Download

1 / 41

410 likes | 588 Views

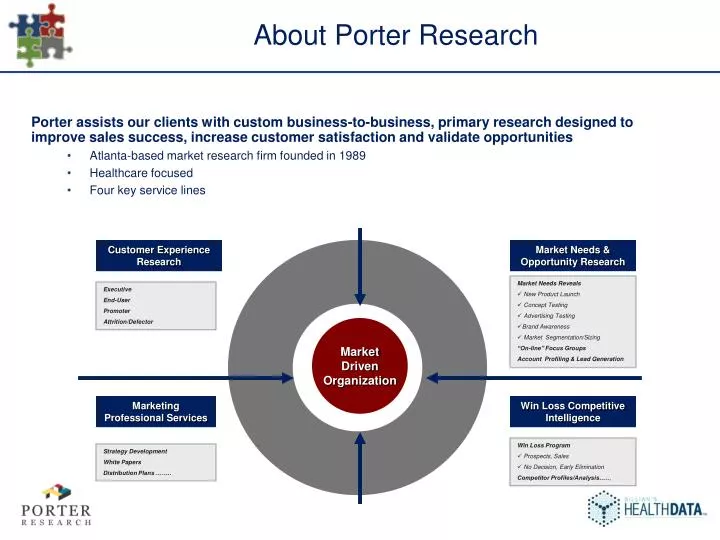

About Porter Research. Porter assists our clients with custom business-to-business, primary research designed to improve sales success, increase customer satisfaction and validate opportunities Atlanta-based market research firm founded in 1989 Healthcare focused Four key service lines.

E N D

About Porter Research • Porter assists our clients with custom business-to-business, primary research designed to improve sales success, increase customer satisfaction and validate opportunities • Atlanta-based market research firm founded in 1989 • Healthcare focused • Four key service lines Customer Experience Research Market Needs & Opportunity Research • Market Needs Reveals • New Product Launch • Concept Testing • Advertising Testing • Brand Awareness • Market Segmentation/Sizing “On-line” Focus Groups Account Profiling & Lead Generation Executive End-User Promoter Attrition/Defector Market Driven Organization Marketing Professional Services Win Loss Competitive Intelligence • Win Loss Program • Prospects, Sales • No Decision, Early Elimination Competitor Profiles/Analysis…… Strategy Development White Papers Distribution Plans ……..

"[Health] Information should follow the patient, and artificial obstacles – technical, business related, bureaucratic – should not get in the way." Dr. Blumenthal

About the Research Porter Research and Billian’s HealthDATA fielded a primary market research program aimed at understanding providers’ perceptions of the Health Information Exchange (HIE) movement • Web-based survey designed by Porter Research • Fielded October 2010 • Select titles targeted and pulled from Billian HealthDATA’s 150,000+ database of hospital decision makers • More than 120 respondents • Participating organizations represent critical access to multi-facility systems and IDNs • Respondents were typically at a C- (54%) or Director-level (21%) within their organization • Functionally, most participants had Information Technology (39%), Medical/Clinical (15%), or Finance (13%) responsibilities

HITECH Transforming Healthcare • Goals: • Quality • Efficiency • Safety • Equity • Business Transformation: • Movement toward outcome-based vs. transaction-based reimbursement • Reengineering of business models to facilitate risk sharing of outcomes-based healthcare

New Business Model? “Is your organization considering moving to one of the new business models below to support healthcare reform? Select all apply…” • Overall, 43% of facilities are considering moving to an Accountable Care Organization model • The Patient Centered Medical Home model is being considered by 34% • Single Hospital facilities are significantly less likely to consider a change, specifically to the Patient Centered Medical home model

Challenge – Meeting Long Term Exchange Demands NHIN Regional/ State

HIE – Primary Strategic Initiative “Which of the following best summarizes your organization's primary strategic initiative as it relates to health information exchange?” • Nearly half of all respondents indicate their primary strategic initiative is “to improve connectivity within the health system” • Approximately 30% stated that their focus extends beyond the health system • There is no significant difference in the responses based on organization size

Current State – “Simple” • Focus is on connectivity of information systems, primarily within their own health system

Current State – “Transitioning” • Focus shifts to sharing data with entities external to the health system, primarily within the community Transitioning 37%

Current State – “Complex” • Focus begins to shift to true coordinated care with the implementation of an HIE central repository/ clearinghouse

HIE Today - Internally “Considering organizations internal to your health system, with whom does your organization exchange information with today?” • Most organizations are exchanging with Labs, Imaging, and Physician Practices Within the Health System • Multi-hospital orgs were significantly more likely to exchange with Post Acute Care Facilities, Pharmacies, Physician Practices Within the Health System, and Other Organization Types

HIE Today & Tomorrow - Externally “With whom does your organization exchange information with today that would be considered external (i.e., not affiliated) to your health system? With whom does your organization want to exchange with in the future?” • Today, the most common exchange partners are Physician Practices External to the Health System and Labs (i.e., Reference) • 86% of respondents believe they’ll be exchanging data with physician practices external to the hospital in the future.

