Download

1 / 32

320 likes | 341 Views

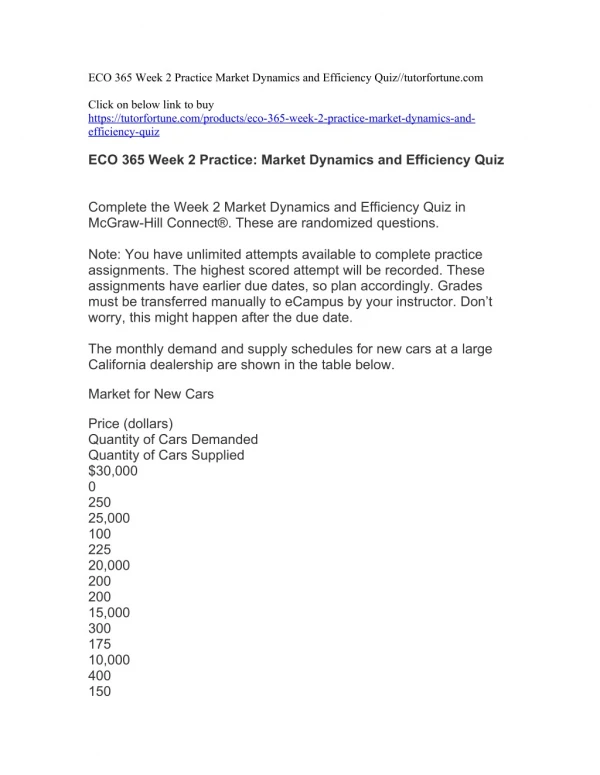

ECO 365 Week 2 Practice Market Dynamics and Efficiency Quiz//tutorfortune.com<br><br>Click on below link to buy<br>https://tutorfortune.com/products/eco-365-week-2-practice-market-dynamics-and-efficiency-quiz<br><br>ECO 365 Week 2 Practice: Market Dynamics and Efficiency Quiz<br> <br><br>Complete the Week 2 Market Dynamics and Efficiency Quiz in McGraw-Hill Connectu00ae. These are randomized questions. <br><br> <br><br>Multiple Choice<br><br> <br><br>excludable.<br><br>nonrival in consumption.<br><br> <br><br>rival in consumption.<br><br>nonexcludable<br>ECO 365 Week 2 Practice: Market Dynamics and Efficiency Quiz<br>.<br>Click on below link to buy<br>https://tutorfortune.com/products/eco-365-week-2-practice-market-dynamics-and-efficiency-quiz<br>

E N D

ECO 365 Week 2 Practice Market Dynamics and Efficiency Quiz//tutorfortune.com Click on below link to buy https://tutorfortune.com/products/eco-365-week-2-practice-market-dynamics-and- efficiency-quiz ECO 365 Week 2 Practice: Market Dynamics and Efficiency Quiz Complete the Week 2 Market Dynamics and Efficiency Quiz in McGraw-Hill Connect®. These are randomized questions. Note: You have unlimited attempts available to complete practice assignments. The highest scored attempt will be recorded. These assignments have earlier due dates, so plan accordingly. Grades must be transferred manually to eCampus by your instructor. Don’t worry, this might happen after the due date. The monthly demand and supply schedules for new cars at a large California dealership are shown in the table below. Market for New Cars Price (dollars) Quantity of Cars Demanded Quantity of Cars Supplied $30,000 0 250 25,000 100 225 20,000 200 200 15,000 300 175 10,000 400 150

If the dealership is currently charging $25,000 for a new car, at the end of the month there will be: a shortage of 125 cars. a surplus of 5,000 cars. a surplus of 125 cars. a shortage of 5,000 cars. neither a surplus nor a shortage; the market will be in equilibrium. The demand and supply schedules for sunscreen at a small beach are shown below. Market for Sunscreen Price (dollars per bottle) Quantity of Sunscreen Demanded (bottles) Quantity of Sunscreen Supplied (bottles) $35 1,000 8,500 30 2,000 7,000 25 3,000 5,500 20 4,000 4,000 15 5,000 2,500 10

