Download

1 / 32

350 likes | 692 Views

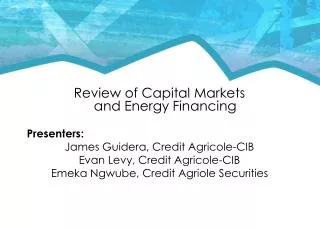

Review of Capital Markets and Energy Financing Presenters: James Guidera, Credit Agricole -CIB Evan Levy, Credit Agricole -CIB Emeka Ngwube, Credit Agriole Securities. Update on the Financing Markets. February 2013. February 2012. 1. Looking Back on 2012.

E N D

Review of Capital Markets and Energy Financing Presenters: James Guidera, Credit Agricole-CIB Evan Levy, Credit Agricole-CIB Emeka Ngwube, Credit Agriole Securities

Update on the Financing Markets February 2013 February 2012 1

Looking Back on 2012 Update on the European Crisis Basel III Implementation and Consequences 2

2011… From Relative Calm to Tumult to relative Calm Again A Greek debt crisis….. but thought to be contained to Greece…… Early 2011 Early 2012 Early 2013 • European Central Bank has stepped-up to fund banks and indirectly sovereigns restoring a degree of market confidence in most sovereign debt • Greece in a box • A full blown European Debt crisis, resulting in downgrades of banks and sovereigns Sovereign Debt European And US Economies • Recession fears in Europe • Mixed economic signals in US but mostly positive • Recession spreading from weaker to stronger economies • Some signs of improvement… • Continued growth in Europe, albeit at a slower pace • Hopes for renewed growth in the US Financial Markets • Improved liquidity • Nervous and volatile markets • Continued historical low rates • Relatively Bullish Markets, even in view of expected weaker growth

The ECB Liquidity Program: Providing some relief • In December 2011, the European Central Bank (ECB), began a program of providing cheap loans to banks, with the funds used principally to buy sovereign bonds. • More than €1 Trillion of 3-year loans were provided under this program, at a reduced spread (-50 bps) in December 2011 and February 2012. Repayments of €137 Billion have already occurred. • Yields on sovereign debt fell, debt issuances have gone well, and the markets have stabilized • Two Year Italian Debt: 1.7% from 7.8% peak • Two Year Spanish Debt: 2.6% from 6.2% peak

CDS Spreads for European Banks January 2012 January 2013

Issues remain… • Floods of liquidity may provide some relief, but don't directly combat the fundamental problems • Greek Solution not yet achieved – is there any solution? • Continued weak economies and high debt burdens • New governments with austerity plans prevail • Recessionary signals for selected countries

Consequences for European Banks Early 2012 Early 2011 Early 2013 • Much higher costs of Liquidity, particularly in US$, for European Banks • Funding cost differences favor Japanese, Canadian banks • Financial impact of plans to reduce funding needs (De-leveraging) Bank Liquidity • Liquidity costs generally lower • Moderate funding cost differentiation among banks • Deleveraging targets achieved for the most part • Resources still abundant and relatively inexpensive • Moderate funding cost differences between banks • 9% benchmark in 2013 required by French regulators • More restrictive definition of capital • More severe weighting of markets activities • Liquidity ratio added to capital ratios • Compliance will limit overall loan growth • Should result in greater loan-pricing differentiation • Tier One Capital Requirement: 7% in 2018 • Wide range of capital instruments available to satisfy requirement BASEL III

Update on Basel III Implementation • Headquarted in Basel, Switzerland the Bank for International Settlements (BIS) has been promoting minimum capital adequacy requirements for participants in the international banking system since the late 1980’s. • Original regime responded to credit bubble driven by over-leveraged Japanese banks, BIS promoted a minimum capital ratio. • Weighted Assets: Bank loans, LOC’s and commitments in the denominator “Cooke-weighting” rules were fairly simplistic, weighting at 100% all funded loans without differentiating among most counterparty risks, and providing lower weightings for unfunded commitments, performance LOC’s, commitments of less than a year. Bank Capital ≥ 8% Weighted Assets

