Download

1 / 15

150 likes | 311 Views

Association of Government Accountants Corporate Partners Advisory Group. CPAG Research Project Financial Analysis Pilot Proof of Concept. Department of the Treasury Fiscal Service Enterprise Data Warehouse November 2, 2009. CPAG Research Project

E N D

Association of Government Accountants Corporate Partners Advisory Group CPAG Research Project Financial Analysis Pilot Proof of Concept Department of the Treasury Fiscal Service Enterprise Data Warehouse November 2, 2009

CPAG Research Project Fiscal Assistant Secretary MeetingNovember 2009 – 2:00pm – 3:30pm Agenda • Introduction of Attendees – Jerry Murphy • CPAG Project Overview – Jerry Murphy • Demonstration Overview - Netezza • System Demonstration – Cognos • Questions and Answers – Jerry Murphy • Conclusions – Next Steps – Jerry Murphy

CPAG Research Project Objectives • Develop an Internet based Monthly Treasury Statement and Combined Statement that offers users access to an Enterprise Data Warehouse and analytical tools to develop interactive queries of Treasury “Official” financial data supporting the Government’s Surplus or Deficit and other related data, e.g., performance, population, employment, geographic, congressional district, etc. to develop performance and other metrics for identifying results and to assist the decision process. • Provide a reconciliation of Federal Expenditure/Outlay data between the Treasury and the American Recovery and Reinvestment Act expenditure/outlay data. • Provide a reconciliation of Federal Expenditures/Outlay data between the Treasury and the Economic Emergency Recovery Act, Troubled Asset Relief Programexpenditure/outlay data. • Provide a consolidated report of Federal Expenditures/Outlay data identifying: • Total Federal Expenditures/Outlays • Federal Funding Accountability and Transparency Act Expenditure/Outlay data. • Economic Emergency Recovery Act, Troubled Asset Relief Program Expenditure/Outlay data. • American Recovery and Reinvestment Act Expenditure/Outlay data.

31USCSec. 3513. Financial reporting and accounting system • The Secretary of the Treasury shall prepare reports that will inform the President, Congress, and the public on the financial operations of the United States Government. The reports shall include financial information the President requires. The head of ach executive agency shall give the Secretary reports and information on the financial conditions and operations of the agency the Secretary requires to prepare the reports. • The Secretary may – • establish facilities necessary to prepare the reports; and • reorganize the accounting functions and procedures and financial reports of the Department of the Treasury to develop an effective and coordinated system of accounting and financial reporting in the Department that will integrate the accounting results for the Department and be the operating center for consolidating accounting results of other executive agencies with accounting results of the Department. Authority Article 1, Section 9, Clause 7 of the US Constitution & 31USC3513a US Constitution, Article I, Section 9, Clause (7) No Money shall be drawn from the Treasury, but in Consequence of Appropriations made by Law; and a regular Statement and Account of the Receipts and Expenditures of all public Money shall be published from time to time.

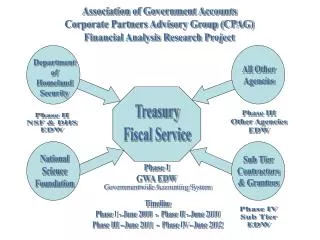

Association of Government AccountantsCorporate Partners Advisory Group (CPAG)Financial Analysis Research ProjectEnterprise Data Warehouse Overview DepartmentofHomelandSecurity All OtherAgencies TreasuryFiscal Service Phase IIIOther AgenciesEDW Phase IINSF & DHSEDW GWAGovernmentwideAccounting SystemEnterprise DataWarehouse (EDW) NationalScienceFoundation Sub TierContractors& Grantees Phase IGWA EDW Timeline Phase I – June 2010 - Phase II – June 2010Phase III – June 2011 - Phase IV – June 2012 Phase IVSub TierEDW

Association of Government Accountants - CPAG Research ProjectDepartment of the Treasury - Fiscal Service Enterprise Data Warehouse – Financial Analysis – Pilot Proof of Concept Project Organization

Association of Government Accountants Corporate Partners Advisory Group CPAG Research Project Financial Analysis Pilot Proof of Concept Timeline Department of the Treasury Fiscal Service Enterprise Data Warehouse November 2, 2009

S. 2590 109TH CONGRESS 2D SESSION S. 2590 AN ACT To require full disclosure of all entities and organizations receiving Federal funds. 1 Be it enacted by the Senate and House of Representa2 tives of the United States of America in Congress assembled, 3 SECTION 1. SHORT TITLE. 4 This Act may be cited as the ‘‘Federal Funding Ac 5 countability and Transparency Act of 2006’’.

