Understanding Options: Definition, Strategies, and Market Dynamics

An option is a marketable security that grants the holder the right but not the obligation to buy an asset at a specific price before a particular date. This guide explores key terms such as holder, writer, and option premium, alongside fundamental strategies including call and put purchases. It explains the difference between American and European options, highlights important profit graphs, and discusses the role of the Options Clearing Corporation in enhancing marketability. Whether you're a beginner or seasoned investor, grasping these concepts is crucial for successful trading.

Understanding Options: Definition, Strategies, and Market Dynamics

E N D

Presentation Transcript

OPTIONS Concepts Market

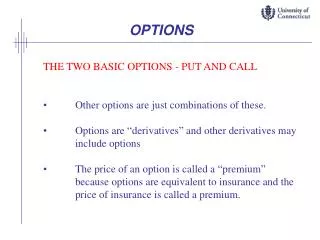

Definition Option is a marketable security which gives the holder the right (but not the obligation) to buy an asset (stock, bond, currency, index, or futures contract) at a specific price (exercise price: X) on or possibly before a specific date (expiration date: T).

Terms • Holder: Buyer of the option; has the right to exercise; short position. • Writer: Seller of the option; has the responsibility to fulfill the terms of the option if the holder exercises. • Option Premium: Price of the option: • C = call premium • P = put premium

Terms • American Option: can be exercised at any time on or before the expiration date. • European Option: can be exercised only on the expiration date. • Symbols: • T = Expiration when the option is exercised. • o = current period • t = any time between current and expiration

Fundamental Strategies • There are six fundamental strategies: • Call Purchase • Naked Call Write • Covered Call Write • Put Purchase • Naked Put Write • Covered Put Write

Profit Graph • Option Strategies can be evaluated in terms of a profit graph. • A profit graph is a plot of the option position’s profit and stock price relation at expiration or when the option is exercised.

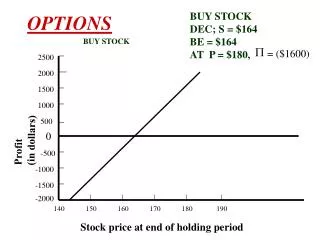

Call Purchase • Buy ABC 50 call for 3.

Naked Call Write • Sell ABC 50 call for 3.

Covered Call Write • Long 50 stock, short 50 call at 3.

Put Purchase • Buy ABC 50 put for 3.

Naked Put Write • Sell ABC 50 put for 3.

Covered Put Write • Short ABC stock at 50, short put at 3.

Straddle Purchase • Buy 50 put for 3 and buy 50 call for 3:

Bull Spread • Buy 50 call for 3 and sell 55 call for 1:

Simulated Long Stock Position • Buy 50 call for 3, sell 50 put for 3:

Option Price Relations: Calls • The price of a call must be at least equal to its intrinsic value (IV). • IV = Max[St-X,0] • If C < IV, there is an arbitrage opportunity from buying the call, exercising, and then selling the stock in the market. • In the absence of arbitrage:

C = IV + TVP • Call Price Curve

Call Function • Call Function:

Note on Variability • The call ( or put) price is positively related to the variability in the underlying stock. This is due to the limited loss feature of options. • Greater volatility suggests a likelihood that the stock will increase substantially and a likelihood it will decrease substantially. • However, given that a call’s losses are limited to just the premium, the extent of the price decrease is inconsequential.

Option Price Relations: Puts • The price of a put must be at least equal to its intrinsic value (IV). • IV = Max[X-St,0] • If P < IV, there is an arbitrage opportunity from buying the put, buying the stock, and exercising. • In the absence of arbitrage:

P = IV + TVP • Put Price Curve:

Put Function • Call Function:

Put-Call Parity Model • Since the call and put derive their values from the underlying stock, the prices of the call, put, and stock are related. The relation governing their prices is know as the Put-Call Parity Model. • The model is based on showing that a long stock, long put, and short call position (conversion) yields a riskless return equal to X at expiration and thus is equal to a price of RF security.

Put-Call Parity Condition • Since the conversion yields a riskless return equal to X at expiration, its value should be equal to the price of a riskless PDB with a face value of X and a maturity equal to T:

Option Market • Options are traded on organized exchanges. • Noted Exchanges: • CBOE • PSE • PHLX • The purpose of any exchange is to provided marketability.

Marketability • Option Exchanges provide marketabilty by: • Listings • Standardization • Set: X, T, and Size • Market Makers or Specialist • Option Clearing Corporation

Option Clearing Corporation • Option Clearing Corporation (OCC) is a clearinghouse which guarantees the writer’s position on each contract and acts as an intermediary. • As an intermediary, the OCC breaks up every contract after it has been established. By doing this, the OCC makes options more marketable.

