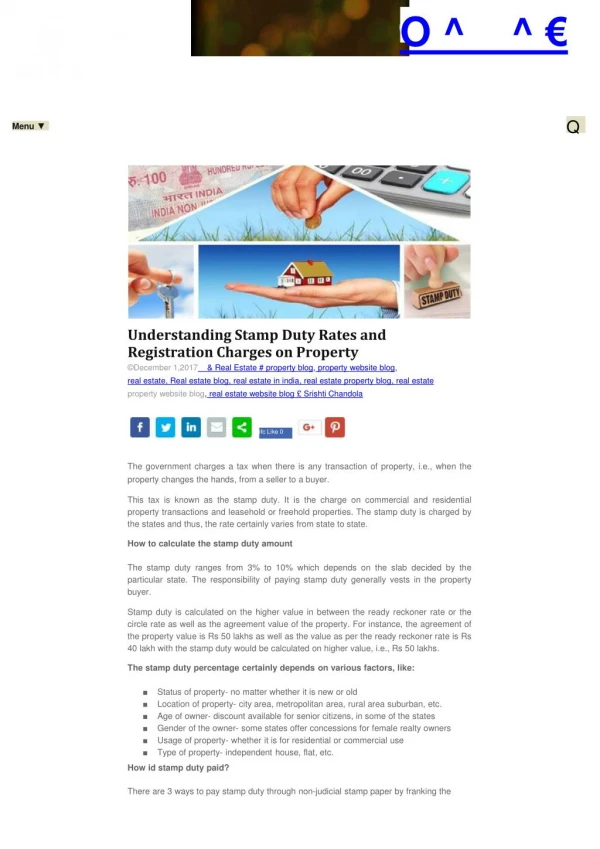

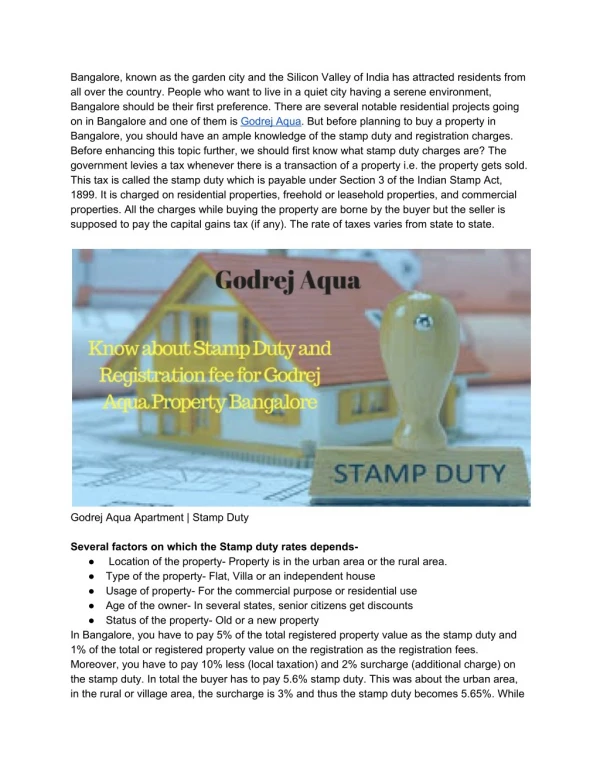

Download

1 / 7

70 likes | 238 Views

Stamp duty March 4th 2011. Legal framework and scope. Act nr. 36/1978 on stamp duty Scope: subject to stamp duty are Leases for real estate and ships that are registered here, as well as other documents that award or transfer the rights to such property.

E N D

Stamp duty March 4th 2011

Legal framework and scope • Act nr. 36/1978 on stamp duty • Scope: subject to stamp duty are • Leases for real estate and ships that are registered here, as well as other documents that award or transfer the rights to such property. • Insurance documents, if they are relevant to a real estate in this country or other valuables, unless it is proved that none of the premium should be paid here. • Bills/drafts, if approved or payment is made in this country. • Documents registered in this country or are the basis for public record in this country.

Main types of documents • The main types of documents related to stamp duty under the provisions of the Act: • Lease agreements (0,4%) • Leases of fishing rights and other duties and obligations on the property• Shares (0,5%) • Association Agreements (2%) • Loan Agreements (1,5%/ 0,5%) • Insurance Bond (1,5%/ 0,5%) • Types of enforcement (1,5%) • Detention of property (1,5%) • Bills and checks (0,25%) • Insurance contracts (0,24% - 8%) • Prenuptial agreements (50 ISK/ 0,4%)

Loan agreements • Stamp duty on loan agreements and insurance bondswhen the debt bears interest, is secured by collateral or guarantee, the stamp duty is 0,09 EUR (15 ISK) for each thousand of the amount. (1,5%) • The stamp duty of other loan agreements and insurance bonds is 0,03 EUR (5 ISK) for each thousand of the amount. (0,5%)

Shares • Stamp duty of shares issued by companies with limited liability is 0,5% of the amount of the bonds. • Certificates for shares in companies with limited liability, other than companies, the stamp duty is the same way as shares. • Association Agreements companies with unlimited liability, the stamp duty is 2% of funds in the company.

Insurance documents • Stamp duty is to be paid on insurance documents. If the insurance policy is issued that document is be stamped, or else the contract, the first receipt or other document regarding the insurance.

Gap analysis • Stamp duty are levied on shares, bonds and loan agreements • Is this consistent to EU rules?