Download

1 / 105

1.16k likes | 1.84k Views

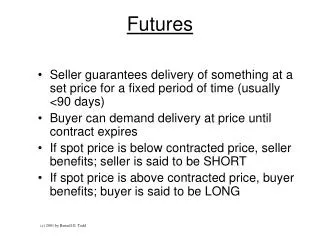

Futures. Futures Contract. A future contract is an agreement between to parties to buy or sell an asset at a certain time in future for a certain price. The buyer of the contract, who is said to be long the contract has agreed to buy (take delivery of) the goods in future.

E N D

Futures Contract • A future contract is an agreement between to parties to buy or sell an asset at a certain time in future for a certain price. • The buyer of the contract, who is said to be long the contract has agreed to buy (take delivery of) the goods in future. • The seller is said to be short the contract and has obligation to sell (deliver) the goods in the future.

0 55 60 65 Payoff for a buyer of Futures Profit/Loss Spot price

0 55 60 65 Payoff for a seller of Futures Profit/Loss Spot price

Futures Market in India • Stock index futures launched on 12th June, 2000 and stock futures in 9th Nov, 2001. • Futures on Stock Index and on individual stocks • NSE: S&P CNX Nifty Futures, CNXIT Futures, BANK Nifty,CNX 100, CNX IT,CNX Nifty Junior, Nifty Midcap 50, futures on 207 individual stocks • Commodity futures • Currency futures • Interest rate futures • NSE: Notional T – Bills, Notional 10 year bonds (coupon bearing and non-coupon bearing)

Futures Contract • Exchange traded products. • A standardized, transferable, exchange-traded contract that requires delivery of a commodity, bond, currency, or stock index, at a specified price, on a specified future date.

Forwards vs. Futures • A futures contract is like a forward contract: • Both specify that a certain commodity will be exchanged for another at a specified time in the future at prices specified today. • They represent zero net supply; for every buyer there is a seller. • Profit-loss profile realized in forwards and futures represent a zero sum game.

Forwards vs. Futures • A futures contract is different from a forward: • Futures are standardized; only the price in negotiated: e.g. all December 2004 gold futures contracts are identical in that the amount of gold (contract size), quality of gold, delivery date and place of delivery are specified. Forwards are customized and all the aspects can be negotiated.

Forwards vs. Futures • Offesetting (prior to delivery date) a trade is possible in futures market while it is non-existent in most of the forward markets. For example, if you are long Dec 2004 gold futures contract you can close that position by later selling a Dec 2004 gold futures contract. • Default risk is least in case of futures. Since forward contracts are agreements between the two parties, each part face the counterparty default risk.

Forwards vs. Futures • Most future positions are eventually offset and in many cases they are cash settled. In contrast, most forward contracts terminate with delivery of the specified good. • Margins and daily marking to market in case of futures.

Futures Contract: Standard Features • Contract specification • Asset type • Exchange stipulates the grade of the asset. • Contract size • Specifies the amount of the asset to be delivered under one contract. • Delivery agreement • The place of delivery

Futures Contract: Standard Features • Delivery months • Futures are referred to by their delivery months. • Price quotes • Daily price movement limits • Daily price movement limits, termed as limit move (limit up and limit down) • Position limits • Maximum number of contracts that a speculator may hold

Futures Contract: Standard Features • Clearing house • Clearinghouse of the exchange becomes the opposite party to both buyers and sellers - thus guarantees the performance of the parties to each transaction. • Margin requirement • When two parties trade a futures contract, the futures exchange requires some good faith money (security) from both, to act as a guarantee.

Futures Contract: Standard Features • Initial Margin • Each exchange is responsible for setting the minimum initial margin requirements. The initial margin is the amount a trader must deposit into his trading account (also called as margin account) when establishing a position. • Exchanges use SPAN (Standard Portfolio Analysis of Risk) to establish initial margin requirement.

Futures Contract: Standard Features • Beyond the initial margin, if the equity in the account falls below a maintenance margin level, additional funds must be deposited to bring the account back up to the initial margin level. The process is known as margin call. The amount that is to be deposited is termed as variation margin. • Once a trader has received the margin call, he must meet the call, even if the price has moved in his favour.

Futures Contract: Standard Features • For example, if the initial margin required to trade per gold futures contract is $1000, and the maintenance margin level is $750, then an adverse change of $2.60/oz. will result in a margin call. Because one gold futures covers 100 oz. of gold a decline of $2.60/oz in the futures price will deplete the long position by $260. The trader with losses must deposit sufficient funds to bring the margin to the initial level of $1000. The margin that is deposited to meet margin call is termed as variation margin.

