Download

1 / 21

230 likes | 580 Views

Bond Portfolio Management. Five steps in investment management process Tracking Errors Active Portfolio Strategies Use of Leverage Indexing. Five Steps in Investment Management. Setting investment objectives Establishing Investment Policy

E N D

Bond Portfolio Management • Five steps in investment management process • Tracking Errors • Active Portfolio Strategies • Use of Leverage • Indexing

Five Steps in Investment Management Setting investment objectives Establishing Investment Policy (in cash equivalent, equities, fixed-income, real estate) Select a portfolio strategy (active, structured, or indexing) Select assets Measuring and evaluating performance (ch22)

Tracking Error • The standard deviation of the return of the portfolio relative to the return of the benchmark index. • (example on pages 416-417) • Calculate monthly or weekly tracking error • Annualize it

Two Types of Tracking Error • Backward-looking (ex-post) tracking error: tracking error calculated from observed active returns for a portfolio • Forward-looking (ex-ante) tracking error: tracking errors associated with bond market index based on multi-factor models – setting an appropriate benchmark

Risk Factors • Systematic risk factors • Term structure risk factors • Non-term structure risk factors • Non-systematic risk factors • Issuer specific • Issue specific

Active Portfolio Strategies • Interest-rate expectations strategies • Yield Curve Strategies • Yield Spread Strategies • Individual Security Selection Strategies • Strategies for Asset Allocation within Bond Sectors

Interest-rate Expectations Strategies • Increase or decrease duration • increase duration when expected interest goes down • decrease duration when expected interest goes up • Approach: Rate anticipation swaps • Gambling incentive – make an interest bet to cover inferior performance relative to a benchmark index.

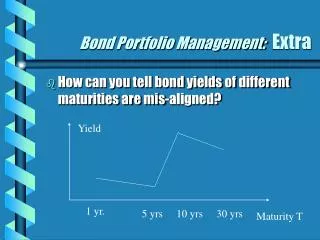

Yield Curve Strategy • Seek to capitalize on expectations based on short-term movements in yields; make profit from the change of yield curve in the portfolio • Key: if your investment horizon is 1 year, what strategy you want to take, put all your money in 1-year bonds or 30-year bonds

Strategies • Bullet strategy (see page 428) • Barbell strategy • Ladder strategy • To see which strategy to implement, investors need look at the impact of the strategy on the total return of the portfolio • Exhibit 19-8 on page 431 compares the relative performance of a bullet portfolio and a barbell portfolio • One factor driving the difference in portfolio performance is the difference in their convexity.

Yield Spread Strategies • Involve positioning a portfolio to capitalize on expected changes in yield spreads between sectors of the bond market. • Swapping one bond for another when manager believes that the prevailing yield spread between the two bonds in the market is out of line with their historical yield spread.

Yield Spread Strategies • Credit spread • Spreads between callable and noncallable securities

Individual Security Selection Strategy • Identify mis-priced securities • Its yield is higher than that of comparably rated issues • Its yield is expected to decline because credit analysis indicates that its rating will improve • To implement this strategy: swap.

Use of Leverage • A portfolio in which a manager has created leverage. • If return from investing the amount borrowed exceed cost of funding. • Leveraging trades will generate a return needed to make the investment attractive to traders.

Create Leverage with Repo Repurchase agreement: sale of a security with a commitment by the seller to buy the same security back from the purchaser at a specified price at a designated future date. Repurchase price Repurchase date Repo rate Overnight repo versus term repo

Example • A dealer delivers (sells) $10 million of treasury security to a customer and buy it back in to the next day. Repo rate is 6.5%. (dealer is financing a long position) (page 441) • What is amount borrowed by the dealer? • What is the dollar interest • Jargons: (1) reversing out securities, (2) reversing in securities – page 442

Indexing • Designing a portfolio so that its performance will match the performance of some bond index • Benefits and costs • Low management fee and expenses • Straightforward and easy to evaluate • Basis risk between indexing and matching to liabilities

Factors Affecting Index Selection • Level of Risk Tolerance • Investor’s objective • Difference in variability • Nonsymmetry in rising and falling markets

Alternative Indexes • Lehman Brothers U.S. Aggregate Bond Index • Salomon Smith Barney (SSB) Broad Investment-grade Bond Index (BIG) • Merrill Lynch Domestic Market Index • Exhibit 20-2, sector breakdown of Lehman Brother index

How to Create an Indexed Portfolio • Tracking error: the discrepancy between the performance of the indexed portfolio and the index • The tradeoff between transaction costs and mismatching of the characteristics of the indexed portfolio and the index. • Have logistic problem (see pages 457, 458)

Specific Approaches • Stratified sampling approach • Based on characteristics (page 456) • Optimization approach • Jointly consider characteristics and fund objectives • Tracking error minimization using multifactor model • Enhanced indexing: adding active portfolio management in indexing

Exercises – Ch19 and 20 • 1. Problem 7, ch19 – (a) 288.74, (b) backward-looking, (c) enhanced indexing • 2. Problem 15, ch19 – (a) II, (b) I, (c) the one having greater convexity, (d) don’t worry about it. • 3. Problem 7, ch20