6,000 1,000 Instructions: Enter your answers as a whole number. If the price is $15 per bottle, how many bottles of sunscreen are demanded and supplied? Qd = Qs = In this case, there would be upward pressure on the price. What is the equilibrium price and quantity in the market for sunscreen? P = Q = Use the following graph for the milk market to answer the question below. There would be excess production of milk whenever the price is Multiple Choice greater than $1.50 per gallon. greater but not less than $2.00 per gallon. less than $1.50 per gallon. less but not greater than $2.00 per gallon. There is a surplus in a market for a product when

Multiple Choice quantity demanded is less than quantity supplied. demand is less than supply. the current price is lower than the equilibrium price. quantity demanded is greater than quantity supplied. Use the following table to answer the question below. Price per Unit Quantity Demanded per Year Quantity Supplied per Year $5 2,000 0 10 1,800 300 15 1,600 600 20 1,400 900 25 1,200 1,200 30 1,000 1,500 There will be a shortage whenever the price is Multiple Choice

equals $25. higher than $25. higher than $30. lower than $25. A decrease in demand and an increase in supply will Multiple Choice decrease price and affect the equilibrium quantity in an indeterminate way. decrease price and increase the equilibrium quantity. increase price and affect the equilibrium quantity in an indeterminate way. affect price in an indeterminate way and decrease the equilibrium quantity. There is an excess demand in a market for a product when Multiple Choice quantity demanded is greater than quantity supplied. supply is less than demand. the current price is higher than the equilibrium price. quantity demanded is less than quantity supplied. In competitive markets, surpluses or shortages will

Multiple Choice cause shifts in the demand and supply curves that tend to eliminate the excess production or excess demand. cause changes in the quantities demanded and supplied that tend to intensify the excess production or excess demand. never exist because the markets are always at equilibrium. cause changes in the quantities demanded and supplied that tend to eliminate the excess production or excess demand. There is a shortage in a market for a product when Multiple Choice quantity demanded is lower than quantity supplied. supply is less than demand. demand is less than supply. the current price is lower than the equilibrium price. Which of the following is an example of a price ceiling? Multiple Choice Price supports for agricultural products.

Subsidies for apartment rent in major cities. Limits on interest rates charged by credit card companies. Minimum-wage laws for unskilled workers. Assume that the graphs show a competitive market for the product stated in the question. Select the graph above that best shows the change in the market for leather coats when leather coats become more fashionable among young consumers. Multiple Choice graph (1) graph (4) graph (3) graph (2) In competitive markets, a surplus or shortage will Multiple Choice never exist because the markets are always at equilibrium.

cause changes in the quantities demanded and supplied that tend to cause changes in the quantities demanded and supplied that tend to eliminate the surplus or shortage. cause changes in the quantities demanded and supplied that tend to intensify the surplus or shortage. cause shifts in the demand and supply curves that tend to eliminate the surplus or shortage. Use the following graph for the milk market to answer the question below. In this market, the equilibrium price is ____ and equilibrium quantity is ___ Multiple Choice $1.50 per gallon; 28 million gallons. $1.50 per gallon; 30 million gallons. $1.00 per gallon; 35 million gallons. $28 per gallon; 150 million gallons. Use the following table to answer the question below. Price per Unit Quantity Demanded per Year Quantity Supplied per Year $5 2,000

0 10 1,800 300 15 1,600 600 20 1,400 900 25 1,200 1,200 30 1,000 1,500 In this competitive market, the price and quantity will settle at Multiple Choice $20 and 900 units. $25 and 1,200 units. $15 and 1,600 units. $10 and 1,800 units. The additional benefit of producing one more roast beef sandwich at a local deli is $2. The additional cost of producing one more roast beef sandwich is $3. To improve allocative efficiency: producers should produce at least one more roast beef sandwich because MB MC.

producers should produce at least one more roast beef sandwich producers should produce at least one more roast beef sandwich because MC MB. producers should not produce one more roast beef sandwich because MB MC. producers should not produce one more roast beef sandwich because MC MB. The value that consumers get (from consuming a product) over and above what they actually paid for the product is called Multiple Choice consumer surplus. consumer utility. consumption expenditures. consumer demand. Consumer surplus Multiple Choice is the difference between the maximum price consumers are willing to pay for a product and the lower equilibrium price. is the difference between the minimum price producers are willing to accept for a product and the higher equilibrium price. is the difference between the maximum price consumers are willing to

pay for a product and the minimum price producers are willing to pay for a product and the minimum price producers are willing to accept. rises as equilibrium price rises. Charlie is willing to pay $10 for a T-shirt that is priced at $9. If Charlie buys the T-shirt, then his consumer surplus is Multiple Choice $19. $1. $90. $0.90. If the equilibrium wage for fast-food restaurants is $8 and the government enforces a minimum wage of $15 Multiple Choice workers will be able to find more jobs. overall, society will be better off. workers will get paid less. fast-food restaurants will hire fewer workers.