HIE Today - Externally “What type of data are you exchanging? Please select all that apply...” • Hospital Lab Results and Radiology Results/Reports Sent to Physician Practices or Other Providers were both mentioned by more than 70% of respondents • Multi-hospital facilities were significantly more likely to claim exchanging Patient Summaries, Orders, Lab and Radiology Results

Barriers/ Challenges “What are the greatest barriers and/or challenges perceived by your organization regarding implementing HIE solutions in the care process?” • When asked top-of-mind, costs were significantly more likely to be cited • There is little to no discernable difference between multi/ single hospital systems

Top Concern “Of the following, what is your top concern?” • Respondents were asked to select one of thirteen possible responses • Again, Cost/ Funding emerged as the top concern, selected by 46% • In this instance, single-hospital facilities were significantly more likely to select cost/ funding

HIE Benefits “What does your organization perceive to be the tangible benefits of health information exchange (HIE)?” • Most respondents –57% - believe HIE will bring Improved Quality/ Care • Other areas of benefit include Administrative/ Clinical Efficiencies and generic Access to Information • Multi-hospital organizations were significantly more likely to provide Administrative/ Clinical Efficiencies as a response

HIE Benefactor “In your opinion, who do you believe benefits most from health information exchange (HIE) and a more comprehensive view of a patient’s health status provided across care settings?” • Most respondents – 63% – believe the Patient benefits most • 16% believe the Community at Large is the benefactor • Only 4% selected the Health System

HIE Funding “How should health information exchange technologies and services be funded? Please select all that apply…” • Nearly two-thirds of respondents believe that the Federal Government should provide funding • Single-hospital organizations were significantly more likely to select the Federal Government or Unsure; Providers (Hospitals/ Health Systems) was significantly more likely to be cited by multi-hospital organizations

Preferred Data Architecture “In your opinion what is the preferred data architecture for health information exchange for your organization?” • The Centralized data warehouse model is most preferred at 27% • 21% of respondents were unsure, although this was significantly more common among single hospital organizations

Comprehensive View of Patient’s Health Status “Do you see achievement of a more comprehensive view of the patient’s status for Health Information Exchange initiatives as an essential element to your organization meeting the requirements highlighted within the HITECH Act?” • Overall, 74% responded positively • Multi-hospital organizations were significantly more likely to select Yes

Role of Traditional Integration Tools “Do you believe traditional integration tools (i.e., interface engine) can achieve the HIE requirements for the following stages of Meaningful Use?” • While just over half of respondents believe traditional integration tools can meet Stage 1 requirements, only 26% believe they’ll meet requirements determined for Stage 2-3 • Multi-hospital orgs are significantly more likely to believe traditional integration tools will meet Stage 1 requirements and not meet Stage 2-3 requirements

Meaningful Use Preparedness –HIE Requirements “On a scale from 1 (“Have Not Started”) to 5 (“Fully Prepared”), how would you rate your organization in terms of preparedness for the HIE requirements of Meaningful Use in the following stages?” • While nearly half rated themselves as mostly prepared (4 or 5) for Stage 1 requirements, less than ten percent believe they’re prepared to meet requirements determined for Stage 2-3 • Overall, multi-hospital organizations tend to rate themselves only slightly higher than single-hospital organizations 23% Unprepared for Stage 1 65% Unprepared for Stage 2-3

HIE Investment to Date “Has your organization made any purchases of technology solutions that facilitate the health information exchange (HIE) process?” • Overall, 61% indicated they have made investments in technology to facilitate the health information exchange process • Single-hospital systems responded negatively 35% of the time, compared 25% for multi-hospital organizations

Detailed HIE Investment – To Date/ Planned “For each of the following types of health information exchange technologies, please indicate your timeframe to purchase.”

Detailed HIE Investment – To Date/ Planned “For each of the following types of health information exchange technologies, please indicate your timeframe to purchase.”

Detailed HIE Investment – To Date/ Planned “For each of the following types of health information exchange technologies, please indicate your timeframe to purchase.”