Public Law 109–282 109th Congress An Act To require full disclosure of all entities and organizations receiving Federal funds. Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled, SECTION 1. SHORT TITLE. This Act may be cited as the ‘‘Federal Funding Accountability and Transparency Act of 2006’’. SEC. 2. FULL DISCLOSURE OF ENTITIES RECEIVING FEDERAL FUNDING. (a) DEFINITIONS.—In this section: (1) ENTITY.—The term ‘‘entity’’— (A) includes, whether for profit or nonprofit— (i) A corporation; (ii) an association; (iii) a partnership; (iv) a limited liability company; (v) a limited liability partnership; (vi) a sole proprietorship; (vii) any other legal business entity; (viii) any other grantee or contractor that is not excluded by subparagraph (B) or (C); and (ix) any State or locality; (B) on and after January 1, 2009, includes any subcontractor or subgrantee; and (C) does not include— (i) an individual recipient of Federal assistance; or (ii) a Federal employee. (2) FEDERAL AWARD.—The term ‘‘Federal award’’— (A) means Federal financial assistance and expenditures that— (i) include grants, subgrants, loans, awards, cooperative agreements, and other forms of financial assistance; (ii) include contracts, subcontracts, purchase orders, task orders, and delivery orders; (B) does not include individual transactions below $25,000; and (C) before October 1, 2008, does not include credit card transactions. (3) SEARCHABLE WEBSITE.—The term ‘‘searchable website’’ means a website that allows the public to—

Sunday, July 27,2008 1 – 2:10 p.m. S102: Federal Funding Accountability and Transparency Act— Implementation Perspectives Julie Basile, Senior Policy Analyst, Office of Federal Procurement Policy, U.S. Office of Management and Budget Mark A. Forman, Principal, KPMG LLP Melinda B. Morgan, Director, Finance Staff, Justice Management Division, U.S. Department of Justice Moderator: Andrea Brandon, Deputy Administrator, Cooperative State Research, Education and Extension Service, U.S. Department of Agriculture A discussion of implementation perspectives related to the Federal Funding Accountability and Transparency Act of 2006 (FFATA). The law was enacted with the purpose of increasing “transparency and accountability of federal government expenditures by providing Wednesday, June 30, 2008 11 a.m. – 12:15 p.m. W117: Beyond Financial Reporting—Financial Analytics Linda M. Combs, Controller, U.S. Office of Management and Budget Mark A. Forman, Principal, KPMG LLP Melinda B. Morgan, Director, Finance Staff, Justice Management Division, U.S. Department of Justice The panel discusses federal financial management strategic opportunities regarding information management and the use of business analytics. Business analytics helps to answer the more complex business questions that are required to accurately drive strategy and execution. As an ongoing process, analytics continually increase knowledge, based on the expanding historic information gathered in today's data warehouses.

PUBLIC LAW 110–343—OCT. 3, 2008 122 STAT. 3765 • Public Law 110–343 • 110th Congress • An Act • To provide authority for the Federal Government to purchase and insure • Certain types of troubled assets for the purposes of providing stability to and preventing disruption in the economy and financial system and protecting taxpayers, to amend the Internal Revenue Code of 1986 to provide incentives for energy production and conservation, to extend certain expiring provisions, to provide individual income tax relief, and for other purposes. • Be it enacted by the Senate and House of Representatives of • the United States of America in Congress assembled, • DIVISION A—EMERGENCY ECONOMIC • STABILIZATION • SECTION 1. SHORT TITLE AND TABLE OF CONTENTS. • (a) SHORT TITLE.—This division may be cited as the ‘‘Emergency • Economic Stabilization Act of 2008’’. • (b) TABLE OF CONTENTS.—The table of contents for this division • is as follows: • Sec. 1. Short title and table of contents. • Sec. 2. Purposes. • Sec. 3. Definitions. • TITLE I—TROUBLED ASSETS RELIEF PROGRAM • Sec. 101. Purchases of troubled assets. • Sec. 102. Insurance of troubled assets. • Sec. 103. Considerations. • Sec. 104. Financial Stability Oversight Board. • Sec. 105. Reports. • Sec. 106. Rights; management; sale of troubled assets; revenues and sale proceeds. • Sec. 107. Contracting procedures. • Sec. 108. Conflicts of interest. • Sec. 109. Foreclosure mitigation efforts. • Sec. 110. Assistance to homeowners. • Sec. 111. Executive compensation and corporate governance. • Sec. 112. Coordination with foreign authorities and central banks. • Sec. 113. Minimization of long-term costs and maximization of benefits for taxpayers. • Sec. 114. Market transparency. • Sec. 115. Graduated authorization to purchase. • Sec. 116. Oversight and audits.