Futures Contract: Standard Features • Types of orders • Market order • Trade to be carried out immediately at the best price • Limit order • Specifies a particular price. The order can be executed only at this price or at one more favouarble to the investor. • Stop order or stop-loss order • Also specifies a particular price. The order is executed at the best available price once a bid or offer is made at a particular price or a less favorable price.

Futures Contract: Standard Features • Stop-limit order • A combination of stop order and limit order. • Market-if-touched order • They are like limit orders, except that they become market orders once a trade has occurred at the specified price. • Discretionary order/Market-not-held order • Traded as a market order except that execution may be delayed at the broker's discretion in an attempt to get a better price.

Futures Contract: Standard Features • Time orders • Unless specified, an order is a day order and expires at the end of the trading day. Good-till-cancelled remains active till executed or cancelled by the customer. Some other time orders are Good-this-week, Good-this-month etc. • Spread order • Specifies two trades that must be filled together. The order can specify a difference in the prices or it can be a market order.

Futures Contract: Standard Features • Offsetting the positions (squaring up) • Most traders choose to close out their position prior to delivery period specified in the contract by entering into the opposite type of the trade. • Open Interest • Total number of contracts outstanding for a particular delivery month. • Open interest is a good proxy for demand for a contract.

Futures Contract: Standard Features • Settlement • Physical settlement vs. Cash settlement • Settlement month • Settlement price

Futures Contract: Standard Features • Marking to Market • All futures traders’ positions are marked to market daily. • Also known as daily resettlement. It means everyday, profits are added to, or losses are deducted from the trader’s account. • Profits and losses are based on the changes in the settlement prices or closing futures prices.

Futures Contract: Standard Features • Marked to Market: An example • In NSE all future contracts are marked to market to the daily settlement price. The profit loss are computed as thus: • The trade price and the day’s settlement price for contracts executed during the day but not squared up • Previous’ days settlement price and the current day’s settlement price for brought forward contracts • Buy price and the sell price for contracts executed during the day and squared up

Futures Contract: Standard Features Source: NSE

Basis and Convergence • Basis and convergence explain the relationship between futures price and cash price. • Basis • Spot price (cash price) minus the futures price • In a normal market basis will be negative; since future prices exceed spot prices and it is positive in an inverted market. • Basis approaches zero as the delivery month is approached.

Basis and Convergence • The process of basis moving towards zero is termed as convergence. Why does it happen? • It is due to arbitrage. For example, if future price is above spot price during the delivery period, the trader can • Short a futures contract • Buy the asset • Make delivery

Pricing Futures • Do the quoted prices reflect true value of the underlying index? • Does there exist any opportunity for arbitrage? • Why should the basis be negative in normal markets? The dynamics lies in the Cost-of-carry model.

Cost of Carry Model • Cost of carry measures the storage cost, plus the interest that is paid to finance the asset less the income earned on the asset. • Cost of carry varies across the assets. • For a non-dividend paying stock, the cost of carry is the risk free rate because there are no storage costs and no income is earned. • For a commodity, storage cost is important.

Cost of Carry Model • The fair value of futures incorporates the ‘no-arbitrage’ limits on the prices. This is as thus F = S + CC - CR • F = Future prices • S = Spot price • CC = Holding costs or carry costs. • CR = Carry returns

Cost of Carry Model • For the stock index futures it can be mentioned as H(0,T) = rT/365, where r is the annual interest rate, T is the number of days until delivery date and [FV(divs)] is the future value of all dividends paid by the component of the stock index

Cost of Carry Model • If • traders will engage in a cash-and-carry arbitrage which calls for buying the spot index (it is relatively cheap) , ‘carrying‘ it, and selling the futures (relatively expensive). • If • Traders will engage in a reverse cash-and-carry arbitrage which calls for buying the futures and selling the spot, and investing the proceeds.

Normal Backwardation and Contango • Normal backwardation • Futures prices are below expected future spot prices, and futures price is expected to rise as the delivery date approaches • Contango • A contango exists wherever the futures price lies above the expected future spot price, and the futures price generally declines as the delivery date nears.

Synthetic Stock and T Bills • Buying a stock index futures contract and buying Treasury bills is frequently called a long synthetic stock position. • Buying shares of stock that replicates an index and also selling a futures contract on the stock creates a synthetic treasury bill.

Synthetic Stock • Illustration • An investor owns $9,523,800 in one year T-bills which will be worth $10 million one year hence. • Take long position in stock index futures with an underlying value equal to $9,523,800 (based on spot index). • Suppose that index futures price is 1375 and the spot is at 1325 and the futures contract multiplier is 250.