Vendors in Consideration “What vendors will your organization consider for future purchases of health information exchange technology? Select all that apply...” • Overall, just over 40% of respondents were “Unsure” • However, single hospital organizations were considerably more likely to respond “Unsure” • Epic – the most mentioned single vendor – was significantly more common among multi-hospital systems 40% 25% 19% 14% 14% 9% 8% 8% 7% 7% 7% 5% 4%

Perceived Market Leaders “Who do you consider to be the market leader among vendors that provide health information exchange technologies?” • Again, no clear leader has emerged, with nearly half of all respondents indicating that they are “Unsure” 48% 9% 8% 7% 7% 6% 4% 3% 3% 2% 2% 2%

Vendor Attributes “What are the key attributes you will look for in a vendor when selecting health information exchange technology solutions for your hospital or health system?” • The most common attribute mentioned was Costs/ Value at 43% • Costs/ Value was also significantly more common to single hospital systems, as was Service/ Support

Preferred Supplier Type – HIE Technologies “What type of organization would you like to obtain health information exchange (HIE) capabilities/technologies from? Please check all that apply...” • The most common response, “A Vendor Solely Focused on Delivering Interoperability Solutions,” was cited by just over one-third of respondents • Also significant: “Current Acute Care EHR Vendor” and “Unsure”

In Summary • “Wide variety” of perceptionsin the market of what defines HIE • Focus on HIE today is internally within the health system, shifting to external entities in the future • HIE is perceived as a critical piece of the puzzleto achieving MU requirements • The majority of providers feel prepared in achieving Stage 1 HIE requirements (50%) while (65%) feel unprepared for Stage 2 and 3 requirements • Providers see the greatest barrierto adoption as cost /funding – sustainability • No clear market leaderin this space - emerging • Providers preferto acquire their HIE technologies either from a sole provider or their EHR vendor

Tift Regional Medical Center - Profile • With a reputation as an innovative provider of quality care, Tift Regional Medical Center (TRMC) is a not-for-profit, 191-bed regional hospital serving 12 counties in South Central Georgia. Located in Tifton, the hospital’s medical staff includes more than 95 physicians with the majority board-certified in over 30 specialties. • Tift Regional provides a wide-range of services, including six Centers of Excellence offering advanced, expert care in oncology, cardiology, neurology, surgery, women's health and emergency medicine.

Tift Regional's HIE Journey to Date Data Exchanged Today In 2007 Tift Regional Medical Center began an IT initiative to share data with a large multi-specialty physician practice in the community. . This collaboration resulted in hospital patient results (lab and radiology) being shared with the physicians – populating their respective EMRs

Tift Regional’s HIE - Initial Steps Initial Steps in Data Exchange Focused on hybrid registration process. HIE technology intercepts all order requisitions to a web work que. Patients are pre-registered into the hospital ADT solution – for Lab and Radiology orders based on this que and matching occurs. Signed physician orders for lab and radiology tests are sent electronically to the hospital documentation system to become part of the medical record. Results for lab and radiology tests performed at the hospital are sent to the practice and populate the AllScripts EMR TouchWorks for viewing.

Tift Regional’s HIE Plan for the “Future” Future Steps in Data Exchange Focus on solidifying exchange within the health system Implementation of a comprehensive enterprise MPI solution, as well as, improved integration between Allscripts and McKesson’s Horizon solutions. Exchange patient data within the medical community of Tifton. - Exchange data with other physician affiliated (non-owned) Exchange of patient and quality data within an Accountable Care Organization (ACO) that will extend beyond Tifton. Exchange data with a statewide Georgia HIE.

Common Barriers/Challenges Lack of Common Definitions What is an HIE? There are different meanings and understandings. Some think interfaces are all that is required, some think an HIE is a patient portal, still others see HIE as something else. Vendors even describe an HIE differently. We need to all speak the same language with the same purpose. Growing need for more robust eMPI solutions Matching a patient across one or two organizations is no longer satisfactory. We need to make sure the same patient matches throughout an organization, an ACO and an HIE Integration and Interfaces Many of today’s healthcare IT vendors are stuck 10 years in the past. Interfaces between hospital systems and physician EMRs are challenging and vendors are reluctant to cooperate in developing outbound clinical interfaces to other entities.

Common Barriers/Challenges Security Meeting HIPAA mandates while sharing PHI with other entities will require investment in robust security measures. Cost Health systems are struggling with managing to higher IT costs and reduced reimbursements. HIE expenses could be formidable. Who will foot the bill? Is and HIE model sustainable?

Healthcare Reform HIE: A Critical Piece of the Puzzle