OCC Example • Suppose A buys an ABC 50 call from B for 3: A is long; B is short. • After this contract is established, OCC breaks it up. • A’s right to exercise is now with the OCC, and B’s responsibility is when the OCC exercises - which could be when someone (not just A) notifies the OCC they want to exercise.

OCC Record: Entry 1 • A: Right to exercise • B: Responsibility

Offsetting Transaction for ‘A’ • Suppose the price of ABC stock increases to $60, pushing the price of the ABC 50 call up to $12. • Seeing the opportunity to profit, suppose A sells an ABC 50 call to C for $12. • OCC breaks up this contract. • OCC’s new entry of responsibility for A cancels A’s right entry: A’s position is closed.

OCC Record Entry 2 • A: Right to exercise • B: Responsibility • A: Responsibility • C: Right to Exercise

Offsetting Transaction for B • Suppose when the price of ABC stock is at $60 and the price of the ABC 50 call is at $12, B begins to worry and decides to close his short position. He can do this by going long in the ABC 50 call. • Suppose B buys an ABC 50 call from D. • OCC breaks up contract. • OCC’s new entry of right for B cancels B’s responsibility entry: B’s position is closed.

OCC Record Entry 3 • B: Responsibility • C: Right • B: Right • D: Responsibility

Importance of the OCC • By acting as an intermediary, the OCC makes it possible for option investors to close their positions. • In this example: • ‘A’ was able to buy an ABC 50 call for 3, then later close her position by selling another ABC 50 call for 12: Profit = 9. • ‘B’ was able to sell an ABC 50 Call for 3, then later close his position by buying another ABC 50 call for 12: loss = 9.

Types of Transactions • Opening • Exercising • Expiring • Closing (or Offsetting)

Option Costs • Margin Requirements: • Initial Margin: Option writers are required to deposit cash or risk-free securities with their brokers to secure their positions. • Maintenance Margin: Writers are required to post additional cash of RF securities when stock prices move against them. See JG: 40-46. • Other Costs: Commissions; bid-ask spread.

Other Options • Stock Indices • Warrants • Rights • Foreign Currency • Debt Securities • Futures

Stock Index Option • Options on stock indices: S&P 500, S&P 100, and MMI. • Features: • Cash Settlement: when you exercise, the assigned writer pays you the difference between the closing (spot) index (S) and the exercise price; Call: S-X; Put: X-S. • Multiplier: $100.

Portfolio Insurance • An important use of stock index options is portfolio insurance. This is a hedging strategy in which an equity portfolio manager protects the future value of her fund by buying index put options. • The put options provide downside protection against a market decline, while allowing the fund to grow if the market increases.

Portfolio Insurance Example • Suppose a fund manager has a $50M portfolio that he may have to liquidate in September. The fund is well-diversified with a beta of 1.25. The current S&P 500 is at 1250, and there is a September S&P 500 put with an exercise price of 1250, multiplier of 100, and trading at 50. • To form a portfolio insurance position, the manager would need to buy Beta(50M)/X =500 puts at a cost of $2.5M= (100)(500)(50).

Other Index Uses • Speculating on the market. • Market Timing • Speculating on Unsystematic Factors • Dynamic Portfolio Insurance

Warrant • Warrant is a call option issued by a Co. • The contractual features of a warrant and a call are the same. • The primary difference between a warrant and a call is that the writer of the warrant is the issuing corporation. • If a warrant is exercised, the corporation receives cash and creates new shares -- dilution effect.

Warrants Example • Example: LM Co. is a $100,000 oil well company; all equity, with 100 shares outstanding and with each share worth $1000; has 4 shareholders, A, B, C, and D, each with 25 shares. • Consider alternatives: Shareholder D sells a call option to investor E, giving her the right to buy 25 shares at X = $1100/share; LM Co. sell a warrant with the same features.

Oil Well Increases in Value • Oil Well increases in value to $120,000, causing LM stock to go to $1200. • Call Exercised: • When Investor E exercises, shareholder D will simply turn over his 25 shares for $1100/share. • Exercising has no impact on the value of LM. • IVc = $1200-$1100 = $100.

Warrant Exercised • When E exercises warrant, the LM Co. will have to print 25 new shares (Nw) and sell them to E at X = $1100/share. • The company will receive cash, but the number of shares will increase: • 100 to 125 shares (dilution) • ($1100) (25) = $27,500 • In this case, the exercise of the warrant lowers the value of the stock from $1200 to $1180.

Warrant Value Stock and Warrant Values:

Warrant and Call Relation • Relation: The value of the warrant is equal to the value of the call times the dilution factor:

Rights • Definition: A right is call option issued by a corporation to existing shareholders, giving the holder the right to buy new shares at a specified price (subscription price). • Corporations use rights to ensure they adhere to preemptive rights. • A right is like a warrant: when it is exercised, new shares are created and the company receives cash.