Warsaw

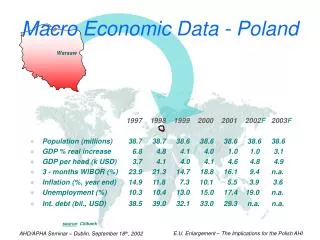

Macro Economic Data - Poland. Warsaw. 1997 1998 1999 2000 2001 2002 F 2003 F Population (millions) 38. 7 38.7 38. 6 38.6 38.6 38.6 38. 6 GDP % real increase 6.8 4.8 4.1 4.0 1. 0 1.0 3.1

Warsaw

E N D

Presentation Transcript

Macro Economic Data - Poland Warsaw • 1997 1998 1999 2000 2001 2002F 2003F • Population (millions) 38.7 38.7 38.6 38.6 38.6 38.6 38.6 • GDP % real increase 6.8 4.8 4.1 4.0 1.0 1.0 3.1 • GDP per head (k USD) 3.7 4.1 4.0 4.1 4.6 4.8 4.9 • 3 - months WIBOR (%) 23.9 21.3 14.7 18.8 16.1 9.4 n.a. • Inflation (%, year end) 14.9 11.8 7.3 10.1 5.53.9 3.6 • Unemployment (%) 10.310.4 13.015.0 17.4 19.0 n.a. • Int. debt (bil., USD) 38.5 39.0 32.1 33.0 29.3 n.a. n.a. source: Citibank

Macro Economic Data - Poland Warsaw • 1997 1998 1999 2000 2001 2002F • Export ( % change) 11.4 10.612.5 7.2 7.2 3.7 • Import ( % change) 18.1 13.77.1 1.7 1.31.3 • Trade balance ($ bil.) 11.3 13.7 14.4 13.2 11.7 10.0 • Official reserve ($ bil.) 20.7 28.3 27.3 27.5 26.6 n.a. • Budget deficit ( % GDP) 3.0 4.3 7.5 6.3 4.0 4.0 • source: Citibank

Polish Agricultural Situation – The End of 2001 All graphs source: GUS

Animal Production in Poland All graphs source: GUS

Animal Production in Poland - Swine Poland has been a sizeable pig meat producer for many years. Pig livestock accounts for about ¼ of the total va-lue of domestic marketable agricultural output. Two major pig breeds pre-vailing in the breeding and herd improvements activi-ties are Large White Polish (LWP) and Polish White Landrace (PWL). Recently, greater interest in pig live-stock production has been observed, which results lar-gery from reduced beef consumption and optimistic forecast on good forage crop in 2002, especially cereals.

Polish Poultry Market Segmentation Apart from pig and cattle livestock, the poultry pro-duction is also of some significance in Poland. In 2000, the poultry live-stock (six months and older) was 53.3 million heads. Chicken accounted for 90.6% of total poultry, including 80.1% of laying hens. However, the broiler production grew and achie-ved 550 million heads. Total poultry density per 100 hectares of farmland at the 2001 end was 302 heads (289 in 2000), and 396 heads per 100 hectares of arable land (379 in 2000). Broilers 550 000 000 Repro Hens (broilers) 4 500 000 Commercial layers 23 000 000 Repro Hens (hens) 450 000 Turkeys 18 000 000 Geese 3 000 000

Major „Players” With Registered Products (alphabetically) 112 companies, both national and foreign once, supply pharmaceutical products, which according to the Polish Pharmaceutical Law must be registered. Some of them are represented by domestic firms, or by foreign companies that established their own subsidiary in Poland. The major are listed below: Animal Trade representing: Boehringer, Bayer Poland alsorepresenting: Biocor, Biowet Gorzów Wlkp.alsorepresenting: Chassot, Vetoquinol, Laboratorios Syva, Biowet Puławy Ceva Sante Animale alsorepresenting: Francodex, Virbac, Vetem, Sanofi Drwalewskie Zakłady Przemysłu Bioweterynaryjnego Elanco/Eli Lilly Fatro Polska Interbiowet Intervet Int. BV alsorepresenting: Cross Vetpharm Group, Knoll, Jelta Krka Lek Polska Medivet PPH representing: Abic, Dopharma, Upjohn, Janssen, Merial Naturan JVCo alsorepresenting: Antec, Novartis Poland Pfizer Polska alsorepresenting: Evans Vanodine Int., Pliva DD Polfa: Grodzisk Mazowiecki, Rzeszów, Kutno, Lublin, Pabianice, Tarchomin, Warszawa ScanVet Poland representing: Cyanamid, Fort Dodge, Norbrook, Schering-Plough