Synthetic Stock • 28.7511 futures will be purchased ($9,523,800/1325*250 ) • Now suppose after one year spot price and futures price are at 1500. The value of the portfolio is • $10 million from T bills • $898,472 in stock index futures profit (125 × 250 × 28.7511) • Gain is 14.434%, given that investor began the year with $9,523,800

Synthetic Stock • The 14.434% is identical to the return from buying actual stocks, ignoring transaction costs. • The capital appreciation on the stock was 13.208%. (1500-1325/1325) • Had he purchased the stocks he would have received the dividends and interest on those dividends, and this dividend yield component would have been 1.2264%. • Total return is 14.434%

Synthetic T bill • The arbitrageur buys the stock and locks in a selling price by selling futures contract. • When performing a cash-and-carry arbitrage, the synthetic T-bill is created by borrowing at a lower rate and lending at a higher rate, which is risk less.

Hedging with Futures • Hedgers use futures market to reduce a particular risk that they face. • A perfect hedge is one that completely eliminates the risk. In practice, these are rare. • When is the short futures position appropriate? • When is a long futures position appropriate? • Which futures contract should be used? • What is the optimal size of the futures position?

Hedging: The Basic Principle • The objective is usually to take a position that neutralizes the risk as far as possible. • Consider an investor who will gain Rs.10,000 for each rupee increase in the price of the commodity over the next three months and lose Rs.10,000 for each rupee decrease in the price during the same period. To hedge, the investor should take a short futures position that is designed to offset the risk.

Hedging with Futures • Short hedge • Involves a short position in futures contract. • Appropriate when the hedger has already owned the asset and expects to sell it in future. • Can also be used when an asset is not owned right now but will be owned at some time in future.

Hedging with Futures • Short hedge illustration • On May 15, 2004 an oil produces negotiated a contract to sell 1 million barrels of crude oil. It has been argued that price that will apply in the contract is the market price on August 15. The oil producer is therefore in the position where it will gain $10,000 for each cent increase in the price and lose $10,000 for each cent decrease in the price.

Hedging with Futures • Suppose that spot price on May 15 is $19 per barrel and August crude oil futures price is $18.75 per barrel. Each futures contract involves the delivery of 1000 barrels. • The company can hedge by shorting 1000 August futures contracts. • If the oil producer closes out his position on August 15, the effect of the strategy should be to lock in a price close to $18.75 per barrel.

Hedging with Futures • Long hedge • Long positions in a futures contract • More appropriate when one needs to purchase a certain asset in the future and wants to lock in a price now.

Hedging with Futures • Long hedge illustration • On January 15 a copper fabricator knows it will require 100,000 pounds of copper on May 15 to meet certain contracts. The spot price of the copper is 140 cents per pound, and the May futures are priced at 120 cents per pound. Each contract is for the delivery of 25,000 pounds of copper. • The fabricator can hedge his position by taking a long position in four May futures contract.

Hedging with Stock Index Futures • Long security – Short index futures • Every buy position on a security is simultaneously a buy position on the index. • As a way out a long position on a security can be accompanied by sale of index futures. • One needs to know the beta of a security.

Hedging with Stock Index Futures • Illustration • Shyam adopts a position of Rs.1 million LONG MTNL on date 5th June 2001. He plans to hold the position till the 25th. • Suppose the beta of MTNL happens to be 1.2. • Hence he needs a short position of Rs.1.2 million on the index futures market to totally remove his Nifty exposure.

Hedging with Stock Index Futures • On date 5th June 2001, Nifty is 980 and the nearest futures contract (with expiration 28th June 2001) is trading at about 1000. Hence, each market lot of the futures (200 nifties) is worth Rs.200,000. To sell Rs.1.2 million of Nifty, we need to sell 6 lots (by rounding off to the nearest market lot). • He sells 6 market lots of Nifty (1200 nifties) to get the position: LONG MTNL Rs.1,000,000 SHORT NIFTY Rs.1,200,000

Hedging with Stock Index Futures • 10 days later, Nifty crashed because of instability in the government. • On Thursday, Shyam unwound both positions. His position on MTNL lost Rs.120,000 since MTNL had dropped to 880,000. His short position on Nifty June futures earned Rs.141,600. Overall, he earned Rs.21,600.

Hedging with Stock Index Futures • Short security – Long index futures • Every sell position on a security is a simultaneous sell position on the index. • A short position on a security must be accompanied by a long position on the index futures. • A knowledge of beta is essential.