Download

1 / 26

270 likes | 302 Views

Learn about Responsibility Center Management (RCM) at UNH, a tool to manage resources strategically to meet academic goals. Discover how RCM impacts revenues, expenses, and governance, promoting transparency and accountability. Explore the journey and future of RCM implementation.

E N D

Responsibility Center Management RCM 401 David Proulx, Assistant Vice President for Financial Planning and Budgeting EMail: david.proulx@unh.edu Budget Office Website: http://www.unh.edu/budget RCM Website: http://www.unh.edu/rcm

RCM 401 Presentation Outline 1. UNH Overview 2. What is RCM? 3. 5 year review

RCM 401 Revenue Summary • $435 million current fund revenues • Research, net tuition and auxiliary revenue greatest sources • Major challenges in state appropriation revenues, financial aid and grant funding • Great dependence on out of state students

RCM 401 Expense Summary • Personnel – largest component of expense • Medical benefit cost growing significantly • Energy costs growing significantly • Behind on renewal and replacement of physical plant • Growth rate on general fund revenue – 4% and expense – 4.5%. Need to address structural issue

RCM 401 Presentation Outline 1. UNH Overview 2. What is RCM? 3. 5 year review

RCM 401 What is RCM? • Responsibility Center Management • A tool to help UNH manage its resources in a manner to meet the goals outlined in the University’s Academic Plan • Informs management of financial impact of decisions • Makes explicit where revenues go and how they are spent • Promotes accountability at all levels of management

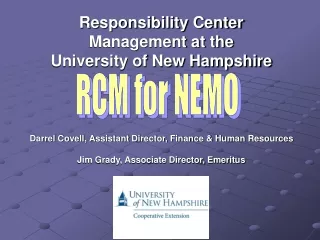

RCM 401 Old Budget System

Revenue - Tuition - Indirect Cost Recovery - State Appropriation Revenue - Direct Revenue (Grant, Gift, Sales, Fees, etc.) Central Budget RC Units Committee - Academic - Incremental funding - Research decisions - Auxiliary - $700k University Fund allocation - Service Unit Advisory Board subcommittee to review Service Units if necessary Direct Expense Institutional Overhead - Salaries, Wages & Benefits - Facilities - Support - CIS - Debt service - Student Affairs - VP Research - General Admin - Academic Affairs RCM 401 RCM Budget System

RCM 401 RC Units

RCM 401 RCM Principles • It should be simple to provide easy comprehension and efficient administration • It should produce results that are widely perceived as fair • It should encourage behaviors that support the institution’s mission and academic plan • It should have strong governance and planning mechanisms

RCM 401 Shared Governance Central Budget Committee • The governing group on budget policy and financial planning for the campus community. • Responsibilities include oversight of RCM, review of internal fees, oversight of assessment rates and central service budgets, oversight of facilities chargeout rates, and advising President on significant budgetary/financial issues. • Comprised of President (Chair), Vice Presidents, 2 Deans, 4 Faculty, 2 RC Unit Directors, Staff rep, Student Treasurer, Graduate Student Organization rep

RCM 401 Unit Financial Structure • Units receive direct revenues (fees, grants, gifts, etc) as well as applicable allocated revenues (net tuition, state appropriations, indirect cost recovery, CBC allocations and hold harmless) • Units are responsible for direct expenses (salaries, wages, fringe benefits, support) as well as indirect expenses (facilities, general and academic overhead) • Unspent funds at end of year are allowed to drop to a unit “reserve” • Most auxiliary operations (MUB, Campus Rec, Health Services, Counseling Center, Housing and Dining) have operated in a RCM type system prior to campus wide implementation of RCM

RCM 401 Before and After • RCM implemented on July 1, 2001.

RCM 401 Presentation Outline 1. Overview 2. What is RCM? 3. 5 year review

RCM 401 Purpose • Understand impact of RCM over the past 5 years • Align RCM allocation methodologies to goals outlined in Academic Plan • Provide opportunity for community to be informed and participate in discussions

RCM 401 Timeline • Dec. 2004 – April 2005 – open discussions with all RC units on RCM • April 2005 – August 2005 – Data accumulation and review structure development • August 2005 – January 2006 – Subcommittee review and Steering Committee recommendations • February 2006 – Central Budget Committee Review and President decision • July 1, 2006 – Implementation of changes

RCM 401 Participation • Steering Committee and 7 subcommittees – 58 total members including 2 students on Steering Committee • 17 meetings and 2 open forums for information gathering/feedback. 2 open forums for initial recommendations.

RCM 401 Review Results • RCM works well for UNH and should remain as budgeting tool • Enhance communications in some areas • Allocation formulas changed to create better incentives/more alignment with Academic Plan (impact in FY07 of changes was zero – offset by hold harmless allocation) • Elimination of hold harmless allocation and review of assessment funded units • RCM should be reviewed again in FY11

RCM 401 Where to get help? • UNH RCM Website – information on 5 year review, RCM principles, RCM manual, etc – www.unh.edu/rcm • Call David Proulx at 2-2421 or send me email at David.Proulx@unh.edu