What was Basel II? • Basel II: New capital adequacy targets reported during 2003-4 and phased in through 2008. • Credit risks for loans were weighted based on credit quality, expected loss given default, and duration. The risk-weighted-asset (RWA) regime provides for a much wider range of financial asset weightings based on the credit rating, loan structure (e.g. collateral quality), and duration. Bank Capital = 8% (Credit + Market + Operations) Risk PF examples: RWA/Commitment Construction mini perm for PPA-hedged generator 8-25% Miniperm for merchant power plant 50-70% Term loan for project portfolio holdco 80% Unsecured corporate revolver (BBB- equivalent) 100% Capital consumption follows the RWA/commitment ratio which is in higher ranges for looser structures, higher counterparty risks, and longer term loans.

Basel III: the regulatory answer to the financial crisis of 2008 • mEconomic cycles are taken into account : • capital buffers to be constituted during expansion phases • Level: up to 2.5% lSystemic Important Financial institutions : Additional level from 1 to 2.5% • kImprovement of the quality of capital : • Close to common equity Regulatory capital Total of risk weighted assets • nTighten levels of regulatory capital : • Common equity 4.5% • Capital conservation 2.5% • p Regulation of excessive leverage : • Introduction of a simpler, transparent • leverage ratio • Higher risk-weighting for: • Securitisation • Market risk • Trading Counterparty credit risk * o Introduction of liquidity standards: • Liquidity Coverage Ratio (1 month) • Net Stable Funding Ratio (1 year) * Project Finance Loan Risk-Weightings unchanged from Basel II

Overview of Basel III Capital Adequacy Calculation Tighten levels of regulatory capital :3 main ratios enhanced by 3 « buffers » with a full implementation starting January 1st 2013 Prior situation As of 2018 for BIS, sooner for certain countries • 3 « Buffer » levels added • l Systemic Buffer : • An additional level from 1% up to 2,5% for systemically important financial institutions • m Countercyclical Buffer : • Core Tier 1 buffer from 0% to 2,5% • To be defined by national supervisors, contingent on macroeconomic indicators, to avoid excess credit growth • n Capital Conservation Buffer : • Capital buffer at 2,5% • If < 2,5%, automatic restriction of dividends and bonus distribution Total capital Hybrid Tier 2 New definition 2,0% ≥ 11,5% Hybrid Tier 1 New definition Tier 1 1,5% Theoretical capital ratio (BIS rules) Systemic Buffer [1% - 2,5%] ≥ 9,5% Countercyclical buffer [0% - 2,5%] Hybrid Tier 2 – 50% deduction = 4% ≥ 8% Capital Conservation Buffer [2,5%] Total capital 8% Core Tier 1 Hybrid Tier 1 - 50% deduction Core Tier 1 -deduction of 100% Threshold : 4,5% Tier 1 4% Core Tier 1

Acceleration of the Basel III Compliance Timetable Timetable for application of the full Basel 3 CET1 ratio (at 31 December of each year) ~ 9% + 2 points 7% Ratio required at 1 January 2019

Introduction of liquidity ratios Two minimum standard ratios designed as a framework for liquidity risk supervision… Implementation timeline extended: Liquidity Coverage Ratio (1 month) shall be disclosed from January 1st 2013 and will be regulatory binding at 60% of target in January 1st 2015 , at 100% in 2019, Net Stable Funding Ratio (1 year) will enter into force in January 1st 2018. Ratio designed to ensure that a bank maintains an adequate level of unencumbered, high-quality assets that can be converted into cash to meet its liquidity needs for a 30-day time horizon under an extreme liquidity stress scenario (name and market crisis) Stock of high-quality liquid assets Total net cash outflows (under stress) over the next 30 calendar days Liquidity Coverage Ratio ≥ 100% Net Stable Funding ratio Ratio designed to guarantee medium and long-term funding of the assets over a one-year time horizon. Non liquid assets, loans with remaining maturity above 1Y, 50% of loans with maturity under 1Y and 5% of OBS commitments should be covered by long term funding (> 1Y) or stable resources. Capital + Liabilities>1Year +Stable deposits Required amount of stable funding ≥ 100%

Basel III Implications for Energy Lending • Regulatory pressure to meet accelerated Basil III ratio targets will limit lending expansion among European banks. • Greater credit pricing differentiation should appear between PPA-hedged and merchant, between opcos secured with hard assets and holdcos secured with shares. • Lender appetite will be very limited for long terms: they attract more capital, they lack liquidity in the market.

