Download

1 / 14

150 likes | 296 Views

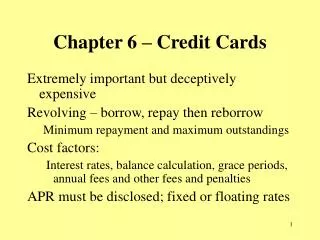

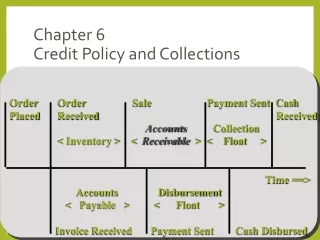

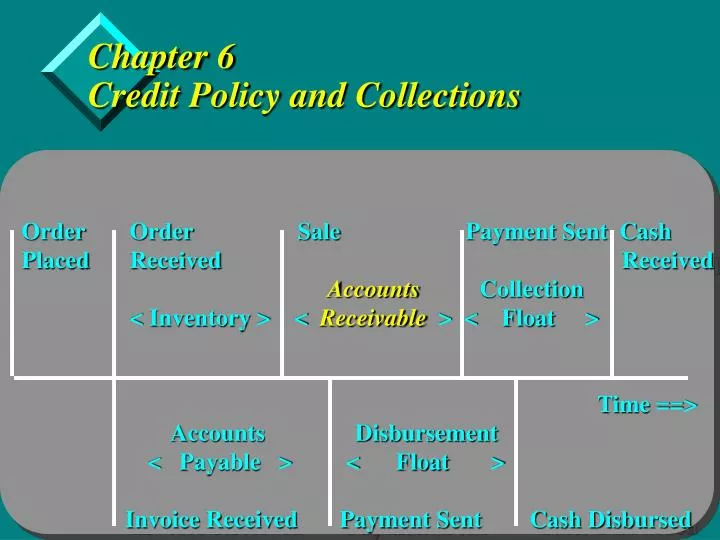

Chapter 6 Credit Policy and Collections. Order Order Sale Payment Sent Cash Placed Received Received Accounts Collection < Inventory > < Receivable > < Float >

E N D

Chapter 6Credit Policy and Collections • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

Objectives • Specify advantages of NPV in evaluating credit policy alternatives. • Calculate the NPV of alternative credit policies and select the best policy. • Identify the 3 major traditional measures of collection patterns, calculate them, and understand their flaws. • Calculate and interpret uncollected balance percentages and relate to traditional measures. • Describe present corporate credit policy practices. • List and explain the major differences encountered when extending credit internationally.

Evaluate Changes in Credit Policy • Credit term change decision variables • effect on dollar profits • sales effect • receivables effect • return on investment effect • 84% of credit executives believe they can estimate: • default probability • credit limits • opportunity cost of funds invested in receivables • company’s overall cost of capital

Incremental Profit vs NPV • Financial statement approach • Choose the alternative with the highest profits • Does not give value effect • NPV approach • Choose the alternative with the highest NPV • Directly measures value effect

Changing Credit Terms, EQ 6.1 ZN = [(1+g)SE](1-dN)PN(1-bN) / (1 + iDPN) PV discount pmts + [(1+g)SE](1-PN)(1-bN) / (1 + iCPN) PV non-discount pmts - VCR [(1+g)SE] Variable cost - EXPN[(1+g)SE] / (1 + iCPN) PV credit expense See page 196 for variable definitions

Changing Credit Terms, EQ 6.2 ZE = SE(1-dE)PE(1-bE) / (1 + iDPE) PV discount pmts + SE(1-PE)(1-bE) / (1 + iCPE) PV non-discount pmts - VCR (SE) PV variable cost pmts - EXPE SE / (1 + iCPE) PV credit expense pmts

Changing Credit Terms, EQ 6.3, 6.4 EQ 6.3 Z = ZN - ZE Decision Rule: IF Z > 0 then Accept policy change IF Z < 0 then Reject policy change EQ 6.4 NPV = Z / i

Monitoring Collections • Receivables turnover • least favored technique • Days sales outstanding, DSO • ranked almost as high as aging schedules • Aging schedules • ranked as most favored technique

Problem • All three traditional measures have a serious flaw • All three are influenced by sales trends • Choice of averaging period impact turnover and DSO • Increasing sales tends to: • improve aging schedules • worsen DSO and turnover

Solution • Uncollected Balance Percentage • Uncollected monthly receivables computed as a percent of the credit sales in the month they originated. • Compare trend through time

Collection Procedures • Typical collection effort • initial contact within 10 days of delinquency • then reminder letter followed by phone call • sales force notified • last resort, reference to collection agency/legal action • Collection agency • Phase 1 - computer generated collection letter, when accounts are 45 to 90 days past due • Phase 2 - commissioned collectors used • Companies tend to be more aggressive the larger the receivables balance • Companies understand the good-will tradeoff when selecting collection methods

Evaluating the Credit Department • Reducing investment in receivables • reduce invoice float • fine-tune credit administration and credit policy • outsourcing and automating • reduce discrepancies and deductions • improve monitoring and collections using benchmark data • Organizational integration and key account management • develop better understanding of needs and wants of key accounts • prioritize accounts by potential value • make credit terms and policies integral part of well designed sales and marketing offering

International Credit Management • Credit policy analysis • lengthening terms increases exchange rate risk • also increases default risk • harder to get D&B reports • harder to get bank credit information • Modifying monitoring and collections • legal remedies for late payment or nonpayment differ by country

Summary • This chapter developed the framework for applying the NPV model to credit policy decisions. • The NPV approach was applied to changes in credit standards, the credit period, cash discounts. • Traditional monitoring tools include aging, DSO and receivables turnover. • Improved monitoring measure • uncollected balance percentage • a reliable and unbiased measure of customer payment behavior • Collection procedures were reviewed. • The chapter concluded with a look at benchmarking and the impact of foreign sales.