Animal Health Products Market Potential All graphs source:Merial estime

AHP Market, Poland – SWOT Analysis (to be continued ...) I will present following SWOT analysisfocusing on two major areas:Polish Agriculture in total,and Animal Health Product Market as such STRENGHTS POLISH AGRICULTURE • Considerable by size, high quality agriculture area (18.4 million ha = 13.5% E.U. ag. area) • Clear, uncontaminated environment • Strong, traditional farmers attachement to the farmland (always private land ownership) • Deeply rooted animal breeding – esp. horses, swine • Relatively low grain production cost ANIMAL HEALTH PRODUCT MARKET • Very well educated veterinarians (around 10200 vets, including 8000 active) • Relatively low (2-3%) cost of vet service (in commercial animal production) WEAKNESSES POLISH AGRICULTURE • NO governmental support for agriculture • NO government’s long term agricultural strategy • UNCLEAR E.U. access policy in the eyes of farmers • insufficient agriculture data base and market survey • spread, small sized herds (swine, cattle) • limited cash flow • fear for ongoing changes resulting in limited investments • decrease in swine and poultry export - 70% • meat price decrease:swine 35%, poultry 27-38%, eggs 40% • unstable meat prices ==> reduction in production • import: pork from the E.U., poultry from the U.S. and Brazil ANIMAL HEALTH PRODUCT MARKET • Old Pharmaceutical Law, often not matching the current situation (to be substituted by a new Pharmaceutical Law on October 1st) • AHP Registration Process – time consuming, costly, often „overheated „ • Low economy of animal production affecting Vet Sector by: - decreased turnover - 40%- producers limits funds on prophylaxy- needed expensive promotional actions • Other examples from agriculture sector: - 50% drop in fertilizers sale (compared to the last year) - 20% lower herbicides sale

AHP Market, Poland – SWOT Analysis (continuation) ... OPPORTUNITIES POLISH AGRICULTURE • Clear agriculture polices, based on E.U. regulations, and transparent, long term government agricultural strategy • Cattle market development: • Dairy - size, productivity, milk quality, management practices, know-how transfer • - business profitability (investment) • „...cow herd of at least 25-30 heads prevequisite for profitable production. Milk productivity can be increased by: modern genetics, proper feeding, well equipped cowsheds and wide use of milking machines...” Top Agrar • Beef - chances for a new business (investment) • Swine market development: • - production concentration, and new integrated systems in swine production - needs for wide service (including Vets) • Poultry integration, growing turkey segment - foreign capital entering Poland • - cost optimization (health/mortality/effectiveness) - know-how transfer • “Healthy food” for Europe, Agro-tourism, “grain” warehouse • ANIMAL HEALTH PRODUCT MARKET • Growing middle class and fashion to keep pets • AHP: - new pharmaceutical law, one independent Registration Department with four Commissions (previously one Registration Bureau) • - registration process improvement (E.U. like, mutual recognition) • - full control (prescriptions, products classification, volume) of the drug market - wider assortment - new vaccines and pharma(especially for cattle line) • - new, comprehensive approach to the specialized client

AHP Market, Poland – SWOT Analysis (continuation) ... THREATS POLISH AGRICULTURE • Unfulfilled farmers’ expectation regarding E.U. entrance • Tough transitional period • Time of rapid changes abused by „grey area” • Temporarily increased unemployment, in rural area especially • Necessity to create the new agriculture-oriented services • Rapid, initial production cost increase • Indication to maintain a narrow, niche sector of agriculture • Uncontrolled dominance of agricultural goods from E.U. countries at the Polish market ANIMAL HEALTH PRODUCT MARKET • Strong dominance of Western pharmaceutical companies • Uncontrolled influx of newly set updrug companies on Polish market • Temporary trend “to sale” rather then “to serve” • Rapid, initial animal health products’ cost increase However, being aware and proactive we can avoid it . Knowing, what I have presented, you shouldn’t hesitate to vote YES .to the Nice Treaty .

Wider e-information available on: www.minrol.gov.pl Ministry of Agriculture and Rural Development www.arr.gov.pl Agriculture Market Agency www.stat.gov.pl National Statistic Bureau www.cihz.com.pl Foreign Trade Information Center You might also contact me in the , Poland office: (48-22) 629 13 04 e-mail: piotr.czarnecki@merial.com.pl Thank you for your attention