U.S. Loan Market Snapshot 16 U.S. Lending Volume • Overall lending volume was down in 2012 vs. 2011 as a result of the following • Unresolved issues in the Eurozone • Looming regulatory concerns for banks • Record year in the bond market • However amid demand-rich technical conditions the leveraged market flourished. Source: Thomson Reuters LPC, S&P Capital IQ LCD

Project Finance Around the Globe 17 • Despite decline in 2012, 4th quarter volume was actually up 11% y-o-y • Australia led in project finance volume in 2012 with a record $82bn driven by 2 large LNG projects ( $34bn Ichthys and $13bn Curtis Island) • North American volume increased for the 3rd consecutive year, reaching $51bn in 2012 driven by merchant power plant financings, wind farm and solar projects, and one LNG project Source: Dealogic

North American 2012 Sector Analysis 18 2012 Sector Volumes (North America) • Energy remains the leading sector within North American PF although declined in 2012 • Lack of PPA’s and continuing low gas prices lowered financing activity on new development and refinancing of merchant projects • Evident increase in wind projects as developers took advantage of subsidies and tax credits • Other projects include Petrochemical/Chemical Plants, Processing Plants, and Steel Mills Source: Dealogic

Project Finance Loan Market in Review – 2012 19 • PPA-Hedged Projects • Increased funding costs and heightened capital considerations early starting margins were pushed up to 275 – 300 bps • However, the margins fell to around 250 bps due to lack of deal flow in 2H012 • Liquidity is deepest for 7 – 10 year mini-perms. • Very select group of sponsors can still push the tenor out, primarily for renewables • Deals were syndicated primarily as clubs. Hold levels were generally between $60-80MM at the top tier. • A more active secondary market developed for PF loans (asset sales) • Merchant Power • Around a dozen commercial banks will consider merchant risk in well-structured and priced transactions with strong sponsorship. • Most merchant power financings were arranged through TLBs in 2012 (approx. 13) • Largest Deal in the market • Successful closing of $3.6bn Sabine Pass Liquefaction tested depth of the PF market

Overview of high-profile deals closed in 2012 20 • Term Loan Bs • $985MM Equipower Resources (ECP) • $750MM LSP Madison (LS Power) • $690MM Panda Sherman/Temple (Panda Power) • $175MM Raven Power Holdings (Riverstone) • Renewables • $650MM Alta Wind VII & IX (TerraGen) • $576MM Centinela Solar Facility (LS Power) • $476MM CSolar IV South (Tenaska) • $467MM Ocotillo Express (Pattern) • $177MM Copper Mountain Solar (Sempra) • Others • $3,626MM Sabine Pass Liquefaction (Cheniere) • $470MM Houston Propylene Pant (Petrologistics)

PF Market Outlook PF Market Outlook 21

PF Energy Sector Historically – Power Financing 22 Impact on Business PPA-hedged deals Predominantly Gas-Fired Plants Abundance of wind generation Growth of utility-scale solar Older coal-unit retirements Market Drivers • Steady Load Growth • Natural Gas Outlook - $5-10/MMBtu • Renewables – RPS criteria, Government Incentives (PTCs, ITC, Cash Grant) • Coal – Emissions playing larger role

PF Energy Sector Going Forward – Driven by Gas 23 Impact on Business Lack of PPAs – Increased merchant activity Shale gas & related infrastructure development Gathering, Storage, Transport LNG (export) Petrochemical Limited wind in U.S. starting in 2014 Larger solar projects with long-term PPAs continue Retrofits, scrubbers, supercritical heat rates Clean coal Contrarian investment opportunities Market Drivers • Low or no load growth • Natural Gas Outlook - $3/MMBtu near-term $5/MMBtu in future • Renewables – Expiration of PTCs • Wind 2013 • Solar 2016 • Coal – Toughening of emissions rules, cheap coal fuel