The market supply curve indicates the Multiple Choice total revenues that sellers would receive from selling various quantities of the product. minimum acceptable prices that sellers are willing to accept for the product. maximum prices that buyers are willing and able to pay for the product. total amount that buyers will pay in buying a given quantity of the product. Charlie is willing to pay $10 for a T-shirt that is priced at $9. If Charlie buys the T-shirt, then his consumer surplus is

Multiple Choice $90. $1. $19. $0.90. Graphically, producer surplus is measured as the area Multiple Choice under the demand curve and below the actual price. above the supply curve and below the actual price. under the demand curve and above the actual price. above the supply curve and above the actual price.

Allocative efficiency occurs only at that output where Multiple Choice the combined amounts of consumer surplus and producer surplus are maximized. consumer surplus exceeds producer surplus by the greatest amount. marginal benefit exceeds marginal cost by the greatest amount. the areas of consumer and producer surplus are equal. A producer’s minimum acceptable price for a particular unit of a good Multiple Choice

must cover the wages, rent, and interest payments necessary to produce the good but need not include profit. equals the marginal cost of producing that particular unit. is the same for all units of the good. will, for most units produced, equal the maximum that consumers are willing to pay for the good. Productive efficiency occurs at the point where Multiple Choice the production technique minimizes economic surplus. the production technique minimizes cost. marginal benefit exceeds marginal cost by the greatest amount. consumer surplus exceeds producer surplus by the greatest amount.

The minimum acceptable price for a product that producer Sam is willing to receive is $15. The price he could get for the product in the market is $18. How much is Sam’s producer surplus? Multiple Choice $45 $3 $270 $33 The difference between the maximum price a consumer is willing to pay for a product and the actual price the consumer pays is called

Multiple Choice market failure. consumer surplus. consumer demand. utility. Consumer surplus arises in a market because Multiple Choice the market price is higher than what some consumers are willing to pay for the product. at the current market price, quantity supplied is greater than quantity demanded. at the current market price, quantity demanded is greater than quantity supplied.

the market price is below what some consumers are willing to pay for the market price is below what some consumers are willing to pay for the product. The difference between the actual price that a producer receives and the minimum acceptable price the producer is willing to accept is called the producer Multiple Choice revenues. surplus. costs. utility.

In the market for a particular pair of shoes, Jena is willing to pay $75 for a pair while Jane is willing to pay $85 for a pair. The actual price that each has to pay for a pair of shoes is $65. What is the combined amount of consumer surplus for Jena and Jane? Multiple Choice $130. $215. $30. $10. Producer surplus Multiple Choice is the difference between the maximum price consumers are willing to

pay for a product and the lower equilibrium price. rises as equilibrium price falls. is the difference between the maximum price consumers are willing to pay for a product and the minimum price producers are willing to accept. is the difference between the minimum price producers are willing to accept for a product and the higher equilibrium price. The production of paper often creates a waste product that pollutes waterways. Assume the producer of paper does not directly pay to dispose of the waste in the water. In this case, the price of paper will be below the socially efficient price and the amount of paper produced will be above the socially efficient amount. Which of the following goods is nonrival? A visit to the doctor at her office A soccer match in a stadium A pizza at a pizza parlor

A tuna in the ocean Which of the following goods is both nonrival and nonexcludable? A hot dog at a hot dog stand A soccer match in a stadium The light from a lighthouse at a harbor entrance A tuna in the ocean Texarkana Electric Company burns coal to heat the water that drives its electricity-producing turbines. The table below shows the marginal benefit of annual electricity consumption and the private marginal cost of annual electricity production. Marginal Cost and Marginal Benefit Quantity (millions of megawatts) MBprivate MCprivate MCexternal MCsocial 1.0 $145 $85 $ 20 $ 105 2.0 130 90 20 110 3.0 115 95

