Download

1 / 16

160 likes | 297 Views

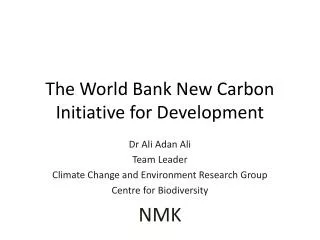

World Bank Carbon Finance Experience, Strategy and New Funds. Workshop – How to develop CDM projects in Central America, March 27-28, 2003 Rodrigo Chaparro. $. $. Carbon Fund. 2. 2. Emission Reduction Purchase Agreement. Nature of Carbon Finance Projects. Investor. Banks. Equity.

E N D

World Bank Carbon Finance Experience, Strategy and New Funds Workshop – How to develop CDM projects in Central America, March 27-28, 2003 Rodrigo Chaparro

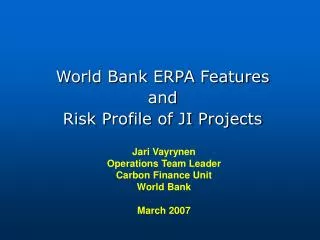

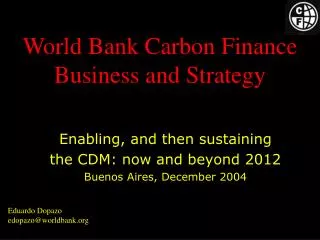

$ $ Carbon Fund 2 2 Emission Reduction Purchase Agreement Nature of Carbon Finance Projects Investor Banks Equity Debt Promote Sustainable development Power Purchase Agreement $$ $$ Main Product e.g: electricity Carbon Credits

Bank Carbon Finance BusinessFamily of Products • PCF as “flagship”: $180 million • Netherlands Clean Development Facility – CDM only, $30 million/year over 2002-2005 • Community Development Carbon Fund (CDCF): to start May/June 2003 at $40-50 million • BioCarbon Fund (BioCF): to start by Sept 2003 at $30-40 million • Climate Neutral Bank; starting March 12th

PCF Shareholders ($180 million) Public Sector(6) Governments of Netherlands, Finland, Sweden, Norway, Canada, and Japan Bank for International Cooperation Private Sector: (17) RWE - Germany, Gaz de France, Tokyo Electric Power, Deutsche Bank, Chubu Electric, Chugoku Electric, Kyushu Electric, Shikoku Electric, Tohoku Electric, Mitsui, Mitsubishi, Electrabel, NorskHydro- Norway, Statoil -Norway, BP, Fortum, RaboBank, NL

Bank’s Carbon Finance Business at a Glance • Value of Emissions Reductions Purchase Agreements (ERPAs) negotiated:15, $38m • Number and value of approved PCF projects: 28, $119.2m • Number and value of NDCF projects: 13, US$ 157.1m • Total estimated investment in 30 approved projects: US$ 1.081 billion

Most Important Findings • Regulatory uncertainty remains post-Marrakesh: • CDM Executive Board still to review and approve methods for carbon asset creation • No Entry into Force of Kyoto Protocol • CDM/JI Carbon Asset Creation remains complex and lengthy: lead times of 3-7 years for project design through delivery of first ERs. • Private Sector is not buying directly in CDM/JI on a significant scale • Capacity Building is Urgent • first carbon purchase in each country and sector is key to build awareness • Carbon finance and TA for capacity building must go hand in hand to support carbon market development • Small projects and hence smaller countries and poorer communities will lose out unless risks and costs are managed by intermediaries, despite streamlining • LULUCF – Sink Assets are high value to sustainable development but poorly understood and at risk as an asset class

Carbon Finance flows 2001-2002 Australia Canada Asia Africa USA Latin America Source: Authors’ own calculation, based on transaction database assembled with Natsource, Co2e.com and PointCarbon

Certifying Sustainable Development Outcomes • Bank has shown that it is feasible and cost effective to create and certify local environmental and community development benefits along with carbon • Examples from PCF: • Colombia Jepirachi Wind Power Plant (19MW) also certifies: • potable water, • electricity for schools/clinics and • small fishing port for local indigenous peoples; • Plantar Project in Brazil (23,400ha fuelwood plantation) also certifies: • Worker health improvement • ABRINQ certification of no child labor or exploitation • Biodiversity benefits • FSC certification of improved forest management

Carbon Asset Creation and Maintenance Manufacturing Process and Costs based on Bank experience Preparation and review of the Project Project completion • Upstream Due Diligence, carbon risk assessment and documentation: $ 40K 3 months Baseline Study and Monitoring and Verification Plan (MVP) Up to 21 years • Baseline : $20 K • Monitoring Plan: $20K Periodic verification & certification 2 months • Verification: $10-25 K • Supervision: $10-20K Validation process 1-3 years 2 months • Contract, Processing • and documentation: $30k 3 months Construction and start up Project Appraisal and Negotiation • Initial verification at start-up: $25K • Consultation and Project Appraisal: $105K • Negotiations and Legal documentation: $50K Total through Negotiations • All expenses: $265 K

World Bank Carbon Finance Strategy:Carbon Finance Beyond PCF • Expand Carbon Market Development • Provide First-of-a-kind opportunities: Introduce more countries and companies to carbon market • Benchmark carbon asset creation and Crowd-In private sector: Increase certainty and lower entry barriers • Expand access to CDM/JI assets in early market: Bank intermediation is critical to expand supply • Strengthen TA/Capacity Building • Demonstrate credible forestry/agriculture “sinks” activities • Open Markets for small projects and small countries: • Build Credibility in AAU Market:Greening of AAUs

Small projects are burdened by high transaction costs • Small and poorer countries will miss out on private sector carbon finance • Need special efforts to: • mitigate risk, bundle small transactions • standardize both CDM/JI requirements and business procedures

Carbon Sequestration has important rural development, poverty alleviation, sustainable natural resource management and global environment implications • PCF carbon sinks projects demonstrate how to create and certify biodiversity improvements and contributions to rural welfare, but PCF can only do 3-4 projects • Need dedicated fund to demonstrate and benchmark carbon sinks assets in support of sustainable agriculture and forestry, watershed management and biodiversity conservation.

Benchmarking and Securing Supply of High Quality ERs includes…. • Reducing Risk and Uncertainty in Supply: Preparing Standardized baselines/monitoring plans for replicable carbon projects which lower risk in carbon asset creation for host countries and buyers • Greening “Hot Air”:helping transition economies market their assigned amount units by helping design investment programs which utilize revenues from AAU sale to invest in clean technology to create actual emissions reductions

Carbon Finance Strategy: Summary • Respond to Host Country demand for carbon finance • Extend carbon finance to the smaller, poorer countries and rural communities • Demonstrate carbon finance for carbon sinks • Strengthen and expand capacity building for mitigation and adaptation • Explore practical arrangements for “greening” AAUs • FY03 business plan targets: • negotiated ERPAs, $155m (PCF on track; NCDF ahead); • cumulative approved projects for negotiation, $250m;

Benefits to New Funds Participants • High quality ERs for compliance and trading • Cheaper: expertise of established carbon finance team at incremental cost • Risk mitigation via diversification, hedge future costs • Knowledge of carbon asset creation, market intelligence: internships, training, advice • Marketing: Corporate social responsibility • Origination Options: Bring projects to fund • Parallel Purchase: Access to additional CO2e to grow carbon portfolios at low risk and effort