Basic Accounting

Basic Accounting. Learning Objectives: Review financial statement analysis Read & interpret basic financial statements Analyze typical business transactions using balance sheet equation. Chapter 1 – 3 (Warren et al.). User Decisions. Accounting: Information Process. Identification

Basic Accounting

E N D

Presentation Transcript

Basic Accounting • Learning Objectives: • Review financial statement analysis • Read & interpret basic financial statements • Analyze typical business transactions using balance sheet equation Chapter 1 – 3 (Warren et al.)

User Decisions Accounting: Information Process Identification of Users User Information Needs Economic Data and Activities Accounting System Reports

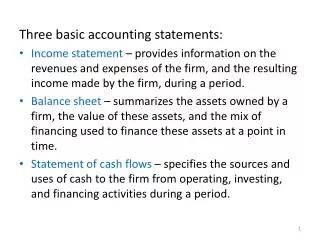

The Need for Accounting Managers, investors, and other internal groups want the answers to two important questions: How well did the organization perform? Major Financial Statements _______________ Where does the organization stand? _______________

Balance Sheet Also called statement offinancial position or statement of financialcondition ___________________________________________________ Month / quarter Income Statement ______________________________________ Match its accomplishments and its efforts ___________________ Financial Statements

Balance SheetAccounting Equation Resources = Sources Resources supplied by creditors and owners Cost of resources used in the business

Assets • Physical items (tangible) or rights (intangible) that have value and that are owned by the business entity • Can be converted into cash or used in operations ________________ • Cash • Account receivable • Inventory • Prepaid expense • Prepaid insurance • Supplies • _____________ • Tangible asset • Depreciation • _____________ • Goodwill

__________________ Account payable Accrued liabilities / accrued expenses Income taxes payable Current portion of long-term debt Unearned revenue / Deferred revenue ________________________ Secured debt Unsecured debt Liabilities • Debts owed to outsiders (creditors) • Item with the word “___________”

______________ Stockholder (owner) investments Owner’s Equity(shareholder’s equity, capital, net worth) • The owners’ equity in a corporation • The owner’s ____________________________ • __________________________________ • Reinvested earnings • Generated from operations +

OWNER’S EQUITY decreased by increased by Owner’s withdrawals Owner’s investments Effects of Transactions on Owner’s Equity Profits (earnings or income)

Revenues Increases in owner’s equity as a result of business and professional activities that earn income Revenues must be earned and realized Expense Decreases in ownership claims arising from delivering goods or services or using up assets Assets used up or services consumed in the process of generating revenues Revenues vs Expense Profits (or earnings or income) excess of revenues over expenses

PAID-IN CAPITAL RETAINED EARNING ASSET LIABILITIES + = + Balance SheetAccounting Equation PAID-IN CAPITAL ASSET LIABILITIES + - = +

Accrual Basis / Cash Basis __________________ • Exact timing of cash receipts and disbursements __________________ • Recognizes impact of transactions • Cash not necessarily changes hands • Match revenues and expenses • Record revenues when earned • Record expenses when incurred

Income Statement • Show a company’s ability to produce long-run earnings and dividends • Summarizes revenue and expense • Matching the company’s “accomplishments” and “efforts” • Revenue – Expenses Key Items

Ex 1: King’s Hardware’s Transaction in March 2004(Adapted from Horngren et al. 2002) • Initial investment by owners, $100,000 in cash • Acquisition of inventory for $75,000 in cash • Acquisition of inventory on open account $35,000 • Merchandise carried in inventory at a cost of $100,000 was sold on open account for $120,000 • Cash collection of account receivable, $30,000 • Cash payment of account payable, $10,000 • On March 1, King Hardware paid $3,000 cash for rent for March, April, and May. Required: • Prepare an analysis of King’s Hardware’s transaction in March • Prepare a balance sheet as of March 31, 2004 and an income statement for the month of March 2004 (ignore income tax)

Ex 2: Analysis of Transaction(Adapted from Warren et al., 2002) Jameson, Attorney-at-Law, is a proprietorship owned and operated by Cecil Jameson. On July 1 on the current year, C. J. has the following assets and liabilities: cash, $1000; account receivable, $3200; supplies, $850; land, $10,000; accounts payable, $1530. Office space and equipment are currently being rented, pending the construction of an office complex on land purchased last year.

