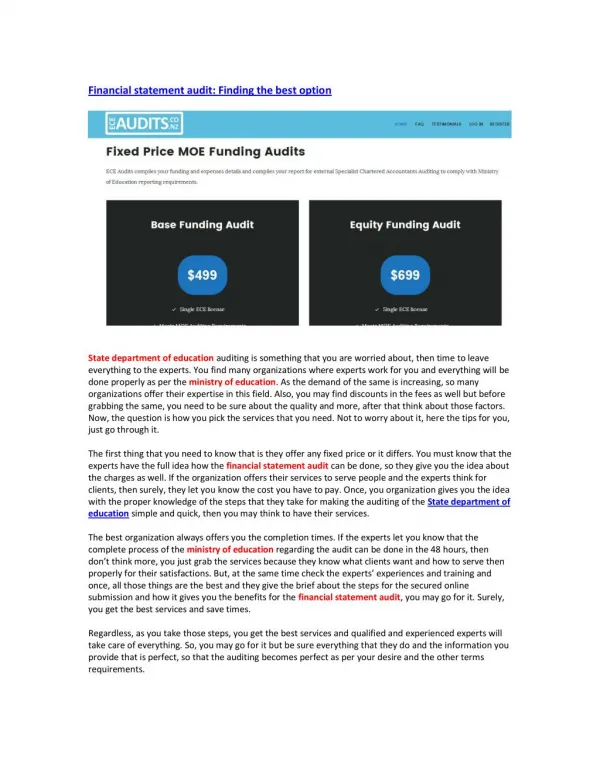

Download

1 / 83

830 likes | 956 Views

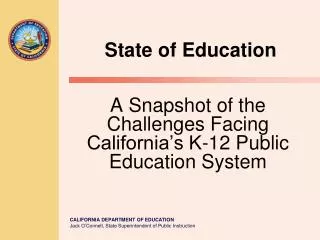

State of Education. Urban vs. Suburban Graduation Rates 2005. Worst High School Graduation Rates of 50 Largest Cities. Omaha, NE 55.1% Houston 54.6 Portland, OR 53.6 Las Vegas 53.1 San Antonio 51.9 Chicago 51.5 Tulsa 50.6 Jacksonville 50.2 Philadelphia 49.6 Miami 49.0

E N D

Worst High School Graduation Rates of 50 Largest Cities Omaha, NE 55.1% Houston 54.6 Portland, OR 53.6 Las Vegas 53.1 San Antonio 51.9 Chicago 51.5 Tulsa 50.6 Jacksonville 50.2 Philadelphia 49.6 Miami 49.0 Oklahoma City 47.5 Denver 46.3 Milwaukee 46.1% Atlanta 46.1 Kansas City, MO 45.7 Oakland, CA 45.6 Los Angeles 45.3 New York 45.2 Dallas 44.4 Minneapolis, MN 43.7 Columbus 40.9 Baltimore 34.6 Cleveland 34.1 Indianapolis 30.5 GRAND PRIZE – Detroit 24.9% America’s Promise Alliance 2008

Tracking Graduation Rates http://apps.arcwebservices.com/edweekv3/default.jsp

History of Retirement Retirement: a complete and permanent withdrawal from paid labor. Historically, retirement has been solely for the rich, however, since 1880 there has been a steady increase in retirement rates. If the current retirement trend continues, 20 year olds today in the US, UK, France and Germany can expect to live 1/3 of their lives in retirement.

Union Pensions Union army veterans retired at a higher rate at all ages than the general public. Union pensions reflect a pure income effect on labor supply. In 1900, a 1% increase in pension benefits increased retirement rates by .73%.

% of Population Aged65 and Older Source: Evolution of Retirement, Costa.

Labor Force Participation Rates of Men Age 65 and Over US UK France Germany Source: Evolution of Retirement, Costa.

