statement of Stockholder’s Equity