PF Energy Sector Going Forward – Driven by Gas 24 Financing Response More B-loans – Investors are looking for higher yields 5-7 year mini-perms in the bank market Starting margins in the 350-450 bps range Refinancings of maturing mini-perms Margins below 250 bps Project Bonds for long tenor Acquisition financing Impact on Business • Lack of PPAs – Increased merchant activity • Shale gas development financing • Gathering, Storage, Transport • LNG (export) • Petrochemical • Limited wind in U.S. starting in 2014 • Larger solar projects with long-term PPAs continue • Retrofits, scrubbers, supercritical heat rates • Clean coal • Contrarian investment opportunities

Historical Global Project Bonds Issuances by Region North America Latin America EMEA Asia 26 All figures in USD MM Equivalents Source: PFI Financial League Tables

Historical Global Project Bonds Issuances by Sector Oil and Gas Power Infrastructure Other 27 All figures in USD MM Equivalents Source: PFI Financial League Tables

2012 Transactions 28 Over $24 BN in project bonds closed in 2012.

Transaction Overview – Oaxaca II and IV 30 Investors by Type August 2012 August 2012 USD 148,469,000 USD 150,231,000 Wind Project 144a Senior Secured Notes Wind Project 144a Senior Secured Notes Joint-Bookrunner Joint-Bookrunner • The Transaction • In August 2012, CA Securities priced two Capital Markets offerings for two 102 MW wind projects located in Oaxaca, Mexico. The first offering was for USD 148.5 MM and the second offering was for USD 150.2 MM. • The projects benefit from one of the best wind regimes in the world. • The transactions refinance an existing bank facility provided during construction. • The client achieved a number of important milestones. • Why Significant? • First ever Latin American wind projects to achieve investment grade ratings and to tap the Capital Markets. • First ever USD-denominated wind project bonds outside of the United States. • First ever international project bonds to significantly tap local Mexican institutional investors. • Marketing • CA Securities acted as Joint-Ratings Advisor and Joint-Bookrunner for the Notes. • The final order book comprised of top US and international institutional investors as well as Mexican investors. • Hedge Fund • Private Wealth Management

Crédit Agricole Corporate and Investment Bank (Global Investment Banking)9 quai du President Paul Doumer92400 Courbevoie PARIS FRANCETel. +33 1 4189 8500Crédit Agricole CIB (or Credit Agricole Securities (USA) Inc.)1301 Avenue of the AmericasNew York, NY 10019Tel. (212) 261-7000www.ca-cib.com Disclaimer This presentation was prepared exclusively for your benefit and internal use in order to indicate, on a preliminary basis, the feasibility of a possible transaction or transactions. This presentation is proprietary to Crédit Agricole Securities (USA) Inc. and Crédit Agricole Corporate and Investment Bank (together with any affiliates, “Crédit Agricole”), is confidential and may not be disclosed by you in any manner, including without limitation, any publication of the contents hereof, to any other party. This presentation is incomplete without reference to, and should be viewed solely in conjunction with, the oral presentation provided by Crédit Agricole and any additional written materials intended as a supplement hereto or thereto. Neither this presentation nor any of its contents may be used for any purpose other than the consideration by the employees and professional advisors of your company of the transaction or transactions contemplated herein without the prior written consent of Crédit Agricole. The information in this presentation is based upon available sources and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. In preparing this presentation, we have relied upon and have assumed, without independent verification, the accuracy and completeness of all information available. In addition, our analyses are not and do not purport to be appraisals or any other valuation of the assets, properties, stock, or business of your company. The information contained in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which could have significant valuation and other effects. This presentation is furnished for discussion purposes only and does not purport to specify all of the terms and conditions of any transaction proposed herein. This is not intended to be, and should not be construed as, a commitment to provide financing or buy risks. Crédit Agricole does not make hereby any representations or warranties as to the outcome, financial or otherwise, of any proposed transaction or strategy. Crédit Agricole Securities (USA) Inc. is a U.S. registered broker dealer and a wholly-owned subsidiary of Crédit Agricole Corporate and Investment Bank, a member of Crédit Agricole Group.