Business Transaction of Jameson (Ex 2, continue) • Received cash from clients for services, $3928 • Paid creditors on account, $1055 • Additional investment from C.J. $3700 in cash • Paid office rent for the month, $1200 • Charged clients on account, $2025 • Purchase office supplies on account, $245 • Received cash from clients on account, $3000 • Received invoice for paralegal service (to be paid on August 10), $1635 • Paid the following expenses: wages, $850; service, $250; Utilities, $325; Miscellaneous, $75 • Determined that the cost of office supplies on hand was $980 • C.J. withdrew $1000 in cash from the business for personal use • Determine the amount of owner’s equity (C.J.’s capital) as of July 1. • Analyze each transaction using the balance sheet equation • Prepare an income statement of July

T-AccountAccount Adjustment • Learning Objectives: • Relate the measurement of expenses to the expiration of assets Chapter 2 -3 (Warren et al.)

T account Right Side Give CREDIT Left Side Receive DEBIT Date Description Debit Credit Double Entry AccountingT Account Scale or Balance • Double-entry accounting is based on a simple concept: each party in a business transaction will receive something and give something in return. In bookkeeping terms, what is received is a debit and what is given is a credit. • The T account is a representation of a scale or balance • General journal Receive DEBIT Give CREDIT

Account Adjustment • Under the accrual basis of accounting, adjustments are used to record implicittransactions, in contrast to the explicittransactions that trigger nearly all day-to-day routine entries. • Adjustments are generally prepared by the accountant at month or year end.

Adjustments: Deferrals and Accruals Revenues Current Period Future Period Unearned revenues Deferrals Cash Received Cash Received Revenue Recorded Accruals Revenue Recorded Cash Received Accrued revenues Expenses Current Period Future Period Prepaid expenses Deferrals Cash Paid Cash Paid Expense Recorded Accrued liability Expense Recorded Cash Paid Accruals

Type 1: Deferred Expenses (Prepaid expenses) • Asset that becomes an expense in future periods • Inventory • Prepaid rent and other prepaid expense • Equipment • Some services are acquired and used up instantaneously, e.g., advertisement service • Theoretically, it is an unexpired cost • 2 steps of analysis (1) Acquire advertising service (2) Use advertising service • When assets expire become expense asset & owner’s equity are decreased • Example: Newspaper advertising was acquired for $1000 cash. To follow the acquisition-expiration sequence, there are 2 steps of analysis:

Type 2: Deferred Revenues (unearned revenues) • Liability created by receiving cash in advance of providing goods or services. • Advanced collection • magazine subscription, • rent (landlord’s view) • How do “Prepaid Expense (type I)” and “Unearned Revenue (type II)” relate?

Type 3: Accrued Expenses (Accrued Liabilities) • Services are paid for after the service has been performed • Wages of employees • Interest (in borrower’s view) • Another type of liability • Ex: Wage payment of King’s Hardware

Type 4: Accrued Revenues (Accrued Assets) • Mirror image of Type 3 • Interest in lender’s view

Ex 3: Transaction Analysis of King Hardware during April, 2003(adapted from Horngren, 2002) Balances of March 31 Beginning balance for April • Cash collection of accounts receivable, $88,000 • Cash payments of account payable, $24,000 • Acquisition of inventory on open account, $80,000 • Merchandise carried in inventory at a cost of $70,000 was sold on open account for $85,000 • Adjustment for recognition of rent expense for April • Some customers paid $3,000 in advance for merchandise that they ordered but KH did not expect to deliver until May • Total wages of $6000 were paid on 4 Fridays in April. • KH incurred wages of $600 near the end of April, but it did not pay the employees till after April 30. • Cash dividends of $18,000 disbursed to stockholders on April 29