Why 65? “Age 65 is generally set as the threshold of old age since it is at this period of life that the rates for sickness and death begin to show a marked increase over those of the earlier years” -Issac Rubinow, 1916 “It is a commonplace fact that physical ability, mental alertness and cooperativeness tend to fail after a man is 65” -Federal Government before the Supreme Court, 1936

Age Discrimination Retirement rates increased from age discrimination at the beginning of the 20th century resulting from: Shorter workdays Scientific Management

Social Security Act of 1935 “The [Social Security] Act does not offer anyone, either individually or collectively, an easy life- nor was it ever intended so to do. None of the sum of money paid out to individuals in assistance or insurance will spell anything approaching abundance. But they will furnish that minimum necessary to keep a foothold; and that is the kind of protection Americans want.” -President Franklin D Roosevelt

Social Security and The New Deal Social Security was intended to provide benefits to retirees and unemployed Social Security was also intended to stimulate consumption -higher wages -reduced work hours -limitations on working ages for older and young workers All of the above modes of increasing consumption made their way into New Deal programs

Importance of Social Security Benefits to Those Aged 65+ 34% 35% 90% to 100% of Income Less than 50% of Income 50% to 90% of Income 31% Source: SSA 2005

The Anatomy of a Ponzi Scheme Current workers far outnumber retirees. Retirees Social Security fit this profile at its creation in the 1930s Workers

The Anatomy of a Ponzi Scheme Current workers struggle to support an increasing share of retirees. Retirees Japan is facing this demographic reality. Workers

The Anatomy of a Ponzi Scheme Retirees The most extreme example, in which a small population of workers supports a mass of retirees. China will face a similar crisis due to a generation of the One Child Policy. Workers

Who We Support Today with Entitlement Spending Population currently over 65 Thousands

Population over 65 by 2025 Who We Will Support in the Future Population currently over 65 Thousands

The Death of Pensions The Wave of Retiring Baby Boomers Will Affect Us All, Potentially Causing:

The Goodyear Model Strike new deal with union (USW here, UAW for GM/Ford/Chrysler Agree to fund VEBA (Voluntary Employee Benefit Association) Trust Put in LESS than needed for full benefits Dilute current shareholders Strap company for cash Use excess earnings from pension Make unions relevant

S&P 500 Pension Status (2008) 10% of companies are fully-funded 90% - the percentage of companies in the S&P 500 index that have a pension plan and are currently UNDERFUNDED Source: Standard and Poor’s

S&P 500 Health Status (2007) Lessthan 2% of S&P 500 companies are fully-funded Only 6 companies out of the S&P 500 have fully-funded health liabilities. The rest are underfunded or not funded at all Source: Standard and Poor’s

PBGC Took More Risk at Exactly the Wrong Time “The Pension Benefit Guaranty Corporation (PBGC) announced February 18 [2008] that it has adopted a new diversified investment policy, which includes investing heavier in equities and alternative investments, to help ensure the federal insurance program can meet its long-term obligations to America’s retirees.”

PBGC Took More Risk at Exactly the Wrong Time …said PBGC Director Charles Millard in a release. “The new investment policy adopted by the PBGC Board of Directors will better manage our invested assets. Although it should generate higher returns, it also offers lower risk through broader diversification. This strategy gives the Corporation a 57% likelihood of full funding within ten years, compared to 19% under the previous policy.” Moved equities from 28% of portfolio to 45% PBGC Diversifies Investment Policies, Melanie Waddell, Investment News, February 20, 2008

Estimated State Government OPEB Funding Source: Pew Center

State and Local Government Revenues Source: Internal Revenue Service

State Budget Gaps Source: CBO & Pew Center

The “State” of California www.lao.ca.gov

Tax Receipts Will Decline Most taxes come from levies on three things: Income (personal and corporate) Consumption (sales, vehicle, fuel, etc.) Assets (property, inventory, etc.) All three main areas are in decline Article #31, DOT

Taxes and the Rich Source: IRS, Statistics of Income, 2008

2006 Federal Tax Schedule 35% 33% 28% 25% 15% 10% $7,550 S $15,100 M $30,650 S $61,300 M $74,200 S $123,700 M $154,800 S $188,450 M $336,550 S $336,550 M

Top Federal Individual Income Tax Rates1913 - 2010 Source: IRS

Federal Tax Schedule: 1980 vs. 2006 Marginal Rates for Single Taxpayer (1980 Tax Brackets adjusted for inflation) $7,550 S $15,100 M $30,650 S $61,300 M $74,200 S $123,700 M $154,800 S $188,450 M $336,550 S $336,550 M Source: IRS (Inflation Adjustments made by HS Dent using BLS data)