Download

1 / 17

E N D

Question 1, Case A (Part 1) The case „Saint-Gobain“ was about a French company having a PE in Germany that held participations in foreign companies incl. companies in non-EU member states. As Germany granted the participation exemption only in tax treaties the PE was not entitled to this participation exemption. A PE is not a (independent) person and cannot invoke treaty benefits. The court decided that the French company was discriminated. The freedom of establishment ensures that each European company may freely choose which business form they use for doing business abroad. If the French company was a Russian company the letter was not entitled to the benefits of the EC-Treaty. Russia is not a EU Member State. The ECJ would not be involved, the court has to rule about the interpretation of European law that is not subject to the case.

Question 1, Case A (Part 2) • However, the discrimination clause of the treaty between Germany and Russia could lead to the same result (see Article 24 (3) OECD Model). Paras 49 and 50 of the Commentary on Article 24, however, show that there are different opinions about this issue and the outcome will, therefore, be dependent on the interpretation made by the court in question. • If the Russian company was willing to go to court it would have to bring the case to the Russian court that is responsible for this kind of cases.

Question 1, Case B (Part 1) • Treaty between Brazil and Germany? • Treaty entitlement (Article 1 OECD Model) of the partnership? Partnership is well a person („body of persons“) in terms of Article 3(1)(a) but it is not resident in terms of Article 4(1) since it is not subject to tax. • Treaty does not apply! • (If Brazil considered the partnership a company the partnership would be treaty entitled to the treaty with Germany; Brazil would apply the the rate stipulated by that treaty; however, according to the OECD Commentary (para 6.3 on Article 1) Brazil should take into account the tax treatment in the state of the partnership (actually the domestic rate would apply because there is no treaty anymore; this only for information purposes))

Question 1, Case B (Part 2) • Treaty between Brazil and Austria/Netherlands? If a partnership is fiscally transparent the partners are taxed with the respective income and therefore the partners are treaty entitled (para 5 Commentary on Article 1). Brazil will apply the treaties with Austria and the Netherlands. • However, the partnership forms a PE of the partners in Germany. According to the treaties between A/NL and Germany the profits of the partnership (incl. the royalty income if attributable to the PE) are taxable in Germany (Article 7 OECD Model). Therefore the income will be taxable in Germany, Germany has to avoid the double taxation (WHT Brazil) on basis of the discrimination clauses in the treaties between A/NL and Germany.

Question 2 A ECJ’s Case Law on Double Taxation • The ECJ has held that juridical double taxation is not precluded by EU law. In it’s case law, the ECJ argues that, in the absence of Community measures for the avoidance of double taxation, it is the exclusive competence of the Member States to determine the connecting factors for taxation. • In Gilly (para. 17) for example, the ECJ held that Article 293 EC has no direct effect. • In Kerkhaert/Morres the ECJ reaffirmed its point of view (1/2 p.). The ECJ stated that the double taxation in the case followed from the parallel execution of taxing competence by the Member States (para. 20).

Question 2 B • In Cassis de Dijon the ECJ drew a distinction between measures in breach of Article 28 which were indistinctly applicable as opposed to distinctly applicable. Indistinctly applicable measures are ones that, prima facie, do not favour domestic producers over importers, and whose effects are equal on both. The ECJ argued that indistinctly applicable measures that favoured domestic traders over importers were not necessarily in breach of Article 28. They could be justified if they satisfied 'mandatory' requirements - namely that the measure is necessary for protecting the public or the consumer. The rule of reason is essentially the proposition that a proportionality exercise must be performed by the Court to determine whether the effects of Member State legislation on the free movement of goods is justified in light of the legislation's stated goals. • This proportionality exercise has itself been applied by the ECJ further than the boundaries of Article 28 would initially allow.

Question 2 C Article 23A(4) • Article 23A(4) avoids double non-taxation in cases of differences in interpretation of the DTC between the Contracting States. • It concerns cases where the source state interprets the DTC to the effect it has no tax jurisdiction on an item of income, the resident state interprets it to the effect that the source state is allocated jurisdiction for which the resident state should give double tax relief. • In that case the resident state is not obliged to provide double tax relief for that item of income on basis of Article 23A(1).

Question 2 C - example • State S regards a business activity of a company resident in R on the territory of S NOT to constitute a PE (Art. 5), whereas State R DOES and exempts a part of the business income income (Art. 7 & 23A). • On basis of Art. 23(4), State R may reverse the exemption.