20 115 4.0 100 100 20 120 5.0 85 105 20 125 6.0 60 110 20 130 Instructions: Enter your answers as a whole number. What is the (apparent) optimal amount of electricity for Texarkana Electric Company to produce each year? 4 million megawatts per year Now assume the production of each million megawatts of electricity also produces sulfur dioxide (a precursor to acid rain). The external cost of the sulfur dioxide is $20 per million megawatts of electricity production. Fill in the external marginal cost (MCexternal) and the social marginal cost (MCsocial) columns in the table above. What is the socially optimal amount of electricity for Texarkana to produce if all costs and benefits are considered? 3 million megawatts per year

If electricity production triggers an external cost of sulfur dioxide of If electricity production triggers an external cost of sulfur dioxide of $20 per million megawatts, these external costs need to be added to private marginal cost in order to measure social marginal cost. When Texarkana Electric Company produces 3.0 million megawatts per year, an optimum for society is reached because social marginal benefit equals social marginal cost. If some activity creates external benefits as well as private benefits, then economic theory suggests that the activity ought to be Multiple Choice left alone. taxed. prohibited. subsidized. Where there are spillover (or external) benefits from having a particular product in a society, the government can make the quantity of the product approach the socially optimal level by doing the following except Multiple Choice

subsidizing the sellers of the product. providing the product itself. taxing the sellers of the product. subsidizing the buyers of the product. External benefits in consumption refer to benefits accruing to those Multiple Choice who are consuming the product abroad. who bought and consumed the product. who are selling the product to the consumers. other than the ones who consumed the product.

When the production of a good generates external costs, a firm’s private supply curve will be Multiple Choice vertical. horizontal. to the left of the social supply curve. to the right of the social supply curve. A negative externality or spillover cost (additional social cost) occurs when Multiple Choice the price of the good exceeds the marginal cost of producing it.

firms fail to achieve allocative efficiency. firms fail to achieve productive efficiency. the total cost of producing a good exceeds the costs borne by the producer. If there are external benefits associated with the consumption of a good or service Multiple Choice the private demand curve will overestimate the true demand curve. consumers will be willing to pay for all these benefits in private markets. the market demand curve will be the vertical summation of the individual demand costs. the private demand curve will underestimate the true demand curve.

A public good Multiple Choice is available to all and cannot be denied to anyone. produces no positive or negative externalities. can be profitably produced by private firms. is characterized by rivalry and excludability. If a good that generates negative externalities were priced to take these negative externalities into account, its Multiple Choice price would remain constant and output would increase. price would increase, and its output would decrease.

price would decrease, and its output would increase. price would increase but its output would remain constant. Use the following supply and demand graph for product X to answer the question below. What would happen if the government taxed the producers of this product because it has negative externalities in production? Multiple Choice supply would decrease demand would decrease supply would increase price would decrease

A positive externality or spillover benefit (additional social benefit) occurs when Multiple Choice a firm does not bear all of the costs of producing a good or service. product differentiation increases the variety of products available to consumers. firms earn positive economic profits. the benefits associated with a product exceed those that accrue for consumers. What are the two characteristics that differentiate private goods from public goods? Multiple Choice

marginal cost and marginal benefit rivalry and excludability ownership and usage negative externality and positive externality A public good Multiple Choice can never be provided by a nongovernmental organization. generally results in substantial negative externalities. costs essentially nothing to produce and is thus provided by the government at a zero price. cannot be provided to one person without making it available to others as well.

The two main characteristics of a public good are Multiple Choice production at constant marginal cost and rising demand. nonrivalry and large negative externalities. nonexcludability and production at rising marginal cost. nonrivalry and nonexcludability. If the consumption of a product or service involves external benefits, then the government can improve efficiency in the market by Multiple Choice imposing a ive tax to for an overallocation of resources. providing a subsidy to for an overallocation of resources. imposing a ive tax to for an underallocation of resources. providing a subsidy to for an underallocation of resources. If one person’s consumption of a good does not preclude another’s consumption, the good is said to be

Multiple Choice excludable. nonrival in consumption. rival in consumption. nonexcludable ECO 365 Week 2 Practice: Market Dynamics and Efficiency Quiz . Click on below link to buy https://tutorfortune.com/products/eco-365-week-2-practice-market-dynamics-and- efficiency-quiz