PUBLIC LAW 111–5—FEB. 17, 2009 123 STAT. 115 • Public Law 111–5 • 111th Congress • An Act • Making supplemental appropriations for job preservation and creation, • infrastructure Investment, energy efficiency and science, assistance to the unemployed, and State and local fiscal stabilization, for the fiscal year ending September 30, 2009, and for other purposes. • Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled, • SECTION 1. SHORT TITLE. • This Act may be cited as the ‘‘American Recovery and Reinvestment • Act of 2009’’. • SEC. 2. TABLE OF CONTENTS. • The table of contents for this Act is as follows: • DIVISION A—APPROPRIATIONS PROVISIONS • TITLE I—AGRICULTURE, RURAL DEVELOPMENT, FOOD AND • DRUG ADMINISTRATION, AND RELATED AGENCIES • TITLE II—COMMERCE, JUSTICE, SCIENCE, AND RELATED • AGENCIES • TITLE III—DEPARTMENT OF DEFENSE • TITLE IV—ENERGY AND WATER DEVELOPMENT • TITLE V—FINANCIAL SERVICES AND GENERAL GOVERNMENT • TITLE VI—DEPARTMENT OF HOMELAND SECURITY • TITLE VII—INTERIOR, ENVIRONMENT, AND RELATED AGENCIES • TITLE VIII—DEPARTMENTS OF LABOR, HEALTH AND HUMAN • SERVICES, AND EDUCATION, AND RELATED AGENCIES • TITLE IX—LEGISLATIVE BRANCH • TITLE X—MILITARY CONSTRUCTION AND VETERANS AFFAIRS • AND RELATEDAGENCIES • TITLE XI—STATE, FOREIGN OPERATIONS, AND RELATED • PROGRAMS • TITLE XII—TRANSPORTATION, HOUSING AND URBAN • DEVELOPMENT, ANDRELATED AGENCIES • TITLE XIII—HEALTH INFORMATION TECHNOLOGY • TITLE XIV—STATE FISCAL STABILIZATION FUND • TITLE XV—ACCOUNTABILITY AND TRANSPARENCY • TITLE XVI—GENERAL PROVISIONS—THIS ACT • DIVISION B—TAX, UNEMPLOYMENT, HEALTH, STATE FISCAL RELIEF, ANDOTHER PROVISIONS • TITLE I—TAX PROVISIONS

Monday, June 22, 2009 10:30 – 11:45 a.m.M104: Treasury Fiscal Service, Strategic Financial Management Direction and PlansMarriott: Balconies L – N Scott Bell, MBA, CGFM, Senior Accountant, Financial Management Services, U.S. Department of the TreasuryCarrie Hug, MS, CGFM, CPA, U.S. Department of the TreasuryJames Sturgill, Assistant Commissioner, Financial Management Service, U.S. Department of TreasuryModerator: Jeff Bateman, Vice President, Strategic Programs and Alliances, Teradata Government Systems, LLC This session explores the strategic plans of the Department of the Treasury, Fiscal Service, related to the next generation of financial management and debt management initiatives. Monday June 22, 2009 4:10 – 5:20 p.m.M121: Predictive Analytics—How to Stop Problems Before They BeginMarriott: Balconies L – N Jeff Lovett, Director, Finance and Performance Management, Teradata CorporationRussell Walker, Ph.D., Assistant Director of the Zell Center for Risk Research, Kellogg School of Management, Northwestern UniversityModerator: David R. Bennett, CGFM, CPA, Finance Director, Blount County Government, Blount County, TN; AGA Immediate Past National Treasurer and Member, AGA National Executive Committee This session is designed for the business or technical manager who oversees a business intelligence environment and wishes to learn the best practices and pitfalls of implementing a predictive analytics capability. While panelists discuss some technical issues, the session is designed to educate business managers about how to drive greater value from their existing investments in data warehousing and information delivery systems. Tuesday, June 23, 2009 10:50 a.m. – NoonT108: Accountability and Transparency in Government—FFATA, EESA/TARP, and ARRA Requirements and Private Sector PerspectivesMarriott: Gallery 3 Thomas N. Cooley, Chief Financial Officer, National Science FoundationDavid S. Ehrlich, CISA, Audit Analyst, Thomson ReutersHagen F. Feuchter, Senior Industry Consultant Risk Management and Financial Services, Teradata Government Systems, LLCModerator: Tim Spadafore, Vice President, Integrated Business Consulting A discussion of the impact of the FFATA PL 109-282 and EESA TARP PL 110-343 legislation will have on accountability and transparency relating to financial reporting for the federal, state and local governments, and the private sector