Question 3, Part 1 • Has Nor-Corp a PE in Australia? • In principle not because there is no place of business, a helicopter is not fixed (Article 5(1) OECD Model) • However, the helicopter was leased to A-Corp. • According to the commentary on Article 5 (para. 8) industrial equipment (a part of a complete form; as the helicopter is an entirety there could be doubts whether it may be considered equipment) may be considered a PE if • There is a place of business used for leasing activities – here no place of business; or • If the activity goes beyond mere leasing, i.e. the supplied personnel has wider responsibilities than operation or maintenance – here no wider responsibilities – no PE

Question 3, Part 2 • Olafson works 96 days in Australia for an existing PE • Principle: taxation in state of work (Article 15(1)) • Exception: taxation in state of residence (Article 15(2) if salary born by the PE • Two different opinions • As the salary is cost attributable to the PE (Article 7 OECD Model), it should be deductible in Australia and therefore subject to tax in Australia (see para 7 Commentary on Article 15) • If the costs are not covered by the PE (bookkeeping) the salary is not born by the PE (wording; argument used by a New Zealand Court)

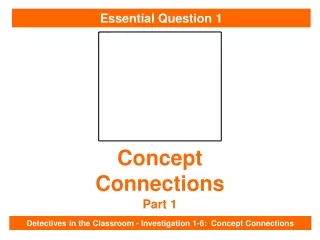

Question 4 Netherlands ALFA Profit Share (3) 25 % Germany BETA Interest (2) Dividend (1) 100% GAMMA France

Question 4 • DTC law • AD 1. DTC Germany-France, beneficial owner is a company resident of Germany and the paying company is a resident of France; On basis of article 10(3) the payment qualifies (autonomously) as a dividend (income from shares). On basis of article 10(2)(a), France is allowed to apply a 5% WHT. • AD 2. DTC Netherlands-France, beneficial owner is a company resident of the Netherlands and the paying company is a resident of France. The 2% interest payment qualifies (autonomously ) as an interest payment on basis of art. 11(3). On basis of art. 11(2), France is allowed to apply a 10% WHT.

Question 4 • Qualification of the loan arrangement • “Hybrid Bond”, i.e. an optional convertible profit sharing bond.

Question 4 DTC law (cont.) • One first has to resort to the ordinary meaning of art. 10(3) and 11(3) that links to the underlying legal relation, respectively ‘corporate right’ and ‘debt claim of any kind’. The payment should be qualified as interest, since the legal relation is under the title ‘debt claim’ and art. 11(3) explicitly includes profit sharing and convertible bonds. • Secondly, it reads in COMM. Art. 11, para. 19, (also COMM. Art. 10, para. 25) that in exceptional circumstances a presumed interest payment should be qualified as a dividend, because the specific conditions in the individual loan arrangement effect that the debt claimant effectively shares the risks run in the debtor.

Question 4 DTC Law (cont.) • Furthermore, the COMM. Art. 10, para. 25 provides certain conditions. [ANALYZE!] • The profit share payment should for DTC purposes be qualified as interest. • Thirdly, In extreme cases of doubt, one could by force of Art. 3(2) and 10(3) resort to French law and consider that French law regards (part of) the payment a dividend payment. (corporate right definition) • ALFA does not hold directly a minimum holding of 10%, so art. 10(2)(b): 15% WHT • Depending on the qualification, either a 15% (dividend) or a 10% (interest) WHT is allowed.

Question 4 EU Law • AD 1. The Parent-Subsidiary Directive clearly applies. On basis of Art. 5 PSD, France may not levy a WHT on the payment. • AD 2. The Interest/Royalty Directive clearly does not apply to this holding relation, see Art. 3(b) since there is no direct holding. • AD 3. The Interest/Royalty Direct clearly does not apply, Art. 3(b) and 4(1)(a), (b), and (c). The PSD could apply, if the payment can be qualified as a ‘distribution of profit’. However, the PSD does not cover payments where the beneficial owner has no direct holding in the paying company. EU law does not limit the French WHT.

Question 4 Conclusion • AD 1. No WHT allowed on basis of PSD, as EU law overrides the DTC based WHT. • AD 2. A DTC based WHT of 10% is allowed. • AD 3. A DTC based WHT of either 10% (interest) or 15% (dividends) is allowed.